by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAX TIPS, TAXES

A recent article by the National Review brought to light how the IRS has taken on the role of “rules interpretation” in recent years, which is beyond its scope as the nation’s tax collecting agency. The most notorious example of this new role is highlighted in the King vs Burwell case before the Supreme Court — where the IRS interpreted the language of Obamacare other than what was expressly written down as law. However, as the National Review discusses, the IRS has grown accustomed to interpreting law as it sees fit, without the oversight of Congress. Therein lies the problem.

With Burwell, the question being debated is over the letter of the law vs the spirit of the law. As Obamacare was written, tax subsidies were available for federal exchanges (letter of the law). As the IRS is the administrator, so to speak, of the subsidies, it interpreted that line of law to apply to all healthcare exchanges (spirit of the law) and ruled that subsidies were available for both federal and state exchanges, even though Obamacare never specified state exchanges, only federal. The federal government was sued, claiming that the IRS had not the power to administer subsidies beyond what was written, passed, and voted into law. SCOTUS will issue its ruling on the matter later this summer.

The question of rules interpretation is an interesting one. How much power, if any, does the IRS have in sorting out the minutiae of detail in the myriad of tax credits and subsidies that the tax code is riddled with?

The potential for abuse is certainly there. The National Review article focused on just one type of tax credit, the “production tax credit” (PTC) which applied to wind-energy producers, and all the changes the IRS made to the rules regarding this tax credit over the past few years:

*“In December 2012, Congress extended the production tax credit (PTC) to cover wind-energy producers who were in the beginning stages of construction by the subsidy’s cutoff date. The IRS clarified shortly thereafter that wind-farm projects would be able to receive the special tax giveaway if they spent as little as 5 percent of the construction costs.”

*“In April 2013, the IRS apparently decided the tax credit wasn’t large enough. So it simply raised the value of the PTC from $22 per megawatt-hour of electricity produced to $23 per megawatt-hour. Voilà — more federal spending courtesy of you, the taxpayer.”

*“In September 2013, the IRS went a step further. It expanded the PTC to cover wind-farm projects that generate power before the end of 2015, despite the fact that the PTC for all projects was set to expire at the end of 2013. The IRS also said in the notice that even projects that come online after that might still qualify; the agency intends to make decisions on a project-by-project basis.”

*“In August 2014, the IRS decided it would not only pay wind-energy developers for each megawatt-hour they produce. It would also allow them to sell a project — regardless of whether it was completed — and use the selling costs they incur to count toward qualifying for the PTC.”

*“The IRS also loosened its requirement that companies need to spend only 5 percent of construction costs to qualify. The agency said it would consider only the nature of the work (such as digging foundations, installing transformers, building roads), not the extent or the cost of the overall project. This more subjective standard gave the IRS even more leeway in doling out government subsidies.”

*In March 2015, the IRS loosened the PTC eligibility requirements yet again. The agency clarified what “begin construction” means. Under the new guidance, if a wind-project developer began construction on a new facility prior to January 1, 2015, and places the project in service before January 1, 2017, then the facility will be considered to be in progress for the purposes of receiving the PTC. This is regardless of the amount of physical work performed or the amount of costs paid or incurred within that amount of time.”

The PTC tax credit, between December 2012 and March 2015, had its rules significantly altered by the IRS. The crux of the issue, however, is the fact that this happened without any congressional oversight. The IRS workers, the ones making the decisions on these rules, are unelected, and accountable to no one. And yet, the changing of the tax credit affects the taxpayer. National Review notes, “While the PTC has historically averaged roughly $5 billion per year, the most recent one-year extension will cost taxpayers $13 billion.” That is an alarming expansion of taxpayer money just in this particular credit instance, without the approval of Congress.

This is also an effect of the larger problem of Congress using the tax code to pick winners and losers. Here, we have special tax credits to companies in order to push “green energy”. It is the essence of crony capitalism, where politicians trade favors and barters to support certain initiatives or restrict others via new taxes or credits. They’re basically all gimmicks to aid in reelection or pander to a portion of the electorate — and then we never get rid of all the tacked-on programs and policies because no one wants to give up their special initiatives.

The code has grown immensely complex. And now we have the IRS regularly going beyond its authority as well. The IRS must be reigned in from interpreter of law back to mere enforcer, as it goes about its business of tax collection. As such, Congress would also do well to reduce the amount of crony capitalism it engages in and stop playing games with our tax code.

by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

The Treasury Inspector General for Tax Administration (TIGTA) found even more missing emails from Lois Lerner among the recycled back-up tapes, which has provided now about 35,000 emails that were deemed lost and destroyed.

This new batch of roughly 6,400 emails is particularly interesting, because it spans 2004- 2013, so it covers the time frame both before and after Lerner’s hard drive crashed in 2011. About 650 emails appear to be from 2010-2011, which is the crucial time during which Lerner’s IRS targeted conservatives groups by denying or prolonging their 501c4 application process.

The bulk of the emails, however, are from 2012. 2012 was the presidential election year. However, by early 2012, we already know that Lerner was instructing her workers to be careful about what they put into writing.

