by | ARTICLES, BLOG, BUSINESS, FREEDOM, GOVERNMENT, OBAMA, TAXES

The Tax Foundation released its first global stat called the “International Tax Competitiveness Index”. This index aims to measure two criteria, competitiveness and neutrality, by examining “the extent to which a country’s tax system adheres to”, these “two important principles of tax policy”.

The Tax Foundation released its first global stat called the “International Tax Competitiveness Index”. This index aims to measure two criteria, competitiveness and neutrality, by examining “the extent to which a country’s tax system adheres to”, these “two important principles of tax policy”.

The index accounted for more than 40 tax positions and policies. In their analysis, two of the most damning reasons for ranking the United States near the very bottom of the list include the highest corporate tax rate (39%), as well as the “rare demand that money earned overseas should be taxed as if it were earned domestically”. As such, the United States outranked out only Portugal and France and was placed 32 out 34 industrialized nations.

The concept of “competitiveness” is described as one that “limits the taxation of businesses and investment”. The Tax Foundation acknowledges that heavy taxation runs the risk of the flight of capital and business location. This is turn drives “investment elsewhere, leading to slower economic growth.” We are seeing this is the growing popularity of business inversions, which is driving President Obama and Sen. Chuck Schumer to create punitive legislation on business that wish to leave. Ironically, if they are successful, the WSJ notes, ” the U.S. could fall to dead last on next year’s ranking. Now there’s a second-term legacy project for the President.”

Not only are corporate taxes the highest on this list of 34 countries, it is pretty much the highest in the entire world:

The accounting firm KPMG maintains a corporate tax table that includes more than 130 countries and only one has a higher overall corporate tax rate than the U.S. The United Arab Emirates’ 55% rate is an exception, however, because it usually applies only to foreign oil companies.

The other major concept besides competitiveness that shaped the overall index rankings is the concept of “neutrality”. Neutrality is characterized as “a tax code that seeks to raise the most revenue with the fewest economic distortions. This means that it doesn’t favor consumption over saving, as happens with capital gains and dividends taxes, estate taxes, and high progressive income taxes. This also means no targeted tax breaks for businesses for specific business activities.” These various forms of taxation, as well as the massive crony capitalism enterprises widely seen in the United States, are found to “misallocate capital and reduce economic growth”. This factored heavily into the low ranking that the United States received.

The United States is falling behind around the world:

“Liberals argue that U.S. tax rates don’t need to come down because they are already well below the level when Ronald Reagan came into office. But unlike the U.S., the world hasn’t stood still. Reagan’s tax-cutting example ignited a worldwide revolution that has seen waves of corporate tax-rate reductions. The U.S. last reduced the top marginal corporate income tax rate in 1986. But the Tax Foundation reports that other countries have reduced “the OECD average corporate tax rate from 47.5 percent in the early 1980s to around 25 percent today.”

This new index ranking should be a wake-up call and a springboard for discussion about much-needed tax reform. Our tax code is byzantine, our businesses are over-taxed, and our economy is continuing to suffer. Our reputation should not be, “At least we beat France!” We can do better. We have done better. We deserve better.

by | ARTICLES, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

The government is still running more than a half-trillion dollar deficit right now, with one month left to go in the fiscal year, despite record revenue being hauled in.

CNSNews reports that “Inflation-adjusted federal tax revenues hit a record $2,663,426,000,000 for the first 11 months of the fiscal year this August, but the federal government still ran a $589,185,000,000 deficit during that time, according to the latest Monthly Treasury Statement.”

Thus, the government is still over-spending, to the tune of $3,252,611,000,000 in total expenses so far this year.

Here’s the breakdown of revenue:

Individual income taxes: $1,233,274,000,000

Corporate income taxes: $247,200,000,000

Employment and general retirement (off-budget): $674,338,000,000

Employment and general retirement (on-budget): $209,281,000,000

Unemployment insurance: $54,591,000,000

Other retirement receipts: $3,155,000,000

Excise taxes: $73,051,000,000

Estate and gift taxes: $17,702,000,000

Customs duties: $30,902,000,000

Miscellaneous receipts: $119,933,000,000

So just remember, the problem isn’t enough tax revenue or underfunded programs — it’s that the government can’t seems to stay on budget or within its revenue receipts. All this overspending does is just continue to add to the growing deficit.

by | ARTICLES, CONSTITUTION, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

Thanks to the folks over at CATO, we have a video of the current IRS Commissioner John Koskinen, speaking before the Ways and Means Health Subcommittee early this week. He was being questioned about taxes and Obamacare, and asked about subsidies being repaid.

