by | ARTICLES, BLOG, BUSINESS, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

Marketwatch is reporting dismal numbers related to economic growth in the first three months of 2016; expansion is “the slowest pace in two years as business slashed investment by the steepest amount since the Great Recession.”

GDP growth was significantly reduced as well — recording a .5% annual growth rate. The prior three quarters were 1.4%, 2% and 3.9% in the preceeding year, per quarter.

Marketwatch suggests that some economists contend this sluggishness is an anomaly and will bounce back this spring, estimating a 200,000 job growth for April numbers, which will be released on the first Friday in May. Those with this sentiment predict that “the economy will speed up to a 2.6% annual clip in the spring, typically the fastest growing quarter of the year. The same pattern occurred in both 2015 and 2014.”

On the other hand, I tend to side with economists who are a little bit leery about a robust-growth outlook. “A tepid global economic scene and a tumultuous U.S. presidential election marked by heavy anti-corporate rhetoric appears to have made business executives more cautious.”

Business investment is certainly anemic, and we’ve recently crossed the threshold of more businesses closing than opening. None of this is a sign of a healthy economy, and I doubt very much that the April numbers will be so rosy.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

The Hill has an interesting article about Obamacare, premium costs, and insurance companies. Insurers have been losing money as a result of the Obamacare set-up, and many are facing increased financial security. From the article:

Insurers say they are losing money on their ObamaCare plans at a rapid rate, and some have begun to talk about dropping out of the marketplaces altogether.

“Something has to give,” said Larry Levitt, an expert on the health law at the Kaiser Family Foundation. “Either insurers will drop out or insurers will raise premiums.”

While analysts expect the market to stabilize once premiums rise and more young, healthy people sign up, some observers have not ruled out the possibility of a collapse of the market, known in insurance parlance as a “death spiral.”

In the short term, there is a growing likelihood that insurers will push for substantial premium increases, creating a political problem for Democrats in an election year.

Insurers have been pounding the drum about problems with ObamaCare pricing.

The Blue Cross Blue Shield Association released a widely publicized report last month that said new enrollees under ObamaCare had 22 percent higher medical costs than people who received coverage from employers.

A report from McKinsey & Company found that in the individual market, which includes the ObamaCare marketplaces, insurers lost money in 41 states in 2014, and were only profitable in 9 states.

“We continue to have serious concerns about the sustainability of the public exchanges,” Mark Bertolini, the CEO of Aetna, said in February.

The Aetna CEO noted concerns about the “risk pool,” which refers to the balance of healthy and sick enrollees in a plan. The makeup of the ObamaCare risk pools has been sicker and costlier than insurers hoped.

The clearest remedy for the losses is for insurers to raise premiums, perhaps by large amounts — something Republicans have long warned would happen under the healthcare law, known as the Affordable Care Act (ACA).

“The industry is clearly setting the stage for bigger premium increases in 2017,” said Levitt of the Kaiser Family Foundation.

Insurers will begin filing their proposed premium increases for 2017 soon. State regulators will review those proposals, and then can either accept or reject them.

Michael Taggart, a consultant with S&P Dow Jones Indices, pointed to data from his firm showing per capita costs for insurers are spiking in the ObamaCare marketplaces.

“We made a significant change in the rules with the ACA and we’re still working through the process to see how that market stabilizes,” Taggart said at a panel on Wednesday. “Is [a death spiral] a possibility? Sure it’s a possibility. I wouldn’t attempt to put a probability on it because I think there are a lot of things going on.”

One factor helping to prevent a death spiral is ObamaCare’s tax credits, which cushion the impact of premium increases on consumers.

“What we’re likely to see is more of a market correction than any kind of death spiral,” Levitt said. “There are enough people enrolled at this point that the market is sustainable. The premiums were just too low.”

Dr. Mandy Cohen, the chief operating officer of the Centers for Medicare and Medicaid Services (CMS), said in an interview that there is “absolutely not” a risk of a death spiral or collapse in the ObamaCare marketplaces.

While acknowledging that “companies are needing to adjust” to the new system, she pointed to the 12.7 million people who signed up this year, 5 million of whom were new customers, as a sign of success.

“What brings us the most confidence about the long term stability and health of the marketplace is its growth,” Cohen said.

Another risk, should regulators reject large premium increases, is that insurers could simply decide to cut their losses and drop off the exchanges altogether.