An email written in February 2012 — which was released by Judicial Watch and not part of the newly found emails — reveals a conversation between Lois Lerner and Holly Paz, one of her employees who served as the former Director of the Office of Rulings and Agreements. Paz’s position as Director of the Office of Rulings and Agreements meant that she “oversaw the tax law specialists who provided guidance to the agents in Cincinnati reviewing “tea party” and other applicants, as well as the department involved with processing the applications.” In Lerner’s email to Paz, she discusses training her employees to be mindful of what they write down:

“We are all a bit concerned about the mention of specific Congress people, practitioners and political parties. Our filed folks are not as sensitive as we are to the fact that anything we write can be public–or at least be seen by Congress. We talked with Nan [Downing – Director of EO Examinations] and she thought it would be great if R & A [Rulings and Agreements] could put together some training points to help them understand the potential pitfalls…

I realize everyone is very busy, but I’d like you and Tom [Miller EO adviser] to get together to work out a reasonable plan for completing the review and reporting back on some of the issues he thinks we’d need to cover. If you need more info, we can talk. Thanks”

If Lerner was mindful by then of written records, what the new Lerner emails could reveal might depend on who they were going to. However, Lerner was apparently not entirely so concerned about covering up everything, because other separate FOIA records have revealed emails between Lerner’s office and other government groups and officials.

For instance that in 2012 and 2013, Elijah Cummings and the IRS were in communication. In April 2014, it was reported that the “House Oversight Committee show staff working for Democratic Ranking Member Elijah Cummings communicated with the IRS multiple times between 2012 and 2013 about voter fraud prevention group True the Vote. True the Vote was targeted by the IRS after applying for tax exempt status more than two years ago. Further, information shows the IRS and Cummings’ staff asked for nearly identical information from True the Vote President Catherine Engelbrecht about her organization, indicating coordination and improper sharing of confidential taxpayer information.”

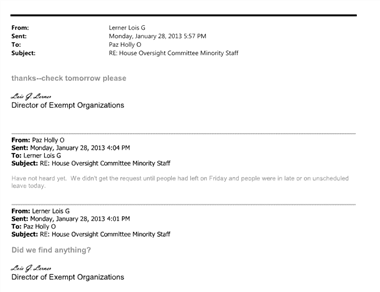

What’s more, the same Holly Paz mentioned earlier colluded with Lerner to provide True the Vote’s 990’s to Cumming’s staff in early 2013: “On January 28, three days after staffers requested more information, Lerner wrote an email to her deputy Holly Paz, who has since been put on administrative leave, asking, “Did we find anything?” Paz responded immediately by saying information had not been found yet, to which Lerner replied, “Thanks, check tomorrow please.” The 990’s were sent three days later.

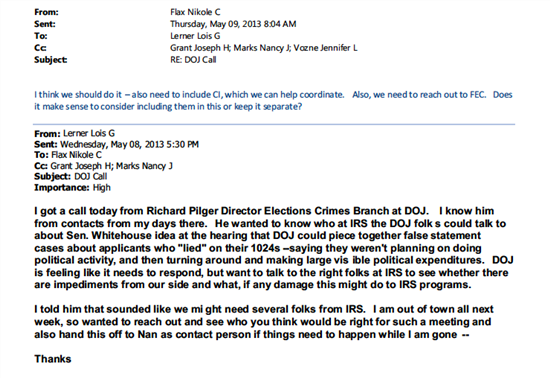

Similarly, in 2013, it has been noted that Lerner was in communication with the Department of Justice regarding prosecuting tax exempt groups. A email obtained by a FOIA request, written by Lerner just two days before the IRS scandal broke in May 2013, stated,

“I got a call today from Richard Pilger Director Elections Crimes Branch at DOJ … He wanted to know who at IRS the DOJ folk s [sic] could talk to about Sen. Whitehouse idea at the hearing that DOJ could piece together false statement cases about applicants who “lied” on their 1024s –saying they weren’t planning on doing political activity, and then turning around and making large visible political expenditures. DOJ is feeling like it needs to respond, but want to talk to the right folks at IRS to see whether there are impediments from our side and what, if any damage this might do to IRS programs. I told him that sounded like we might need several folks from IRS,” Lerner wrote in a May 8, 2013 email to former Nikole C. Flax, who was former-Acting IRS Commissioner Steven T. Miller’s chief of staff.

“I think we should do it – also need to include CI [Criminal Investigation Division], which we can help coordinate. Also, we need to reach out to FEC. Does it make sense to consider including them in this or keep it separate?” Flax responded on May 9, 2013.”

Incidentally, that wouldn’t be the first time Lerner explored such a scenario with the DoJ, and Pilger in particular; she did so even way back in 2010. National Review reported last June that “The Internal Revenue Service may have been caught violating federal tax law. In October 2010, the agency sent a database on 501(c)(4) social-welfare groups containing confidential taxpayer information to the Federal Bureau of Investigation, according to documents obtained by a House panel.

The information was transmitted in advance of former IRS official Lois Lerner’s meeting the same month with Justice Department officials about the possibility of using campaign-finance laws to prosecute certain nonprofit groups. E-mails between Lerner and Richard Pilger, the director of the Justice Department’s election-crimes branch, obtained through a subpoena to Attorney General Eric Holder, show Lerner asking about the format in which the FBI preferred the data to be sent”.

