by | ARTICLES, BUSINESS, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

The Government Accountability Office (GAO) released a new study that monitored Obamacare subsidy payments. The results are sobering; billions in payments were made to individual Obamacare users which may have been the result of fraud.

The Centers for Medicare and Medicaid Services (CMS) uses information from three agencies in order to verify Obamacare eligibility; they are the IRS, DHS, and SSA. But if there are inconsistencies within the data, the system doesn’t necessarily catch them, resulting in the misallocations. From the report:

“About 431,000 applications from the 2014 enrollment period, with about $1.7 billion in associated subsidies for 2014, still had unresolved inconsistencies as of April 2015—several months after close of the coverage year.”

These findings correspond to other reports over the last couple of years which found similar problems. They were summarized by ATR, below:

- “An auditor’s report examining Minnesota’s Obamacare exchange found the exchange enrolled more than 100,000 individuals who were ineligible for the program. In all, the audit estimated an error rate of close to 50 percent, and the state overpaid up to $271 million over the five-month period that was analyzed by auditors.

- A December 2015 report by the Health and Human Services Inspector General (HHS OIG) found that CMS relied entirely on data from health insurers to verify whether enrollees had paid their premiums and were eligible. However, this data was completely insufficient – insurers provided payment information on an aggregate rather than enrollee-by-enrollee basis, making verification all but impossible.

- A October 23, 2015 report by GAO found that Obamacare exchanges (both state and federal) were failing to verify key enrollment information of applicants including Social Security numbers, household income, and citizenship.

- A September 1, 2015 report by the Treasury Inspector General for Tax Administration (TIGTA) found that Obamacare exchanges are failing to provide adequate enrollment information to the IRS for proper payment and verification of tax credits.

- An August 2015 report by HHS OIG found that the federal exchange is failing to verify Social Security numbers, citizenship, and household income of Obamacare applicants. As a result, the exchange is unable to verify whether applicants are properly receiving tax credits.

- A July 16, 2015 audit by GAO found that 11 of 12 fake ‘test’ applicants received coverage for the entire 2014 coverage period despite many using fraudulent documents, and others providing no documentation at all. From these 11 applicants alone, Healthcare.gov paid $30,000 in tax credits.

- A June 16, 2015 report released by the HHS OIG found that $2.8 billion worth of Obamacare subsidies and payments had been made in 2014 without verification.

- A June 10, 2015 TIGTA report found the IRS failed to properly administer nearly $11 billion in Obamacare tax credits.

- A May 21, 2015 report by TIGTA found that the IRS failed to test Obamacare processing and verification IT until a week before the filing season began.”

How much more mismanagement can we take? This latest report is just one of many highlighting the string of Obamacare failures — unfortunately at the expense of the taxpayer once again.

by | ARTICLES, BLOG, GOVERNMENT, OBAMA, POLITICS, TAX TIPS, TAXES

With Bernie Sanders doing well against Hillary Clinton for the Democrat nomination, it’s a great time to look at some of the specifics of his tax plan. The Tax Foundation studied the affects of the major changes (listed below). Their analysis found that Sander’s plan will reduce typical income by more than 15% while simultaneously hiking taxes by the trillions and shrinking the GDP by nearly 10% over the next decade.

First, Sander’s plan highlights:

Individual Income Tax Changes

–Adds four new income tax brackets for high-income households, with rates of 37 percent, 43 percent, 48 percent, and 52 percent.

–Taxes capital gains and dividends at ordinary income rates for households with income over $250,000.

–Creates a new 2.2 percent “income-based [health care] premium paid by households.” This is equivalent to increasing all tax bracket rates by 2.2 percentage points, and would raise the top marginal income tax rate to 54.2 percent.

–Eliminates the alternative minimum tax.

–Eliminates the personal exemption phase-out (PEP) and the Pease limitation on itemized deductions.

–Limits the value of additional itemized deductions to 28 percent for households with income over $250,000.

Payroll Tax Changes

–Creates a new 6.2 percent employer-side payroll tax on all wages and salaries. This is referred to by the campaign as an “income-based health care premium paid by employers.”

–Creates a 0.2 percent employer-side payroll tax and 0.2 percent employee-side payroll tax, to fund a new family and medical leave trust fund.

–Applies the Social Security payroll tax to earnings over $250,000, a threshold which is not indexed for wage inflation.

