The newest calls to raise the minimum wage in NYC to $11/hour are a frustrating reminder that the city’s own Comptroller, Scott Stringer, has a total lack of understanding about how economics work.

Scott Stringer makes the argument that raising the minimum wage to $11/hour would provide an additional $2 billion in annual income to working families. While that might sound good to taxpayers — to get more money in their pockets — he completely fails to explain the other side of the equation: from where does that $2 billion come?

Stringer seemingly takes that $2 billion figure out of thin air, as there is no documented basis from which he arrived at this number. If Stringer is not utterly incompetent, then he should certainly have available his complete analysis of the financial pluses and minuses that are likely to occur as the result of the minimum wage hike; after all, that is his job.

Here’s the problem. Minimum wage hikes mean that all employers in New York City – both in the government and in the private sector – will pay more for its labor than it currently does pay, in order to produce the exact same product or services. Looked at it another way, in order to keep to the operating budget, NYC will get less goods and services than it now receives. Or, to keep its present level of operations would result in a budget deficit — because of having to spend more overall to maintain the current goods and services.

Therefore, the thought that minimum wage increases — especially a substantial one — will not have a negative effect on the city economy, is ludicrous.

The standard justification goes that the higher minimum wage puts more money into needy families and therefore strengthens the economy. This argument just happens to have a wonderful political effect for Democrats: it makes them seem sensitive to the plight of the needy, while making Republicans look like shills for those greedy Republican businessmen who are only trying to squeeze every last dollar out of their poor employees.

Just one problem —the Democratic position is nonsense, and economists know it, because of simple Economics 101: no businessman would be willing to pay an employee more than the economic value of the employee for him to perform his work.

Let’s assume that the rise in the minimum wage puts the cost of employee in excess of the value of that employee. The employer may then 1) terminate the employee (saving the excess of cost over productivity) or 2) buy equipment which, at that price, becomes cheaper than the employee.

But let’s say the employer keeps the employee, just paying him more for the same work he did before. The employer will then either a) earn a smaller return on his investment, reducing the amount he will be able to invest in the business in the future; b) he will raise his prices, which will maintain his profit margin, but will reduce his sales via you, or c) some combination of a) and b). In either case, growth of the NY economy will be hurt.

Here in New York City, a minimum wage hike would mean that New York City will pay more for its labor than it currently has calculated to pay, in order to produce the exact same product or services. Looked at it another way, to then keep to the operating budget, NYC will get less goods and services for the taxes it receives. This would result in a budget deficit — because of having to spend more overall to maintain the current goods and services.

Therefore, the thought that minimum wage increases — especially a substantial one — will not have a negative effect on the city economy, is ludicrous.

What the city is demanding with the minimum wage increase will have two effects. First, businesses in the city will have to pay their labor more, thereby raising the price of their goods to cover the wage increase. This ultimately will render New York City businesses less competitive than other businesses not located in the city. The result? Our businesses will lose business to those outside of New York City. That is not positive for the economy.

Secondly, New York City is often required to buy from the lowest bidder for many of its goods and services. Therefore, the city would likely have end up buying from outside of the city in order to get those cheaper prices — thereby not supporting the city’s own businesses.

The net effect of a minimum wage hike from $8 to $11 (a 37.5% increase) will take its toll on businesses in New York City and the economy. Stringer has publicly admitted that “the budgetary path we are on is still not sustainable.” Instead of cutting spending, his solution is to make the businesses cough up extra funds via a wage increase so that those wages can subsequently be taxed for more revenue for the city and the city’s budget — even at the expense of NYC businesses. Taxpayers too, will be affected, because their tax dollars will have less purchasing power in the city.

The minimum wage is already set to rise incrementally through 2015 to $9.00 for New York. Pushing through a faster and higher minimum wage increase will handicap New York City businesses in an already sluggish economy, and punish those companies who already endure high taxes and unending bureaucracy under the heavy hand of government.

What is Wall Street, anyway? I would be willing to bet that 90% of the protesters from Occupy Wall Street and of self-styled liberals have absolutely no idea what Wall Street is, what it does, and how important it is.

If not for Wall Street, there wouldn’t be any Main Street, certainly not as we know it today.

In order for any business to be successful, it must run on capital. Capital can be funded by an owner’s personal investment or through funds from outside investors. The ability to grow from the Mom and Pop store to the bigger corporation model is dependent upon the business owner’s ability to get risk capital.