The Department of Justice never formally did anything to the social welfare groups, but it was shortly thereafter that targeting was begun by Lerner — not to current 501c4s, but new groups applying for status. “E-mails cited in a committee report released in March [2014] show that the [Citizen’s United] decision caused a lot of angst for Lerner and her colleagues in the IRS’s Exempt Organizations division, and she noted in public remarks that the agency was under pressure to “fix the problem” created by the decision.”

TIGTA is expected to release its report later this year on all the missing 35,000 emails, which will include this new-found batch. After TIGTA’s report comes out, a second report by a bipartisan Congressional committee will also be released, and the public will be able to see more clearly what Lerner was trying to hide when she discarded her computer hard drives.

.

by | ARTICLES, BLOG, ECONOMY, FREEDOM, OBAMA, POLITICS, TAX TIPS, TAXES

Forbes recently had a very good article which explores the US Federal Debt and how it affects economic growth. It also reviews government debt for the future, and its affect on the private sector and the debt-to-GDP ratio. Unfortunately, it doesn’t cover the entirety of US debt, which includes substantial entitlement obligations, but that’s probably fodder for another article entirely. If you want a decent primer on our federal debt — which translates into $154,161 each taxpayer owes towards it — read the article below.

The availability of credit in the U.S. was a major catalyst in the economic boom of the twentieth century. However, too much of a good thing can also be a problem. Is the U.S. too reliant on debt? Is the federal government mortgaging the future earnings of an entire generation? In this article, we’ll explore these and other issues as we take a look at the debt cycle in America.

The Impact of Debt on Economic Growth

In the early part of the twentieth century, if people didn’t have the money to purchase an item, they would save for it. With the introduction of credit terms, high-dollar items became much more affordable. It also changed the way we view debt. For example, rather than think of a new car in terms of its total price, we began to focus on the amount of the monthly payment. And, as the use of debt increased, the American standard of living rose with it. Excessive debt was also one of the primary catalysts for the economic boom of the 1980s, 1990s, and part of the 2000s. However, when debt is used in excess, it steals from the future since it must be repaid. This is because a dollar borrowed today necessitates that a dollar plus interest be repaid in the future. This reduces the amount of money available for future spending. If the amount of debt accumulated is significant and the period of accumulation is long, the required debt payments will negatively impact economic growth. What about government debt? How does it impact the future and the economy?

Government Debt and the Future

As I write this article, the federal government has accumulated $18.2 trillion of debt. In 2004, the federal debt was $7.3 trillion. This rose to $10 trillion when the housing bubble burst four years later. Today it exceeds $18 trillion and is projected to approach $21 trillion by 2019. When you break this down to an amount per taxpayer, the numbers are substantial. It has more than doubled over the past 11 years, rising from $72,051 per taxpayer in 2004 to $154,161 today. As the debt continues higher, the liability of every taxpayer is also rising. The change in the amount of the federal debt per taxpayer from 2004 to 2015 represents an average annual increase of 7.16%. This is much more than the average annual wage increase during the same period.

The Great Private Sector Extortion?

What problems might result from our fiscal failure? With the debt per taxpayer as high as it is, if the government continues to raise taxes on middle income earners and above, it will become increasingly difficult for many of these individuals to preserve their standard of living. This will result in a reduction of wealth that spans the entire income spectrum, excluding perhaps the super-rich. The difficulty will begin in the middle class and eventually creep toward the higher income earners if the debt problem persists. Why will this create difficulty? Because these individuals will be asked to pay higher taxes so the federal debt can be retired. It may be framed under a pretense of patriotism but will really be just another excuse to extract money from the private sector. As the private sector shrinks, economic activity will slow which will result in smaller wage increases. Therefore, these individuals will be squeezed from both ends (taxes and wages). This is one of the key reasons why the middle class is shrinking. It’s as if we’re all on the Titanic and people are continuing to sing and dance while the ship slowly sinks. Does the federal government have the ability to repay its debt? And, if it does today, what about in five or ten years? How difficult will it be then? Let’s address this question now.

The U.S. Debt-to-GDP Ratio

The debt-to GDP ratio compares the amount of the public debt to the size of the economy. For example, if GDP – which is the total of all goods and services produced in the U.S. – is $17.0 trillion and the debt is the same amount, the ratio would be 100%. As the debt rises beyond GDP, the ratio will exceed 100%. This indicates that the debt is greater than the total of what we produce. You might equate it to an individual’s debt-to-income ratio which helps lenders assess an individual’s ability to repay a loan. America’s debt-to-GDP ratio in 1980 was only 35.4%. Ten years later it was 57.7%. As you can see from the chart below, America’s debt-to-GDP ratio has continued to rise and today stands at 102.6%. Although this is not a staggering percentage, as an absolute number, $18.2 trillion in debt is very formidable.