Business Income Tax Changes

–Eliminates several business tax provisions involving oil, gas, and coal companies.

–Ends the deferral of income from controlled foreign subsidiaries.*

–Changes several international tax rules to curb corporate inversions and limit use of the foreign tax credit.*

Estate Tax Changes

–Decreases the estate tax exclusion from $5.4 million to $3.5 million.

–Raises the estate tax rate from 40 percent to a set of rates ranging between 45 percent and 65 percent.

–Changes several estate tax rules involving asset valuation, family trusts, gift taxes, and farmland and conservation easements.*

Other Changes

–Creates a financial transactions tax on the value of stocks, bonds, derivatives, and other financial assets traded by U.S. persons. The rate of the tax ranges from 0.005 percent to 0.5 percent, depending on the type of asset.*

–Limits like-kind exchanges of property to $1 million per taxpayer per year and prohibits the use of like-kind exchanges for art and collectibles.*

Now, The Weekly Standard analysis:

Now that Bernie Sanders has routed Hillary Clinton by 22 points in New Hampshire, the American people might be curious to learn more about some of his specific policy proposals, starting with his tax plan. The nonpartisan Tax Foundation has scored Sanders’s plan and has found it would cause the after-tax incomes of those in the middle of the income spectrum—those with incomes between the 40th and 60th percentiles—to drop by between 16.3 and 17 percent. In other words, Sanders’s tax plan would reduce the typical American’s income by a sixth.

This would result partly from Sanders’s raising of taxes on the middle class (and on everyone else), and partly from the ill-effects that his myriad tax hikes would have on the economy. In terms of tax increases for the middle class, Sanders would add a new 6.2 percent employer-side payroll tax that his campaign calls an “income-based health care premium paid by employers,” which would be passed on to employees in the form of lower wages. He would also add a new 2.2 percent “income-based [health-care] premium paid by households,” which the Tax Foundation writes “is equivalent to increasing all tax bracket rates by 2.2 percentage points.” It turns out that government-run “single payer” health care requires a whole lot of payers.

In all, the Tax Foundation finds that Sanders’s tax plan would be a $13.6 trillion tax hike—27 times as large as Hillary Clinton’s proposed $498 billion tax hike.

Sanders’s plan would also shrink the U.S. gross domestic product by 9.5 percent over ten years in relation to what it otherwise would have been, according to the scoring. That means it would decrease the size of the economy by about $2.6 trillion—or about $8,000 for every American, or $32,000 per family of four. If a rising tide lifts all boats, Sanders’s plan seems designed to sink the whole American fleet.

While middle-class Americans’ incomes would fall by a sixth under Sanders’s plan, the incomes of the top one percent would fall even more, dropping by a quarter. That might provide some solace for Sanders supports—if everyone is less prosperous, everyone should at least be more equal.

If you’d like to read the full Tax Foundation study, go here.

by | ARTICLES, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

President Obama’s final budget was submitted today, a $4.1 trillion millstone for American taxpayers. The budget was chock full of tax hikes in order to fund Obama’s pet projects, and “proposed investments in infrastructure, cyber security, education, and job growth.” The FY2017 budget has an $503 billion deficit, which would follow the heels of the projected budget deficit for the current FY2016, $616 billion.

Highlights from the bill include:

— $11 billion for the Departments of Defense and State to fight Islamic State militants and stabilize Syria

— $19 billion for cyber security investments across the U.S. government

— a $10.25 per barrel tax on imported and domestically produced oil to fund transportation infrastructure such as mass transit and high speed rail

— eliminating including the “carried interest” loophole allowing investment fund managers to treat income as capital gains

— impose the “Buffett Rule” to ensure that millionaires pay a tax rate of no less than 30 percent of their income after charitable contributions

— a new fee on the liabilities of the largest banks that would raise $111 billion over 10 years and discourage excessive leverage in the financial system.

— $152 billion for research and development

On the cost savings side, Obama’s budget seeks to reduce deficits by $2.9 trillion over the next decade. “The budget forecasts that deficits would average 2.5 percent of U.S. economic output over 10 years compared to about 4.0 percent in the Congressional Budget Office’s estimate, which is based on existing tax and spending laws.”