Chairman Brady said, “The law in that case is that there is not a cap. Subsidies must be repaid. Will you be following the law in that recapture?”

Koskinen replied, “Yes, wherever we can, we follow the law.”

In other words, following the law is a “can”, not a “must”.

With regard to Koskinen’s remarks, Forbes had an interesting observation:

“Numerous Treasury and IRS staffers have told investigators from the House Committee on Oversight and Government Reform that they knew back in 2011 that the Patient Protection and Affordable Care Act didn’t authorize them to issue health-insurance subsidies through Exchanges established by the federal government. But they did so anyway. (And now they’re in court.) The Wall Street Journal‘s Kim Strassel writes about it here.

Given that context, Koskinen’s remark seems like an admission that the IRS sees the law more as a set of guidelines”.

Indeed. I wonder if anyone was to get audited by the IRS, that they could use the phrase “Wherever we can, we follow the law” successfully in their defense.

by | ARTICLES, BLOG, ECONOMY, OBAMA, POLITICS, TAXES

At least you can say Bernie Sanders is ideologically consistent. The self-proclaimed socialist unabashedly declared on Saturday that “we need a tax system which asks the billionaire class to pay its fair share of taxes and which reduces the obscene degree of wealth inequality in America.” It was particularly fitting that the speech was at an AFL-CIO convention.

Over on his Senate page, Sander’s posted his proposal — “a progressive estate tax on the wealthiest Americans”:

“For those who would pay more, the tax rate on estates valued from $3.5 million to $10 million would be 40 percent. There would be a 50 percent tax on estates worth $10 million to $50 million and a 55 percent levy on estates worth more than $50 million. A 10 percent surtax would be applied on estates worth more than $1 billion, a category that today includes fewer than 500 American families. The bill also would close estate tax loopholes that have allowed the wealthy to avoid an estimated $100 billion since 2000.

His rationale? Sanders said that this is “the fairest way to reduce wealth inequality, lower the $17 trillion national debt and pay for investments in infrastructure, education and other neglected national priorities.”

Notice he said fairest — not most efficacious — way to reduce wealth inequality. Because the actual amount raised on such a tax will be negligible for any real deficit reduction, hopefully such a foolish proposal will never be implemented.

Unfortunately, with any sort of supertax, the truest and most invisible effects will be felt in the economy. The confiscatory nature of a high estate tax is among the worst offenders. “The economic incidence of the death tax is far broader, because it causes many wealthy individuals to save less, choosing instead to retire early or, as Milton Friedman put it, “dissipate their wealth on high living.” This reduction in savings means a concomitant reduction in investment, lessening the flow of capital to businesses and organizations where countless ordinary Americans are employed.”

And yet, Sanders sees nothing “obscene” about the another kind of wealth inequality: the salary and benefits of Congress, which, at $286K, is about 95% greater than what average Americans earn. Or still yet, another kind of wealth inequality: the $17 trillion government debt and spending problem that he is purporting to fix by his punitive tax proposal.

by | ARTICLES, ELECTIONS, GOVERNMENT, OBAMA, POLITICS, TAXES

The idea of “disparate impact” is a cancer that has taken root in the business world. If we do not focus on substantially curbing or ending it, it will continue to grow, extorting huge sums from innocent companies, creating an enormous economic burden on society, and allowing the tort bar to run amok.

There are many areas in business where charges of “discrimination”, often regarding race, could and are being made every day. Employment and mortgage origination are two of the most prevalent. The law requires – as it should -that for a company to be guilty of such discrimination, there must be an intent to discriminate.

But government agencies have found a way to overrule that requirement by developing the idea of “disparate impact”. Disparate impact is the concept which allows if a protected class of citizens has a statistically lesser representation with respect to a business (hiring, mortgages origination, etc) it may be implied that the business has intentionally discriminated — because there is an adverse impact as a result. This is clearly irrational, since there may be many economic, societal, and local reasons for the particular statistical representation. Unfortunately, disparate impact puts the burden to show lack of discrimination on the employer, meaning he is guilty until proven innocent. In fact, in order for an employer to defend himself against such a charge, he would have to show that the “offending rule or practice” was a “business necessity”.