Is the federal government getting in over its head? Will the mounting debt cause a financial hardship on Americans? As the debt continues to expand, the economy will continue to be sluggish, the tax burden will continue to grow, and the middle class will continue to shrink. If Washington doesn’t act soon, will the debt become an unmanageable burden? I believe the answer to this questions lies somewhere between “absolutely” and “very likely.” How bad could it get? It’s difficult to say. To change direction, however, we will need elected officials who are willing to put the needs of the country ahead of their own agenda. In other words, politics will have to take a back seat. You can be sure of this: You cannot circumvent the laws of economics. If we continue to accumulate debt, if we ignore the warning signs, if our officials maintain the status quo, there will be consequences. I only hope America realizes it before it’s too late.

by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

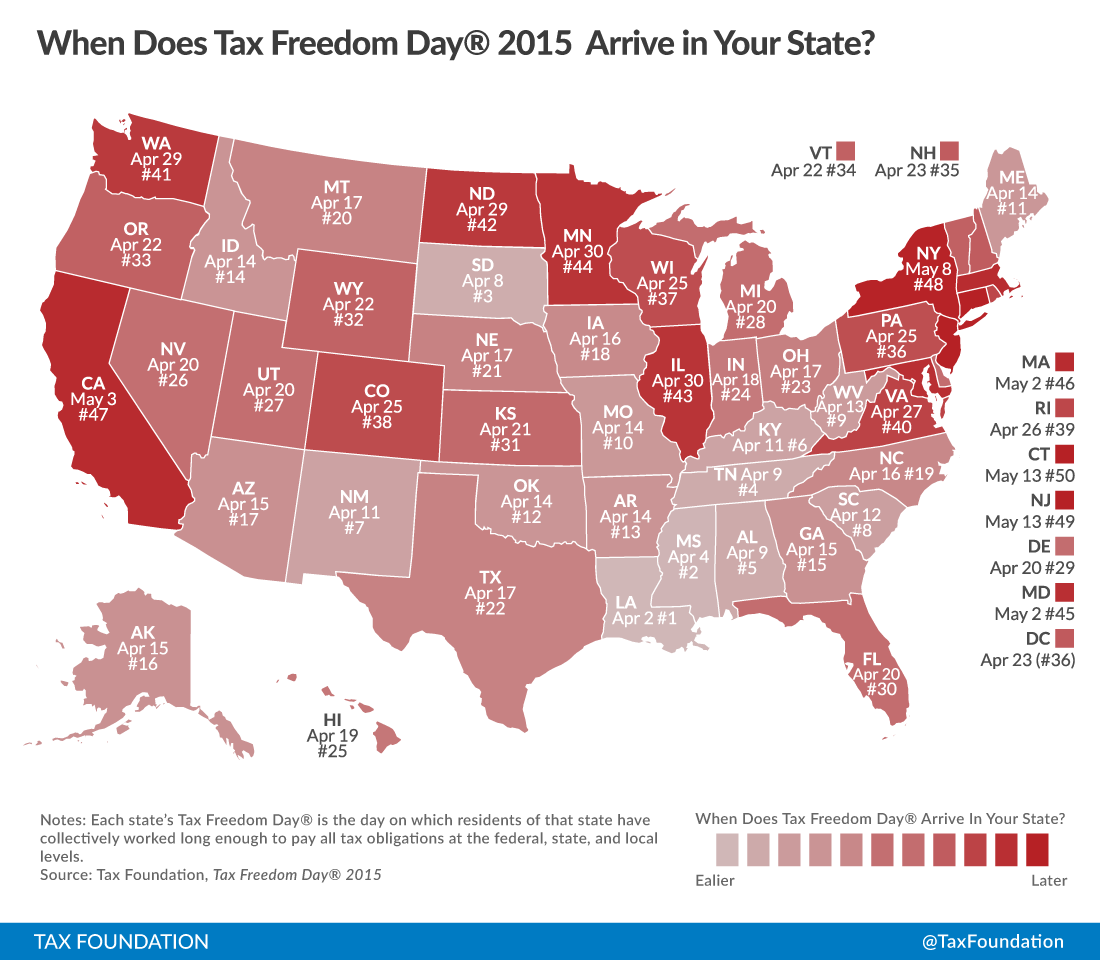

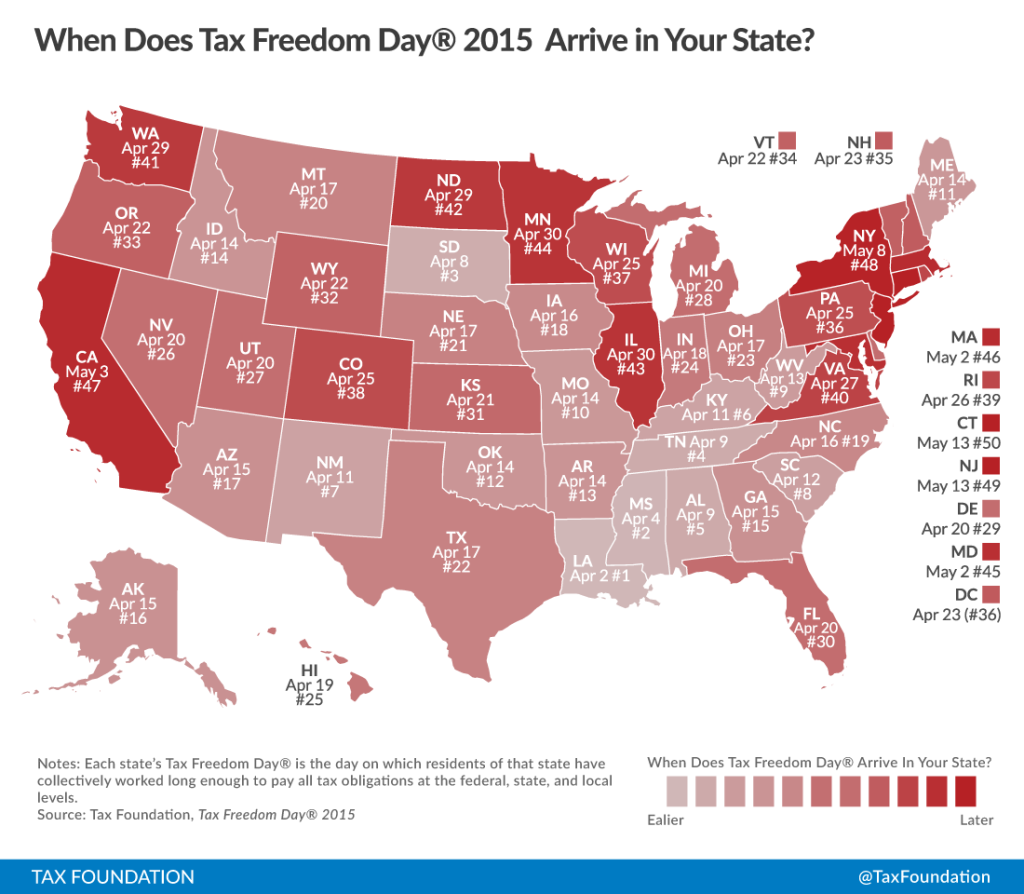

Each year, the Tax Foundation releases its annual report measuring Tax Freedom Day, “the day when the nation as a whole has earned enough money to pay its total tax bill for the year.” Tax Freedom Day is today. April 24th. It takes 114 days of working to pay the country’s tax bill.

Some important findings:

“Americans will pay $3.3 trillion in federal taxes and $1.5 trillion in state and local taxes, for a total bill of more than $4.8 trillion, or 31 percent of the nation’s income.

Tax Freedom Day is one day later than last year due mainly to the country’s continued steady economic growth, which is expected to boost tax revenue especially from the corporate, payroll, and individual income tax.

Americans will collectively spend more on taxes in 2015 than they will on food, clothing, and housing combined.

If you include annual federal borrowing, which represents future taxes owed, Tax Freedom Day would occur 14 days later on May 8.

Tax Freedom Day is a significant date for taxpayers and lawmakers because it represents how long Americans as a whole have to work in order to pay the nation’s tax burden.”

According to the Tax Foundation, the farthest Tax Freedom Day in the calendar year was in 2000, when Tax Freedom Day was May 1. That year, “Americans paid 33 percent of their total income in taxes that year. A century earlier, in 1900, Americans paid only 5.9 percent of their income in taxes, meaning Tax Freedom Day came on January 22. The last time Tax Freedom Day was this late in the year was 2007 (April 25).”

Additionally, Tax Freedom Day is calculated state-by-state. Some states have a more progressive tax system and higher taxes, and some have a lower tax burden. The latest Tax Freedom Day is found in New Jersey and Connecticut, whose Tax Freedom Days fall on May 13th. A few states have Tax Freedom Days earlier than the national Tax Freedom Day; Louisiana is the earliest on April 2nd. You can see how your state fares:

In case you are interested in the methodology of the Tax Foundation, they issues the following description: “In the denominator, we count every dollar that is officially part of national income according to the Department of Commerce’s Bureau of Economic Analysis. In the numerator, we count every payment to the government that is officially considered a tax. Taxes at all levels of government—federal, state, and local—are included in the calculation. In calculating Tax Freedom Day for each state, we look at taxes borne by residents of that state, whether paid to the federal government, their own state or local governments, or governments of other states. Where possible, we allocate tax burdens to the taxpayer’s state of residence. Leap days are excluded to allow comparison across years, and any fraction of a day is rounded up to the next calendar day.”

by | ARTICLES, BLOG, ELECTIONS, FREEDOM, OBAMA, POLITICS, TAXES

Earlier this year, John Koskinen, the IRS Commissioner, complained about the IRS budget given to him by Congress. It was reduced by nearly $350 million for this fiscal year. Commissioner Koskinen claimed the “agency’s $10.9 billion budget is its lowest since 2008. When adjusted for inflation, the budget hasn’t been this low since 1998.”

Due to budget cuts, the IRS warned that customer service would be reduced. The Taxpayer Advocate, (the IRS watchdog of sorts) recently gave her semi-annual report to Congress and discussed this issue at length. Among her findings were 1) if you call, it is likely that only half of the estimated 100 million people will ever reach an IRS agent on the other end; 2) hold times will exceed 30 minutes or more; and 3) the IRS is mandated to provide callers with the option to speak to a live person on its helplines, but would not even clarify to the Taxpayer Advocate which lines are designated helplines when calling in.

Now it seems that the dire, reduced customer service has already been happening for the past year and was orchestrated by the IRS itself. A new House Ways and Means report shows that, “while congressional funding for the IRS remained flat from 2014 to 2015, the IRS diverted $134 million away from customer service to other activities. In addition to the $11 billion appropriated by Congress, the IRS takes in more than $400 million in user fees and may allocate that money as it sees fit. In 2014, the IRS allocated $183 million in user fees to its customer service budget, but allocated just $49 million in 2015–a 76 percent cut.” How much more will they cut for FY2016? How much worse will customer service get?

Just as Obama dared to close national parks and monuments and cut off treatment for cancer kids during the government shutdown, in order to inflict pain on ordinary citizens, the IRS decided follow the same tactic and abrogate its basic responsibility to help taxpayers with compliance. Reducing the ability to provide customer service is particularly shameless.