This risk capital is necessary to rent the space, hire the employees, grow the inventory,and buy the equipment to get the business going. There is no guarantee that this money could ever be paid back. But the investors are willing to risk their hard-earned money in the hope that the venture is successful enough to 1) repay the money borrowed and 2) to give back a reasonable profit for the risk taken.

So where does that money typically come, that risk capital? Wall Street. Look around the house at what you have. Your lights? From the utility company. Where did that capital come from to build the utility plants, to lay the distribution networks, to expand them? Risk capital. Wall Street. Where did Macy’s get its start? Or Google, or IBM? Or any of the energy, pharmaceutical, or chemical companies? Or virtually any large corporation you can think of today — where did it get its funds to really get going and continue to grow? Wall Street.

And the people on Wall Street, people sometimes described (invariably by clueless politicians and populists who know nothing about what it takes to run a business or create jobs) as paper-pushers who make unconscionable amounts of money, what do they do?

They must be able to analyze how businesses (Main Street) work, and which ones (out of the many thousands out there all claiming to be worthy) are likely to be successful. They must develop the confidence of potential investors, and convince them to invest in these projects. They must bring the companies and investors together to agree on how much of the company the investors would get for the amount of capital that is being invested. Should the money invested be equity (ownership in the company) or bonds (loans to the company), and if bonds, what interest rate? Most importantly, more than in any other business, pay day never comes to Wall Street unless the capital is successfully raised. And if Main Street is not successful with its new capital, good luck for that Wall Street company in trying to raise money for its next project.

There have been abuses on Wall street, certainly. But there is absolutely no reason to believe that there are any more abuses than in any other business. And those abuses almost always are paid for with serious financial pain to those companies.

But none of these abuses can compare with the financial abuses and mismanagement that we endure daily from our government. Our government has us at the brink of bankruptcy, with a $17 trillion dollar debt (more than 100% of our GDP) which balloons to more than $100 trillion if our entitlement obligations are included.

We have President Obama and the Democratic leaders of the Senate (Harry Reid) and the House (Nancy Pelosi) saying that this is not a current problem (clearly not the truth) and spending money they don’t have to get votes for the next election. A short trip through YouTube (circa 2004-2005) clearly show that Barney Frank (Democratic House…), Chris Dodd (Democratic Senate ….) and Maxine Waters (Democratic House ….), among other Democrats, were principally responsible for the recent economic meltdown. The videos of Congressional Hearings demonstrate unquestionably that Fannie Mae and Freddie Mac were cooking their own books and lending to dangerously unqualified borrowers, but the Democrats prevented any remedial action to be taken.

And taxpayers and Main Street have borne the heavy burden of their negligence during this sluggish, anemic economic recovery.

Wall Street is an invisible backbone of our economy — providing the money and investments that are necessary to continue America’s upward mobility in all facets of our lives. Focusing only on trumped up Wall Street problems or buying into the class warfare hatred of the rich is misguided — especially while giving our government a free pass to use and abuse our taxpayer money each day.

It is really obvious to see that Ben Bernanke was not an independent Fed Chair, but just a lackey for President Obama. Though his responsibility was monetary policy, he was often asked why – despite the most stimulative monetary policy possible – the economy has shown the worst recovery, by far, since the Great Depression more than 80 years ago.

As a student of the Great Depression, Mr. Bernanke was fully aware of the disastrous policies of FDR that impeded the recovery – large tax increases, burdensome regulation, anti-business government programs, and overboard support of union labor- and that President Obama followed suit in every particular.

And yet not a word from Mr. Bernanke that these policies should be questioned. You might be able to say that the President didn’t know any better – you cannot say that about Mr. Bernanke.

I find Mr. Bernanke’s failure to address the exploding Obama regulatory excesses particularly inexcusable. The effect of new regulations from the EPA, NLRB, ObamaCare, Dodd Frank, etc., etc. clearly serves to curtail expansion plans, absorb capital that otherwise would have been used for growth, and increase the costs of starting a new business (clearly scuttling some). At least some meaningful portion of our scrawny recovery can be explained by this regulatory environment.

As Chair of the (supposedly) independent Federal Reserve, Mr. Bernanke owed it to the American people to speak out. This failure should be long-remembered.

The new pre-school plan presented by Mayor de Blasio reveals just how politically disingenuous he really is.

In his effort to push the progressive agenda he put forth during his campaign, de Blasio has vowed to have universal pre-school in New York State to be paid for only by the wealthiest New Yorkers.