Though I find this concept outrageous, the federal and state governments and their agencies seem to love it lately. I therefore believe that they should be equally adamant in applying the concept of disparate impact in the public sector.

The IRS scandal has shown the clear practice of targeting conservative groups applying for 501c4 status (despite the subsequent cover up). By applying disparate impact theory to this situation, the charge of intentional discrimination would most certainly apply because there is no “business necessity” in the policy the IRS employed.

The Obama administration, having complete control and responsibility for the Department of the Treasury and its Internal Revenue Service is therefore guilty of such intentional discrimination. In particular, President Obama’s specific response, that there has been no evidence that anyone directed anyone to intentionally target conservatives, does not insulate him from being actually guilty.

The current administration has been keen on applying disparate impact theory to a number of private companies, and appears intent on ramping up the practice. For example, Obama’s labor secretary pick, Thomas Perez, has been particularly lucrative in this regard. Last summer, National Review Online (NRO) covered some of Perez’s cases in recent years, noting that Perez “has applied that theory vigorously to force large settlements from financial companies even in cases where there was no evidence of actual racial discrimination”. In other words, employers can be sought after for violating the law whether or not they intended to do wrong.

The White House in general, and Perez in particular, like disparate impact theory because it, as NRO notes, it “sets a very low bar for proving discrimination. Under it, prosecutors need not prove intent, merely that minorities have suffered a disparate impact from some action”. And this is a person Obama added to his Presidential Cabinet.

If disparate impact can be applied to the private sector, it should also — in the spirit of fairness and equality, of course — be applied to the IRS. Particular groups were adversely singled out and subject to excessive, burdensome, and overreaching scrutiny; of this we are certain. The targeting of conservatives was a concerted effort to slow down or dissuade the creation of their tax-exempt groups. Even if we no longer have tangible evidence of a White House link because of lost, missing, or destroyed emails and Blackberrys, it doesn’t really matter anyway under disparate impact theory. Intent needs not to be proved in court; merely the act of discrimination is enough.

Based on the White House’s unmitigated belief of their ability to use disparate impact against companies for questionable practices, the rule should be applied to the IRS for its questionable practices as well. Since the IRS falls directly under the purview of the Executive Branch, why is the President of the United States therefore not directly responsible and culpable for the IRS abuse?

by | BLOG, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

In a moment of recent hand-wringing, the Fed examined the question of why inflation has stayed extremely low in the United States despite all the efforts of quantitative easing money pumping. Their answer: American consumers are mainly to blame.

Yes indeed. In a paper released this week by the St. Louis Federal Reserve, the Fed cites “low level of money movement in large part on consumers and their “willingness to hoard money.”. To be fair, the paper also criticized its own policies as well, suggesting that the has they have “reinforced the recession” with their “excessively low interest rate policy”.

However, “hoarding money” is seen as the main culprit and attributable to two factors:

A (gloomy) economy after the financial crisis.

The dramatic decrease in interest rates that has forced investors to readjust their portfolios toward liquid money and away from interest-bearing assets such as government bonds

The use of the word hoarding is key to understanding the contempt here. They didn’t say “willingness to save money”, they said “willingness to hoard money”. Saving would imply prudence while hoarding implies selfishness, carefully guarded. It’s like a petulant temper tantrum: why won’t you spend your money for the good of the economy?!

Equally stunning is the lack of discussion with regard to investors. They point out that investors aren’t investing in interest-bearing assets “such as government bonds” but completely omit the reality that investors aren’t investing in businesses either. This is a result of the anti-business climate which is displayed by the current administration.

People used to spend their money investing in or even starting small businesses. That was the backbone of America. It’s not so much anymore. This administration has been exceedingly heavy-handed in its efforts to demonize businesses, while promising that businesses will be highly taxed and regulated. Additionally there have been huge increases in both criminal rules and regulations about what businesses are allowed and not allowed to do, along with a litigation-friendly environment.

All anyone ever reads in the paper is that the government is spending their time and money going after businesses and penalizing them, so much that we are truly becoming dissuaded from going into business.

A few months ago, I wrote about the liberty of risk after the WSJ posted an article by Ben Casselman, who noted the very real decline of risk-taking in business ventures. It is this downward trend which is a major contributor to the fact that the recovery from the recent recession is so painfully slow and anemic. The people’s appetite for investing has been totally decimated by the war on businesses being waged.