For all the complaints about lack of budget funds, the Weekly Standard made note of a particular irony: “The IRS’s total annual $11 billion budget is dwarfed by the amount of improper tax payments it makes each year. According to the report, the IRS paid out $17.7 billion in improper Earned Income Tax Credit payments (which are supposed to help poor and low-income individuals) and an additional $6 to $7 billion in improper child tax credit payments.”

That’s double the amount of the entire IRS budget paid out to taxpayers incorrectly. Perhaps if the same amount of diligence the IRS took when targeting conservatives was paid to processing tax returns properly, there wouldn’t be such whining from the IRS Commissioner. And maybe some more phone calls would be answered.

by | BLOG, ELECTIONS, FREEDOM, OBAMA, POLITICS, TAXES

The vote to confirm Loretta Lynch might happen as early as this week. The process has been stretched out under the auspices of being contingent on passing a human trafficking bill in the Senate, but it is just as likely that the vote was put quietly on hold in a “logjam” until 51 votes were clinched for certain. It has been a struggle to get enough votes throughout the process, with the 51 vote only been secured at the beginning of April. 5 Senate Republicans that were needed are: Sens. Orrin Hatch (Utah), Lindsey Graham (S.C.) and Jeff Flake (Ariz.) — all members of the Judiciary Committee — and moderate Sens. Mark Kirk (Ill.) and Susan Collins (Maine).

Lynch’s opponents have been painted as racist and anti-immigrant. But the most abhorrent reason for nominating Lynch is truly in the realm of civil rights, with the media turning a blind eye to her antics, specifically related to civil asset forfeiture.

The most ironic about the matter is that “Ten civil and human rights organizations, including the National Action Network, which is headed by the Rev. Al Sharpton, the League of United Latin American Citizens and the NAACP wrote a letter to McConnell [last] Friday urging a vote on Lynch.

A couple of months ago, I wrote an open letter decrying the nomination of Loretta Lynch and spelled out her egregious record on the issue of civil rights, which should be chilling for anyone considering her nomination. I will repost it here below, since the media has failed to give any real scrutiny to her time in New York.

The nomination of Loretta Lynch to the position of Attorney General is before you. Although her intelligence, experience, and poise may appear to make her a superb candidate, it is clear now that she would be an extremely poor – even dangerous — choice due to her strong position on civil asset forfeiture.

The need to safeguard civil liberties and individual rights is a priority for all Americans. Do you really want to consider confirming a person who has been exceedingly proud of her record of taking property without due process…of practicing guilty until proven innocent? This is a very serious issue, not to be taken lightly.

Civil asset forfeiture is a particularly egregious abuse of power, allowing the government to seize property and cash if it merely suspects wrongdoing, even with no evidence and no charging of a crime.

Loretta Lynch was particularly lucrative in this regard as the U.S. attorney for the Eastern District of New York. Between 2011 and 2013, the forfeiture operations under her management netted more than $113 million in civil actions. Lynch’s division was among the top in the country for its collections. But this is not something to be proud of.

In one particularly appalling case, Loretta Lynch’s office seized nearly a half-million dollars from two businessman in 2012 and sat on it for more than two years without a court hearing or appearance before a judge. In fact, no crime had been committed. These men were denied due process and deprived of their assets without warning or criminal charges. Lynch suddenly returned the money just weeks ago on January 20, 2015 — on the eve of her confirmation hearings, having found no wrongdoing by the men either.

During Lynch’s confirmation hearing testimony pertaining to civil asset forfeiture, Lynch stated that “civil and criminal forfeiture are very important tools of the Department of Justice as well as our state and local counterparts.” She further argued that forfeiture is “ done pursuant to court order, and I believe the protections are there.” This is, in fact, not true. In the case mentioned above, there was not only no court order, but also no hearing at any time in nearly three years. That is unconscionable. And this is only one of many similar, well-documented, incidents.

The problem of civil asset forfeiture is that the government can confiscate money or property under the mere suspicion of a crime without ever actually charging someone. The person must prove his innocence to reclaim what was seized, which is a burden of time and money and readily seems to go against our staunch American belief of “innocent until proven guilty.” What’s more, besides the obvious threat to civil liberties, those most likely to be victims are poor and minority citizens.

Thankfully, in recent months, individuals and organizations on both sides of the political aisle have come together to demand reform to this unjust practice. Bipartisan legislation has been proposed in Congress; groups ranging from the Heritage Foundation to the American Civil Liberties Union have been increasingly critical of civil asset forfeiture practices. Even Eric Holder has called for changes and the IRS has recently and publicly pledged to reduce its involvement as well.

Loretta Lynch and her record on civil asset forfeiture represents the worst of this “tool for law enforcement”. A vote for her confirmation is a vote you will never be able to walk back. Do you really want to confirm a person who is so deeply committed to civil asset forfeiture at the very same time in America that there is strong bipartisan support for protecting civil liberties and walking back the laws pertaining to this practice? It makes no sense to proceed down this path.