From the looks of this budget, President Obama clearly foresees or at least champions a Bernie Sanders presidency. Big tax increases on the wealthy are predictable, but the proposed bank “fee” is a new concept. It’s the last gasp of a failed presidency mired by economic illiteracy.

by | ARTICLES, BLOG, ECONOMY, GOVERNMENT, TAX TIPS, TAXES

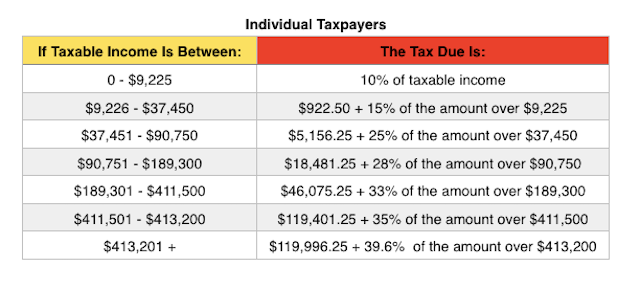

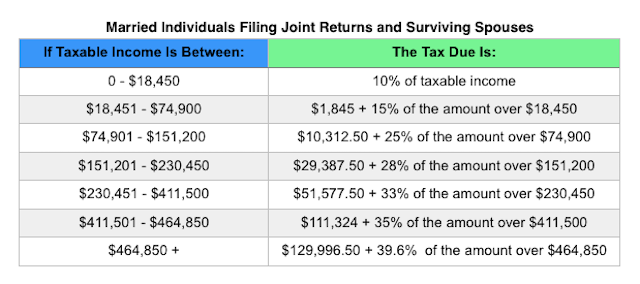

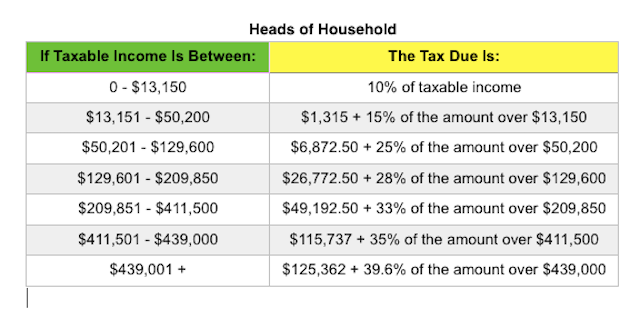

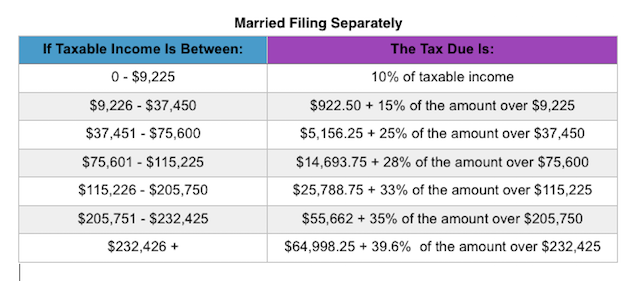

Tax season has begun. Normally, the deadline for filing your federal tax return is April 15. But because the Washington D.C. Emancipation Day holiday falls on April 15 this year, Tax Day is the Monday after, April 18th.

Last spring, Forbes put together a nice, extensive list of all the tax rates and adjustments for 2015. I have posted below some of the most pertinent information. For an all-inclusive list, you should check out the article in its entirety.

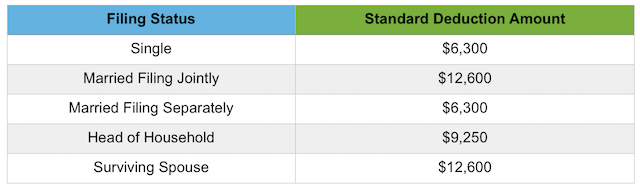

The standard deduction amounts are:

Some tax credits are also adjusted for 2015. Some of the most common tax credits are:

Earned Income Tax Credit (EITC). For 2015, the maximum EITC amount available is $3,359 for taxpayers filing jointly with one child; $5,548 for two children; $6,242 for three or more children (up from $6,143 in 2014) and $503 for no children. Phaseouts are based on filing status and number of children and begin at $8,240 for single taxpayers with no children and $18,110 for single taxpayers with one or more children.

Child & Dependent Care Credit. For 2015, the value used to determine the amount of credit that may be refundable is $3,000 (the credit amount has not changed). Keep in mind that this is the value of the expenses used to determine the credit and not the actual amount of the credit.