Here’s the logical inconsistancy: If universal pre-school is the all-important and necessary step for all children in their educational development (the merits of which is fodder for another article entirely), then the only logical conclusion is that the cost should also be borne by all taxpayers the way K-12 already is — not just a select few. If “everyone” is not willing to pay his or her fair share of this “necessary” project, then maybe that tells us that it should not be done.

This line of thinking clearly echoes the Obama Administration’s sentiment that the rich “pay just a little bit more”, and it is not welcome in New York.

Today marks the fifth anniversary of the Santinelli Rant on the floor of the Chicago Mercantile Exchange, which spawned the infamous Tea Party (Taxed Enough Already?). Even if you heard it then, it’s definitely worthwhile listening to once more:

The first Tea Party protests subsequently followed on February 27th to protest the American Recovery and Reinvestment Act (ARRA) stimulus bill signed by President Barack Obama on February 17th, 2009.

There is raging debate about whether or not the Tea Party still holds the influence it did during the 2010 Congressional elections as well as whether or not ARRA helped our economy recovery.

“Five years later, the U.S. economy is undoubtedly in a stronger position, thanks to the grit and determination of our nation’s workers and businesses. The economy has now grown for 11 straight quarters, and businesses have added 8.5 million jobs since early 2010. While far more work remains to ensure that the economy provides opportunity for every American, there can be no question that President Obama’s actions to date have laid the groundwork for stronger, more sustainable economic growth in the years ahead.”

At the same time, Obama has more than doubled the public debt. CNS News reported that “the marketable debt of the U.S. government has more than doubled–climbing by 106 percent–while President Barack Obama has been in office, increasing from $5,749,916,000,000 at the end of January 2009 to $11,825,322,000,000 at the end of January 2014”

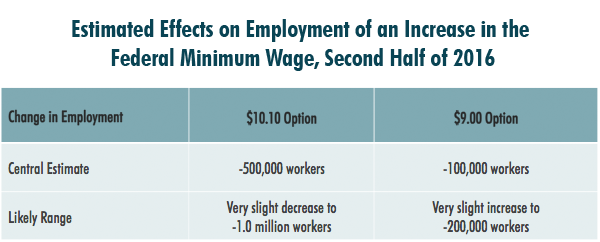

“Increasing the minimum wage would have two principal effects on low-wage workers. Most of them would receive higher pay that would increase their family’s income, and some of those families would see their income rise above the federal poverty threshold. But some jobs for low-wage workers would probably be eliminated, the income of most workers who became jobless would fall substantially, and the share of low-wage workers who were employed would probably fall slightly”

What Options for Increasing the Minimum Wage Did CBO Examine?

For this report, CBO examined the effects on employment and family income of two options for increasing the federal minimum wage:

1) A “$10.10 option”

A “$10.10 option would increase the federal minimum wage from its current rate of $7.25 per hour to $10.10 per hour in three steps—in 2014, 2015, and 2016. After reaching $10.10 in 2016, the minimum wage would be adjusted annually for inflation as measured by the consumer price index.

2) A “$9.00 option”

A “$9.00 option” would raise the federal minimum wage from $7.25 per hour to $9.00 per hour in two steps—in 2015 and 2016. After reaching $9.00 in 2016, the minimum wage would not be subsequently adjusted for inflation.

It was certainly no surprise to most of us the the CBO report showed Obamacare was costing the economy countless jobs. White House and congressional Democrats could have put a rational spin on it – that this was a necessary price to pay in order to get his signature health care proposal implemented, – but they didn’t do that.

Instead, they chose a response which showed them to be the disingenuous hypocrites that they truly are. It also showed that the true intention is simply political — in other words, they wantonly come up with whatever excuse will lose them the least number of votes.

The White House and congressional Democrats have explained the CBO’s job loss outlook to actually be a good thing. The job losses merely reflect the fact that individuals will, going forward, have choices. Such examples include the option to retire before one might have otherwise done so, or perhaps stay at home as a single parent because the government is providing for them (health care) what otherwise only a job could.

But this “logic” is ridiculous. Electing the option to not work when one could do so will certainly prevent many people from getting ahead along the economic chain. And in combination with an extension of food stamp benefits, an extension of unemployment benefits, an extension of other welfare programs, and raising the minimum wage, all are acting in tandem to prevent the upward mobility that the President has said he so sorely wants and unequivocally demands.

He can’t have it both ways. The President cannot be both against economic inequality and simultaneously for policies that maintain prolonged dependence. The preposterous idea that work is now a “lifestyle” choice reveals the shallowness of his commitment to economic success.