Loretta Lynch may arguably be the most successful forfeiture agent in government today. This is not a positive quality for an Attorney General. The practice is abusive and her tactics even more so. Voting to confirm a person with such an atrocious civil liberties record is certain to cause problems for you down the road when you have to answer for your support. Therefore, on behalf of all Americans, I urge you to vote no for her confirmation.

by | ARTICLES, BLOG, ECONOMY, FREEDOM, OBAMA, POLITICS, TAXES

“Life, liberty, and property do not exist because men have made laws. On the contrary, it was the fact that life, liberty, and property existed beforehand that caused men to make laws in the first place” — Frédéric Bastiat in “The Law.”

If you haven’t read “The Law” yet, you can download it here for free. It is one of the most marvelous works of economics and philosophy.

by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, OBAMA, TAX TIPS, TAXES

If you are an American living abroad — dubbed an “expat” — you are still expected to pay income taxes and file income tax reports to the IRS. The United States is the only country in the world that has this requirement and it is mandatory until and unless one renounces citizenship.

Being an expat in recent years has become more difficult. In 2010, Congress passed FATCA, which was enacted as a means to find foreign accounts of US taxpayers (such as a Swiss bank account). Overseas banks must also report to the IRS any bank accounts held by Americans; this has led to the unintended consequence of many banks choosing not to service expats because of the additional headache for the particular financial institution.

And now compliance has become even more onerous for expats. The IRS has announced the permanent closing its three remaining walk-in offices at the U.S. embassies in London, Paris, and Frankfurt, by the end of the fiscal year. Taxpayers abroad are expected to use the internet for all their tax needs. But woe to the international taxpayer who makes a filing mistake; you can be sure that the IRS will levy hefty fines.

Furthermore, even more simple transactions will be impacted by the office closings:

“For foreign citizens who need an Individual Taxpayer Identification Number (ITIN) to do things like sell property in the U.S. or claim dependents on a U.S. tax return, the process could be even more difficult. Ms. Otto, the accountant, says that when she was based in France, foreigners could get an ITIN by getting a notarized copy of their passport and submitting that with an ITIN application to the IRS at the embassy locations abroad.

But now foreigners who need an ITIN have to mail their passport to an IRS office in the U.S. for verification. “What person in his right mind is going to mail his passport to the IRS?” she asks.”

The number of taxpayers living abroad has grown substantially in the last five years, with some estimates as much as a 50% increase. It is certainly not a time to reduce services to our overseas Americans. However, the IRS sees fit to protest budget cuts by doing that — just not just abroad, but in all facets of customer service to taxpayers.

*To get an idea of tax compliance for expats, check out this very good, comprehensive list of important forms below

Common Overseas Tax Forms

Form 2555 & 2555- EZ: These forms are for calculating your Foreign Earned Income Exclusion (FEIE) and to calculate your Foreign Housing Exclusion or Deduction. If you meet certain foreign residency requirements, you may be able to exclude up to $99,200 of earned income in 2014 and a portion of your foreign housing expenses from U.S. income tax. Note that this exclusion does not apply to self-employment taxes. If you are self-employed abroad, you are still subject to U.S. Social Security taxes unless you live in one of the 25 countries with which the U.S. has a Social Security Totalization Agreement. The FEIE is generally advantageous to use when income tax rates in the foreign country are lower than in the U.S. and/or your total earned income is below the exclusion threshold.

Form 1116: This is the Foreign Tax Credit form and it is used to claim a credit against your U.S. income tax for income taxes paid in the foreign country. This credit applies both to foreign earned income (wages, self-employment income, etc.) and unearned income (interest, dividends, capital gains, rents, etc.). This is generally the most beneficial form to use for residents of countries with high income tax rates, those with children eligible for the additional child tax credit and those interested in contributing to U.S. retirement plans (traditional and Roth IRAs, SEPs, solo 401(k)s, etc.)

FBAR Form FinCEN 114: This form is independent of the tax return and a separate filing requirement. The FBAR applies to any U.S. person who owns, has beneficial interest or signature authority over foreign financial accounts that exceed $10,000 in the aggregate in value at any time during the year. If you have any foreign bank accounts, this also has to be disclosed on Part III of Schedule B, whether the FBAR is required to be filed or not. FinCEN 114 must be e-filed and cannot be mailed, with the absolute filing deadline on June 30, with no extension possible.

Form 8938: This form, also known as the Fatca form, is used to report Specified Foreign Financial Assets and the income derived from them. There is some overlap with the FinCEN 114 Form (FBAR), but the filing thresholds are higher, and depend on the taxpayer’s residency and marriage status, with different thresholds for the highest value reached during the year and on the last day of the year. These thresholds range from a low of $50,000 to a high of $600,000.

Other Overseas Tax Forms

Not every tax preparer will be familiar with the forms described below. If any of these forms apply to your situation, you will need to make sure that your preparer is qualified to do the work. Many of these forms are quite complex and require special training to prepare. The IRS, for example, estimates that each Form 8621 requires almost 17 hours of record-keeping and more than 14 hours to prepare. These are the forms that are most commonly missed or filed with errors. The list that follows is illustrative and not comprehensive:

If you received a gift or inheritance from a foreign person, even though it will generally not be taxable in the U.S., depending on the amount, you may have to report it in Form 3520. This form is also used to report transactions that you had with foreign trusts. If you are grantor in a foreign trust, you are likely required to file Form 3520-A in addition to form 3520.