Hope Scholarship Credit. The Hope Scholarship Credit for 2015 is an amount equal to 100% of qualified tuition and related expenses not in excess of $2,000 plus 25% of those expenses in excess of $2,000 but not in excess of $4,000. That means that the maximum Hope Scholarship Credit allowable for 2015 is $2,500. Income restrictions do apply and for 2015, those kick in for taxpayers with modified adjusted gross income (MAGI) in excess of $80,000 ($160,000 for a joint return).

Lifetime Learning Credit. As with the Hope Scholarship Credit, income restrictions apply to the Lifetime Learning Credit. For 2015, those restrictions begin with taxpayers with modified adjusted gross income (MAGI) in excess of $55,000 ($110,000 for a joint return).

Changes were also made to certain tax Deductions, deferrals & exclusions for 2015. You’ll find some of the most common here:

Student Loan Interest Deduction. For 2015, the maximum amount that you can take as a deduction for interest paid on student loans remains at $2,500. Phaseouts apply for taxpayers with modified adjusted gross income (MAGI) in excess of $65,000 ($130,000 for joint returns), and is completely phased out for taxpayers with modified adjusted gross income (MAGI) of $80,000 or more ($160,000 or more for joint returns).

Flexible Spending Accounts. The annual dollar limit on employee contributions to employer-sponsored healthcare flexible spending accounts (FSA) edges up to $2,550 for 2015 (up from $2,500).

IRA Contributions. The limit on annual contributions to an Individual Retirement Arrangement (IRA) remains unchanged at $5,500. The additional catch-up contribution limit for individuals aged 50 and over remains at $1,000.

Also note that the floor for medical expenses remains 10% of adjusted gross incocome (AGI) for most taxpayers. Taxpayers over the age of 65 may still use the 7.5% through 2016.

For a more complete list of tables and rates, check out the Forbes article or visit the official IRS website.

by | BLOG, ELECTIONS, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

The State Department, in tandem with the IRS, will soon have the ability to “block Americans with ‘seriously delinquent’ tax debt from receiving new passports and will be allowed to rescind existing passports of people who fall into that category.” This new law will likely begin in January 2016.

The roots of this new law began back in 2012, a report issued by the GAO suggested the possibility of tying tax collection to passport issuance, in an effort to collect revenue. Soon thereafter, Senator Harry Reid introduced a bill in Congress that did just that, with a threshold of $50,000 in delinquency. The bill been attempted several times in Congress over the last few years.

Most recently, the new rule proposal is tucked into a highway-funding bill (HR22) that currently sits in committee and is likely to be voted on sometime in December.

Though there will be exceptions to the rule (emergency and humanitarian travel, for instance), valid criticisms of the rule were raised earlier this year in Forbes. For instance the proposal “isn’t limited to criminal tax cases or even situations where the government fears you are fleeing a tax debt. In fact, if the bill is passed you could have your passport revoked merely because you owe more than $50,000 and the IRS has filed a notice of lien.

A $50,000 tax debt is easy to amass today. In addition, tax liens are pretty standard. The IRS files tax liens routinely when you owe taxes. It’s the IRS way of putting creditors on notice so the IRS eventually gets paid. In that sense, the you-can’t-travel idea seems extreme. Some commentators noted that a far smaller sum of unpaid child support can trigger similar passport action. Others attack the proposal as potentially unconstitutional.”

The Joint Committee on Taxation has estimated that the new law would raise about $400 million over the next decade.

A serious problem, however, looms for millions of U.S. citizens living abroad. Passports, obviously, are essential for travel, residency permits, banking, school, and work visas; yet, the IRS has documented trouble with getting mail properly to ex-pats.

The Wall Street Journal mentioned noted that ” a report issued in September by the Treasury Inspector General for Tax Administration, or Tigta, a watchdog agency, found that the IRS sent 855,000 notices to U.S. citizens abroad in 2014. According to the report, ‘IRS data systems aren’t designed to accommodate the different styles of international addresses, which can cause notices to be undeliverable.’

The Tigta report said that ‘current IRS processes for addressing international mail issues are ineffective or nonexistent.’ In response, the IRS said that Tigta’s recommendations wouldn’t overcome the agency’s ‘budgetary, statutory, and operational constraints.’ ”

The implementation of this new law will be worthwhile to watch in the coming months, especially as it will likely affect those living abroad.