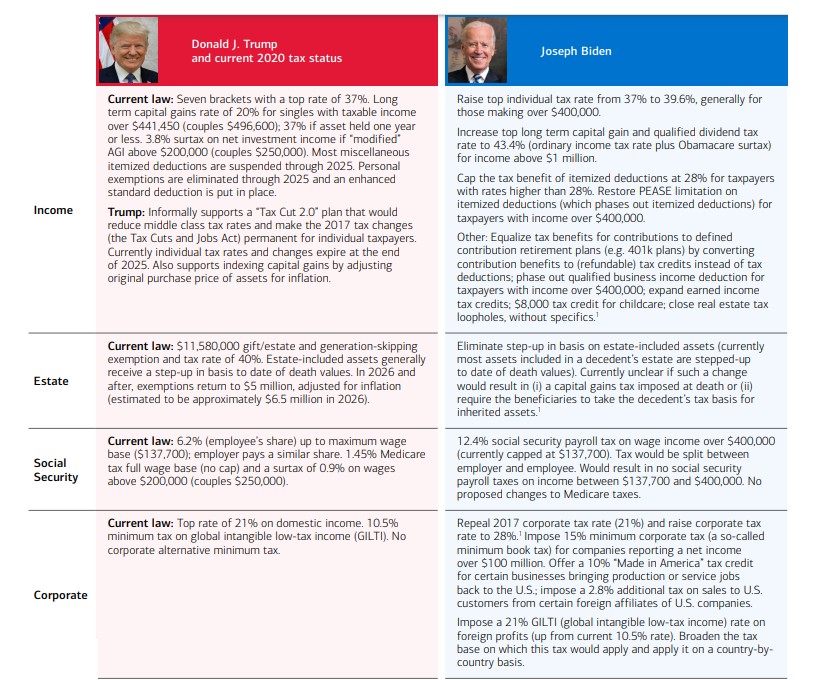

Now that Biden has been elected President, it’s important to take stock of what tax changes are likely to be coming. Merrill Lynch did a good job putting together a side-by-side comparison of current tax law in four areas: income, estate, social security, and corporate, and then possible changes in those areas according to Biden’s campaign tax plans. The summary is below.

It is notable that in just about every instance, there will be a tax increase under Biden’s plans. How this will impact the economy, jobs, wages, and investments remains to be seen.

I was shocked to read “Get Ready for the Biden Stock Boom” in the pages of the Wall Street Journal, written by a former editor of Barron’s, no less. Ed Finn really, really wants you to support Joe Biden and his article is full of so much wishful thinking that it reads like a Disney Fairy Tale — except in reality, there will be no happy ending.

To be fair, Ed Finn does acknowledge that the stock market will certainly experience some turbulence if Joe Biden is elected — but that’s because smart investors know that socialist policies are coming in the form of higher taxes, strangling regulation, and ridiculous legislation such as the “Green New Deal.” You think Obama was bad for the economy? Wait until Biden gets in there.

Yet after laying out the coming economic reality, Ed Finn still wants you to believe in Joe Biden, and the rest of his analysis is basically dependent on the word IF. You can’t make this up:

“IF a President Biden can control the federal budget deficit, IF he can forge better relationships with America’s trading partners, IF he can reverse some of President Trump’s anti-immigration policies, IF he can bring a less combative atmosphere to Washington and the nation, there is no reason to think that during his term average annual stock returns, including dividends, can’t be in the 10% range, as they have for the past 95 years.”

It should be noted that even with all the “if’s” coming true, they have no positive economic consequence. They would be nice, but not economically powerful.

How does he spell out how Joe Biden’s going to improve the economy: “Given Mr. Biden’s ambitious plans to use increased tax revenue to fund more spending on green energy, health care and infrastructure, it’s conceivable he could spur the U.S. economy enough to push annual stock returns to 15%.” Ed Finn must think that the readers of the Wall Street Journal are stupid. To think that anything relating to “green energy” isn’t detrimental to the economy is economically illiterate. We already have efficient fossil fuels, but the Democrats would happily pay three times as much for less energy to be environmentally woke — and that’s supposed to improve the economy? That’s either ignorant or socialist or both. And see how Finn continues to use wishful language: “it’s conceivable he could spur the U.S. economy enough to push annual stock returns to 15%.” That’s because neither Finn’s analysis nor Biden’s policies are actually grounded in any sort of economic reality, only fantasy.