If you run your own business in a foreign country, you may have established a company to conduct your business. Depending on the entity’s classification for U.S. tax purposes, which will be a corporation by default or will depend on the classification election made through Form 8832, you may be required to file Form 8858 if the entity is disregarded; Form 5471 if the entity is classified as a corporation; or Form 8865 if classified as a partnership. Transactions between you and your foreign company may have to be reported on Form 926.

If you live in a country with which the U.S. has an income tax convention, you may be entitled to certain treaty benefits with respect to your foreign retirement accounts, re-sourcing of certain U.S. source income to avoid double taxation, taxation of foreign social security, etc. The treaty-based positions taken in your return may have to be disclosed in Form 8833.

If you have a brokerage account or other investments (including some foreign retirement accounts) in a foreign country, these investments may be classified as Passive Foreign Investment Companies or PFICs, which are subject to special tax rules that are generally unfavorable in nature. Most foreign mutual funds and ETFs are classified as PFICS. Each PFIC you own is reported on a separate Form 8621.

Other forms that could also apply to your situation include Form 5173: Transfer Certificate which is issued by the IRS upon the death of an American citizen overseas, and is a discharge form confirming that all taxes had been paid and which is often required by banks and brokerage firms to release funds to the estate; Form 5472 for certain U.S. corporations with 25% foreign ownership and certain foreign corporations engaged in a U.S. trade or business; and Form 720, Quarterly Excise Tax Return, to report and pay excise taxes on certain foreign life insurance premiums.

Common Tax Forms – With Some Overseas Components

The following forms are common for U.S. taxpayers but also have some international elements to be aware of:

1040: Ultimately all of your income (foreign and domestic) should end up on your form 1040. Americans married to non-Americans may be able to us the Head of Household filing status instead of married filing separately. In some cases adding a non-citizen spouse (and their income and assets) to the U.S. tax return can be beneficial. All dependents on the return, must have a U.S. tax ID number.

1040: – Schedule A: Some expenses related to being overseas may be able to be claimed as itemized expenses such as certain foreign taxes, certain moving expenses and travel, mortgage interest, medical and dental expenses etc.

1040: – Schedule B: Part III of Schedule B has information related to foreign trusts and foreign bank accounts. Make sure you check these correctly.

1040: – Schedule C. If you live overseas and are self-employed, you will still have to file a Schedule C. You may be subject to U.S. Social Security though Totalization Agreements may negate the need for paying into U.S. Social Security. You will also generally be able to contribute to a U.S. solo 401(k) or SEP IRA but these may not be tax-deferred in the country where you live and work.

For more information about overseas tax returns, you should check the IRS’s website, which has thousands of pages for your reading pleasure in a section dedicated to International Taxpayers. A good starting point for any new overseas American is Publication 54: Tax Guide for US Citizens and Resident Aliens Abroad.

by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, POLITICS

A recent incident involving a woman and police officer in Indiana is a prime example of law enforcement run amok. The woman was arrested and faces charges of resisting arrest — a felony in Indiana — after she failed to immediately pull over her vehicle on a dark country road at night, and instead chose to drive less than a mile down the road to a lit, public parking lot. The woman, acknowledging the police officer with a wave, also put on her hazards as she made her way to a safer area.

The offensive officer, Porter County Sheriff’s Department Patrolman William Marshall, initially flagged her for speeding, but when he approached her in the parking lot after she stopped her vehicle there, he chastised her for not stopping immediately. Reason reported the officer saying, “What in the hell are you doing? I could arrest you for this.” She explained her rationale was safety, but, according to the officer, after she “refused to listen to how her actions put her and others in danger, Marshall said he arrested her.”

The woman, with no prior criminal record, now faces felony charges, while Patrolman William Marshall is being fully supported by his county’s sheriff’s department. The department “cited state law requiring motorists to yield to emergency vehicles and said Marshall was driving a fully marked squad car and used the lights and siren.” Never mind that the woman did acknowledge the officer; her crime was that she picked a safe, public, and well-lit parking lot instead of a dark, isolated, country road for her interaction.

Patrolman William Marshall deserves to have disciplinary action taken against him for this egregious incident. To arrest someone for not immediately pulling over a vehicle in order to ensure personal safety and liberty is contemptuous, audacious, and just plain spiteful. Such behavior is not honorable and is unbecoming of any officer. Patrolman William Marshall must be held accountable for his actions.

by | ARTICLES, BLOG, ECONOMY, FREEDOM, OBAMA, TAXES

It’s frustrating when popular TV economists perpetuate economic myths that have been thoroughly debunked. Last week, Becky Quick, host of CNBC’s “On the Money”, interviewed Bethany McLean, Contributing Editor over at Vanity Fair. They discussed the subject of equal pay for women; unfortunately, they both asserted that women only earn 77% of pay that men do, a charge that is simply untrue, but endlessly repeated.

Factors such as education paths, child bearing choices, hours worked, and job risk are not always equal for men and women. Taking these items into consideration, the gender wage gap shrinks almost entirely, with likely no more than a 5% variance. This is also supported by the simple economic reality that if women actually did make 23% less than men in wage costs, businesses would almost entirely hire women as a means to minimize labor costs and maximize profits. Since this does not actually happen, it is obvious that the 23% wage disparity is merely a distortion perpetuated by the Left, and most notably by the White House.

It’s one thing for partisan politicians to spew such nonsense, but for an economics reporter to peddle it as well is absolutely irritating and reckless. She should know better.