“Given that most carriers have experienced losses in the exchanges, often large losses, it only makes sense that most exchange insurers will request significant rate increases for 2017,” said Michael Adelberg, a former CMS official under President Obama and now a consultant at FaegreBD.

“Market exits are not out of the question if an insurer is looking at consecutive years of losses and regulators are unable to approve rates that get the insurer to break-even.”

The most prominent insurer eyeing the exits is UnitedHealth, which made waves in November by saying it was considering whether to leave ObamaCare in 2017 because of financial losses. The company last week announced that it is dropping its ObamaCare plans in Arkansas and Georgia, and more states could follow.

The Department of Health and Human Services argues that the attention on UnitedHealth is overblown, given that the insurer is actually a fairly small player in the marketplaces.

It’s more important to watch what happens with Blue Cross Blue Shield plans, which are the backbone of the ObamaCare marketplaces.

There have been some rumblings of discontent from Blue Cross plans. The plan in New Mexico already dropped off the marketplace there last year after it lost money and state regulators rejected a proposed 51.6 percent premium increase. Now, Blue Cross Blue Shield of North Carolina says that it might drop out of the marketplace because of its losses.

Blue Cross of North Carolina CEO Brad Wilson said in an interview that the company had lost $400 million due to its ObamaCare business.

“We’re not alone and I think that that also is evidence to suggest that there are systemic and fundamental challenges that we all need to have a civilized conversation about,” Wilson said.

He said a key factor in the decision on whether to stay in the market next year will be whether regulators approve whatever premium increase the company ends up proposing so as to try to make up for its losses.

Asked about the risk of a death spiral, Wilson said he is not worried about that happening “tomorrow,” but has concerns if the situation does not change over time.

“There’s not going to be something magical happen that will cause this to turn around,” Wilson said. He is pressing for changes like further tightening up extra sign up periods that insurers say people use to game the system, and repealing the Health Insurance Tax, which could help lower premiums.

Dr. Cohen of CMS said that her agency is in close touch with insurers and Blue Cross Blue Shield of North Carolina in particular. But she pushed back on talk of Blue Cross of North Carolina dropping out of the marketplace, stating flatly that, “I have no concerns about them leaving the market.”

She referred to problems the company has had with its computer systems that have led to some people being enrolled in the wrong plan, along with other issues that have added to the company’s administrative costs.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

A short but informative article by the Washington Free Beacon describes how the Government Accountability Office (GAO) has calculated that within a few years, the federal government will owe more money that the sum of what is produced by the economy. That, my friends, is an egregious amount of debt.

“Gene Dodaro, the comptroller general for the Government Accountability Office, testified at the Senate Budget Committee to provide the results of its audit on the government’s financial books.

“We’re very heavily leveraged in debt,” Dodaro said. “The historical average post-World War II of how much debt we held as a percent of gross domestic product was 43 percent on average; right now we’re at 74 percent.”

Dodaro says that under current law, debt held by the public will hit a historic high.

“The highest in the United States government’s history of debt held by the public as a percent of gross domestic product was 1946, right after World War II,” he said. “We’re on mark to hit that in the next 15 to 25 years.”

Another economic projection which assumes that cost controls for Medicare don’t hold and that healthcare costs continue to increase, shows debt rising even further.

“These projections go to 200, 300 percent, and even higher of debt held by the public as a percent of gross domestic product,” said Dodaro. “We’re going to owe more than our entire economy is producing and by definition this is not sustainable.”

Additionally, the audit found fault with the number of improper payments that should not have been made or were the incorrect amount. The audit found that in fiscal year 2015 there were $136.7 billion improper payments, which was up by $12 billion from the year prior.

The audit also called into question the reliability of the government’s financial statements. According to the report, if a federal entity purchases a good or service, that cost should match the revenue recorded by the federal entity that sold the good or service. The report found that this was not always the case and found hundreds of billions of dollars in differences between transactions between federal entities.

“The government-wide financial statements that the GAO audits tell us what came into the government’s coffers and what went out, what the government owns and what it owes, and if the operations are financially sustainable,” said Sen. Mike Enzi (R., Wyo.). “But can we trust the information in the statements?”

“GAO’s audit calls into question the reliability of the underlying financial data,” he said. “The sketchiness is such that GAO remains unable to even issue an audit opinion on the government’s books.”

According to the audit, these weaknesses will eventually harm the government’s ability to reliably report their assets, liabilities, and costs, and this will prevent the government from having the information to operate in an efficient and effective manner.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, RETIREMENT, TAXES

The Financial Times reviewed data recently that suggested that the US public pension system is in dire straits; the funding shortage is likely 3 times as large as what is being reported. The estimated deficit is $3.4 trillion.