On the other hand, what we do know is that there are multiple policy proposals that WILL have negative economic consequences, none of which will come close to offsetting any of the rosy positives that Finn is pinning his hopes on. The main threats Biden poses to the stock market are increased regulation and higher taxes. Increased regulation will inevitably result in slowed economic growth, and with that decreased profits and a less robust stock market. But that’s not even the worst of it. Two specific initiatives will affect the stock market both in the short- and long-term: 1) Raising taxes on corporate profits from 21% 28% and 2) Nearly doubling the capital-gains tax from 20% to 39.6% on income over $1 million/year — and don’t forget the investment-tax surcharge of 3.8%! Of course, Biden plans to raise taxes on nearly every taxpayer regardless.

Ed Finn ought to be ashamed for penning such an unrealistic economic outlook with Joe Biden at the helm. Increased taxation, crushing regulation, and impudent legislation never improves the economy or the lives of the American people.

I was disappointed to read “How the Bidens Dodged the Payroll Tax” last week in the WSJ, not because Biden is a good guy, but because the author of the screed, Chris Jacobs, gets it all wrong. Those of you who read my columns regularly know that I’m no fan of Biden, but in this case, Biden is in the right. There is nothing legally wrong with how he structured and paid his taxes – to the contrary, it elucidates an ongoing tax inequity that was completely missed in the article.

In order to understand what Biden did and didn’t do, you need to understand a little bit about s-Corps, LLCs, partnerships, and Social Security taxes. Foremost is that Social Security taxes are imposed on individuals’ earned income – salaries for employees and earned business income for independent earners. It is a tax on earned income — and only earned income. It’s money contributed from your work that goes into your retirement social security pension, not your business profits, interest and dividends income, capital gains or anything else. Social security is calculated from your working history, because you are taxed only on your earned income. That’s why it’s dubbed the payroll tax.

So now let’s look at some different scenarios. Say you work for a business operated as a C corp or S corp, and you also are a stockholder in that business. The money you get as a stockholder — such as dividends–is not working income so you do not pay the Social Security tax. But the money you earn on your labor for your work in this company – salary – up to $137,700 (for 2020)- is subject to the social security tax.( Amounts earned over the $137,700 is still subject to the much smaller Medicare Tax).

But it gets more complicated when you consider partnerships (or LLC’s which are taxed as partnerships). If you work for and are also an owner of a partnership, your share of the partnership income – both for your labor and share of profits are included in one number reported to you on a K-1 form. And the full amount is subjected to the social security tax. For instance, say you are a 50% owner of an architecture partnership and the firm makes $2 million, you would get a K-1 form showing $1 million. Though that would be for both labor and profit, you would have to pay Social Security tax on the full amount.

But if you are structured as an s-Corp, you pay yourself a salary. If the architecture firm were an s-Corp and it earned $2 million and each shareholder received a $400K salary and netted $600K in profit, they only pay the Social Security tax on the earned income, the $400K. And this is exactly what Biden did. He paid tax on his earned income.

So with an S-corp, you have cleared defined salary and (hopefully) profits. It is conceivable that, in Biden’s case, his salary was too low. That is a bit unclear. But what is absolutely clear is that the business is not all labor and therefore he should not be paying Social Security on the full amount. The problem, therefore, isn’t that Biden did something wrong or that he used an S-Corp “loophole” to “get away with” only paying tax on some portion of the business. The problem is that just because someone is a business owner should not mean that he has to pay social security tax on his business profits. Remember Social Security is a tax only on earned income and thus Biden rightly paid the Social Security tax only on his salary. The real problem is that partnerships, unlike their C-corp and S-corp counterparts, have to unjustly pay the full Social Security tax on both their labor and profits. This is the real problem with the tax code that has needed reform for many years. Biden and Trump would do well to address this inequality in the future.

“…the current vice president…talks like the sort of guy who sits right next to you on the bus even though there are plenty of empty seats — just so he can explain how squirrels aren’t mammals.”

Indeed, in many respects, he’s as close as American politics gets to a wacky sitcom character who’s a couple fries short of a Happy Meal.