And don’t forget, we apparently have lost our appetite for spending too, because we “hoard money” these days (whatever is leftover in a paycheck to actually be able to hoard, that is) in this “gloomy economy”.

by | ARTICLES, GOVERNMENT, OBAMA, TAXES

Thomas Perez’s recent appearance on “On the Money”, proved his economic naivete once again. It begs the question as to how he can be the head of the Department of Labor?

When asked about inversions, he used an anecdote to set the tone of the discussion. It was about a Fortune 500 Exec who (anonymously) proclaimed “I’d rather be rich than right!” implying that a) these people were willing to do the “wrong thing” to make money and b) that inversions are wrong in general.

By implying inversions are wrong, Perez completely and conveniently ignores the fact that our tax laws currently make taxes lower when a foreign corporation owns a US business than when a US company owns that same business. How stupid is that! That not only provides incentive for US companies to do inversions, but it incentivizes US companies to sell out to foreign owners. Stated differently, it is more profitable for a foreign company to own a US company, than it is for a US entity to own that same company. The law then actively promotes the movement of multinational headquarters out of the US, taking untold numbers of jobs with them.

Only someone who is both economically ignorant and politically partisan could support this status quo, and Thomas Perez fits the bill. Perez as the head of the Department of Labor is in charge of improving the situation for workers – but by his actions, he makes it much worse. He should be making it a priority to advocate for change in our tax policy to make it more friendly for our companies in the United States, not for their foreign competitors.

by | ARTICLES, ECONOMY, FREEDOM, GOVERNMENT, HYPOCRISY, OBAMA, POLITICS, TAXES

Just like the recent rise of business inversions — moving business HQ abroad — the United States has seen an uptick (up 221%) in Americans renouncing their citizenship. The elephant in the room in both these cases is taxes: both high taxes and burdensome tax compliance in foreign jurisdictions.

Instead of facing the problems directly, the Obama Administration has resorted to punitive measures. The shame and blame tactic of calling out businesses who wish to relocate as “unpatriotic” was undignified. Perhaps realizing that using the same strategy with individuals would be even less well received, they went the more quiet, direct route: yesterday, the State Department announced their interim final rule that raises the fee for renouncing citizenship from $450 to $2,350.

Their justification for raising the fee is the time and labor involved in the process; that is, the bureaucratic red tape that they created, and then decide to charge exhorbitant fees for:

“The CoSM demonstrated that documenting a U.S. citizen’s renunciation of citizenship is extremely costly, requiring American consular officers overseas to spend substantial amounts of time to accept, process, and adjudicate cases. For example, consular officers must confirm that the potential renunciant fully understands the consequences of renunciation, including losing the right to reside in the United States without documentation as an alien. Other steps include verifying that the renunciant is a U.S. citizen, conducting a minimum of two intensive interviews with the potential renunciant, and reviewing at least three consular systems before administering the oath of renunciation. The final approval of the loss of nationality must be done by law within the Directorate of Overseas Citizens Services in Washington, DC, after which the case is returned to the consular officer overseas for final delivery of the Certificate of Loss of Nationality to the renunciant. These steps further add to the time and labor that must be involved in the process. Accordingly, the Department is increasing the fee for processing such requests from $450 to $2,350. As noted in the interim final rule dated June 28, 2010 (77 FR 36522), the fee of $450 was set substantially below the cost to the U.S. government of providing this service (less than one quarter of the cost). Since that time, demand for the service has increased dramatically, consuming far more consular officer time and resources, as reflected in the 2012 Overseas Time Survey and increased workload data. Because the Department believes there is no public benefit or other reason for setting this fee below cost, the Department is increasing this fee to reflect the full cost of providing the service. Therefore the increased fee reflects both the increased cost of the provision of service as well as the determination to now charge the full cost.

Interestingly enough, if you compare the cost of renunciation in the United States to the cost of renunciation in other countries, the new fee puts the United States way above others. You can check out this handy chart here. The next two highest are Jamaica ($1,010 in US dollars), and Sierre Leone ($663 in US dollars).

So those who wish to renounce their citizenship get to buy their freedom by paying a 422% fee increase for the express privilege of dealing with United States bureaucracy one final time.

This is considered an administrative fee, issued by the State Department, but it is essentially an unofficial “exit tax” for regular citizens. But there is a real one too. As Forbes notes, “To leave America, you generally must prove 5 years of U.S. tax compliance. If you have a net worth greater than $2 million or average annual net income tax for the 5 previous years of $157,000 or more for 2014 (that’s tax, not income), you pay an exit tax”.