The solutions for the funding shortfalls are grim: either raise taxes or cut spending; unfortunately the “cut spending” approach always goes to the essential services first, so that taxpayers feel the heat and will consider a tax hike instead.

US Congressman Devin Nunes recently noted that, “It has been clear for years that many cities and states are critically underfunding their pension programmes and hiding the fiscal holes with accounting tricks.” Nunes has “put forward a bill to the House of Representatives last month to overhaul how public pension plans report their figures.” He added: “When these pension funds go insolvent, they will create problems so disastrous that the fund officials assume the federal government will have to bail them out.”

Insolvency has already been observed in San Bernardino, California and Detroit, Michigan, largely due to mismanagement of pension funding and budget shortfalls. The Financial Times noted that “Chicago, Dallas, Houston and El Paso have the largest pension holes compared with their own revenues”, as well as the states of Illinois, Arizona, Ohio, and Nevada.

Research done by Stanford paints a difficult future: “Currently, states and local governments contribute 7.3 per cent of revenues to public pension plans, but this would need to increase to an average of 17.5 per cent of revenues to stop any further rises in the funding gap.”

And more: “Several cities and states, including California, Illinois, New Jersey, Chicago and Austin, would need to put at least 20 per cent of their revenues into their pension plans to prevent a rise in their deficits, while Nevada would have to contribute almost 40 per cent.”

Much of the problem lies in the fact that retirement costs and liabilities have consistently been calculated on a 7%-8% return , which is not particularly realistic, as has been demonstrated in recent years during the economic downturn.

There is no way this silent funding crisis will get any better — and until localities recognize and admit their crisis and make ardent changes to their pension systems, it will only continue to worsen egregiously.

by | ARTICLES, BUSINESS, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAX TIPS, TAXES

The Fix the Debt Campaign Steering Committee is a bipartisan group of prominent leaders and experts, including luminaries such as Erskine Bowles and Alan Simpson, the co-chairs of the White House Fiscal Commission. The Fix the Debt group put together some decent graphics regarding federal spending.

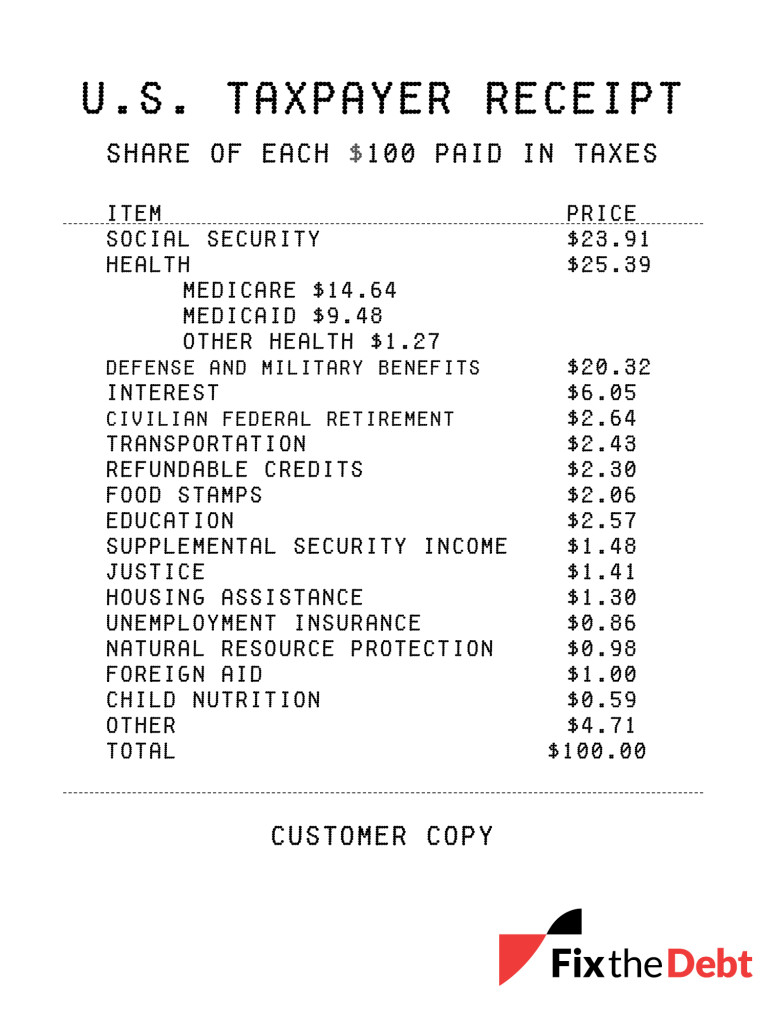

This is a “taxpayer receipt” highlighting where the money goes and highlight where it comes from in the first place.