So for those who have done well in the United States, besides the higher administrative fee/exit tax, you get to pay that real “exit tax” knows as the 877A.

Alas, this isn’t the first time those wishing to leave have been targeted. A bigger, punitive measure was attempted in 2012 by Senators Chuck Schumer and Bob Casey. When the co-founder of Facebook, Eduardo Saverin, renounced his U.S. citizenship as a means to save millions in taxes before Facebook went public, the Senators reacted by proposing the “Ex-PATRIOT Act” of 2012 that essentially doubled the exit tax for high worth individuals. “People who could not prove another reason for renouncing citizenship would face a 30% tax on future capital gains on U.S. investments – twice the current 15% rate – and be barred from receiving a visa to enter the country.” Thankfully the bill died in committee the first year, and did not advance out of the Senate in 2013.

Though this new fee hike is different than the standard exit tax, and on a much smaller scale (dollars-wise), it speaks the same language: punish. All this fee hike does is prove that that current administration would rather squeeze U.S. citizens for more revenue, thus likely reiterating to those renouncing their citizenship that being a U.S. citizen lacks much of the value that it once did. And that is a very sad thing.

by | ARTICLES, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

According to the Treasury Inspector General for Tax Admininstration (TIGTA), the 2.3% medical device excise tax enacted to help pay for Obamacare is not meeting targets.

The tax went into affect January 1, 2013. The TIGTA report analyzed the returns for the first two quarters (6 months) of 2013, and found that the “excise tax revenue being reported are lower than estimated” for a total of $913.4 million. The IRS expected to have received “excise tax revenue of $1.2 billion for this same period.”

The report also states that the “Joint Committee on Taxation estimated revenues from the medical device excise tax of $20 billion for Fiscal Years 2013 through 2019.”. And yet, in the first six months alone, the estimate amounts are off by 25%. That does not bode well.

Many of the problems originate in the IRS. In fact, the report is aptly named “An Improved Strategy Is Needed to Ensure Accurate Reporting and Payment of the Medical Device Excise Tax”. Some of the key findings:

“The IRS is attempting to develop a compliance strategy to ensure that businesses are compliant with medical device excise tax filing and payment requirements and has taken several measures to advise medical device manufacturers of the new excise tax. However, the IRS cannot identify the population of medical device manufacturers registered with the Food and Drug Administration that are required to file a Form 720 and pay the excise tax.”

“In addition, processing controls do not ensure the accuracy of medical device excise tax figures reported on paper-filed Forms 720. Our analysis of 5,107 Forms 720 processed for the quarters ending March 31 and June 30, 2013, identified discrepancies in the amount of the medical device excise tax and/or taxable sales amount captured from 276 paper‑filed tax returns. TIGTA identified medical device excise tax discrepancies totaling almost $117.8 million when comparing the excise tax amount captured by the IRS from the Form 720 to the excise tax amount TIGTA calculated.”

And the most interesting:

“Finally, the IRS erroneously assessed 219 failure to deposit penalties totaling $706,753 against businesses filing a Form 720 for the quarters ending March 31 and June 30, 2013, which was designated a penalty relief period. The IRS had reversed 133 of the 219 penalty assessments. When TIGTA alerted the IRS of the remaining 86 penalties, IRS management reversed the penalties and issued apology letters to the affected taxpayers.”

The IRS, it seems, was unprepared to handle the collection of excise tax, and furthermore, did not seems to understand basic reporting and penalty relief periods of which it was put in charge.

Think about this: we are now in August of 2014. That means that the second half of 2013 and the first half of 2014 went by before the TIGTA report was released with its findings. If the first 6 months of revenue were found to be about 25% under estimate, it is likely the trend continued for the next full year.

The IRS did agree to the findings of the TIGTA report. However, the summary does not leave one feeling confident that there will be swift resolution now that the problems have been discovered and dissected. Note the ambiguity and qualifiers:

The IRS agreed with our recommendations and plans to consider alternative strategies for identifying noncompliant manufacturers, identify programming changes needed to improve the math verification for paper-filed Forms 720, and implement procedures for corresponding with taxpayers if the changes can be accomplished within budgetary constraints.