How are our federal tax dollars spent? As the taxpayer receipt illustrates, more than $75 of every $100 paid in federal taxes goes to Social Security, federal health care, defense, and interest on the debt. And the amounts for Social Security, health care, and interest are forecast to grow considerably in the years to come.

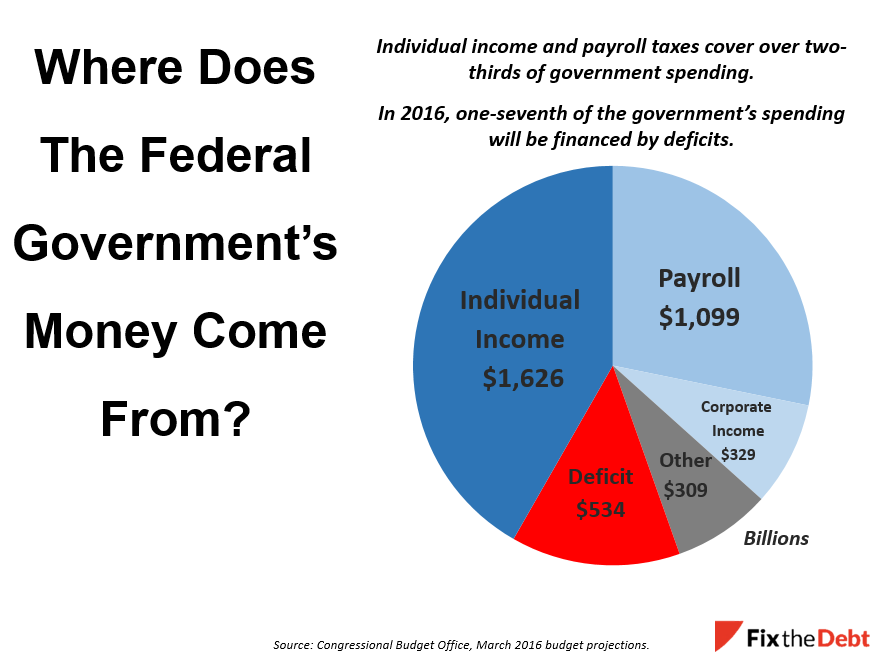

Where does the money come from? Much of the revenue for the federal government comes from the individual income tax that many of us are rushing to complete. Another major source is the payroll tax, which is the “FICA” tax that is withheld from your paycheck. It is used to fund Social Security benefits and parts of Medicare.

But a significant part of the government is deficit financed because spending exceeds revenue. That share is expected to grow substantially in the years ahead.

Check out their blog for more information.

by | ARTICLES, BUSINESS, ECONOMY, FREEDOM, GOVERNMENT, HYPOCRISY, POLITICS, TAXES

Yesterday, The Treasury Department made more changes to rules with regard to inversions. The driving force behind the constant meddling into this legal practice is the retention of tax revenue.

“Under the new rules, there will be a three-year limit on foreign companies bulking up on U.S. assets to avoid ownership requirements for a later inversions deal, Treasury said in a statement.”

In an inversion, a U.S. company typically buys a smaller foreign rival and reincorporates to the rival’s home country, which moves the company’s tax domicile, though core management usually stays in the United States.

The Treasury, which had last introduced new rules in November to curb inversions, also is proposing tackling the practice of post-inversion earnings stripping with new limits on related-party debt for U.S. subsidiaries.”

This continued attack on inversions is ridiculous and companies are being targeted unfairly because they represent a possible loss of revenue for the government. Inversions are legal, and sometimes necessary. They are a way for U.S. companies to change their HQ from the U.S. to a foreign country, for the sole purpose of allowing themselves the express privilege of being on par with foreign companies and eliminate the severe disadvantage that the U.S. puts on its own businesses via excessive taxes!

It is outrageous that the government applies such discrimination. It is outrageous that American companies have to chose to move their headquarters elsewhere simply to survive and compete globally, because they are taxed on their profits in two jurisdictions — both domestic and foreign.