Never mind the fact that the Affordable Care Act passed in March 2010 with the excise tax being a key, but controversial, revenue-raiser. The IRS had nearly three years to come up with a) a system to identify companies who owed the tax and b) a system to process the associated forms. And it couldn’t do it.

With the tax being so controversial from the get-go, there have been measures in Congress calling for its repeal because of its impact on the cost of devices and well as jobs in the medical device field.

“The medical device industry has been lobbying hard to get the tax repealed, and there has been movement in Congress. Both the House and the Senate have passed separate pieces of legislation calling for the tax to be repealed, though the Senate vote was on a nonbinding resolution.”

The problem at this point with excise tax repeal is the question of how to make up for even more lost revenue to pay for Obamacare. Taxpayers should be indeed be nervous that the tax collection is showing to be only 75% and we actually have no idea if it improved or worsened at all over the following year because data is not available for it.

The only thing we do know is that we are certain to see a premium rate increases this coming year because the projections have been so off-estimate.

by | ARTICLES, BLOG, ECONOMY, FREEDOM, GOVERNMENT, HYPOCRISY, OBAMA, POLITICS, TAXES

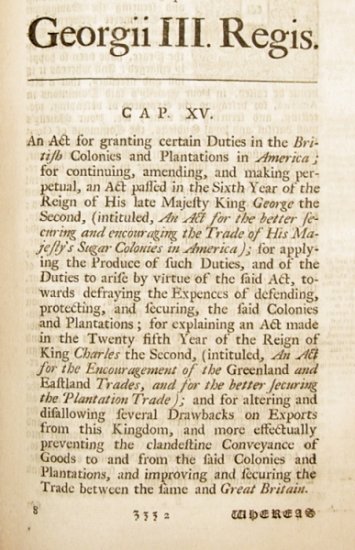

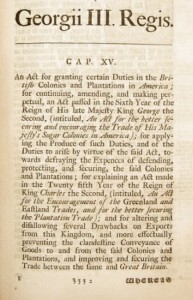

On April 5, 1764, Parliament passed something called “The Sugar Act”, which, interestingly, had another name: “The American Revenue Act”. It was a modification of the 1733 Molasses Act, and it also affected other goods, such as wine and coffee.

The Preamble to this Act states: “it is expedient that new provisions and regulations should be established for improving the revenue of this Kingdom … and … it is just and necessary that a revenue should be raised … for defraying the expenses of defending, protecting, and securing the same.”

The Sugar Act/American Revenue Act, therefore, was a revenue raising measure (and not just a regulation measure), whose revenue was intended to help defray the costs of defending the colonies during the 7 Years War which ended in 1763. Instead, it wreaked havoc in the colonies:

“The situation disrupted the colonial economy by reducing the markets to which the colonies could sell, and the amount of currency available to them for the purchase of British manufactured goods. This act, and the Currency Act, set the stage for the revolt at the imposition of the Stamp Act.”

Fast forward to 2014. A new measure was introduced by Rep. Rosa deLauro called the SWEET Act, also known as the “Sugar-Sweetened Beverages Tax” — a proposed tax of “one cent per teaspoon – 4.2 grams – of sugar, high fructose corn syrup or caloric sweetener”.

The Act sounds eerily like a revenue-raiser, much like its ancestor, the Sugar Act. From the text of the SWEET Act:

“This Act is intended to discourage excessive consumption of sugar-sweetened beverages by increasing the price of these products and by creating a dedicated revenue source for programs and research designed to reduce the human and economic costs of diabetes, obesity, dental caries, and other diet-related health conditions in priority populations”

Let’s compare:

Sugar Act: “improving the revenue of this Kingdom”… “just and necessary that a revenue should be raised”… “for defraying the expenses of defending, protecting, and securing the same.”

SWEET Act: “dedicated revenue source for programs and research”… “to reduce the human and economic costs of diabetes, obesity, dental caries, and other diet-related health conditions”.

Same over-reaching thinking, different government.

As a response to the Sugar Act in May 1764, Samuel Adams drafted a report on the Sugar Act for the Massachusetts assembly, in which he denounced the act as an infringement of the rights of the colonists as British subjects:

For if our Trade may be taxed why not our Lands? Why not the Produce of our Lands & every thing we possess or make use of?

”

Will there also be a similar rebuke over the Sweet Act of 2014? The Sugar Act was subsequently repealed in 1766 because it was such a disastrous piece of legislation. Let’s hope history doesn’t repeat itself and the SWEET Act never comes to fruition.