by | ARTICLES, BLOG, ECONOMY, OBAMA, POLITICS, TAXES

At least you can say Bernie Sanders is ideologically consistent. The self-proclaimed socialist unabashedly declared on Saturday that “we need a tax system which asks the billionaire class to pay its fair share of taxes and which reduces the obscene degree of wealth inequality in America.” It was particularly fitting that the speech was at an AFL-CIO convention.

Over on his Senate page, Sander’s posted his proposal — “a progressive estate tax on the wealthiest Americans”:

“For those who would pay more, the tax rate on estates valued from $3.5 million to $10 million would be 40 percent. There would be a 50 percent tax on estates worth $10 million to $50 million and a 55 percent levy on estates worth more than $50 million. A 10 percent surtax would be applied on estates worth more than $1 billion, a category that today includes fewer than 500 American families. The bill also would close estate tax loopholes that have allowed the wealthy to avoid an estimated $100 billion since 2000.

His rationale? Sanders said that this is “the fairest way to reduce wealth inequality, lower the $17 trillion national debt and pay for investments in infrastructure, education and other neglected national priorities.”

Notice he said fairest — not most efficacious — way to reduce wealth inequality. Because the actual amount raised on such a tax will be negligible for any real deficit reduction, hopefully such a foolish proposal will never be implemented.

Unfortunately, with any sort of supertax, the truest and most invisible effects will be felt in the economy. The confiscatory nature of a high estate tax is among the worst offenders. “The economic incidence of the death tax is far broader, because it causes many wealthy individuals to save less, choosing instead to retire early or, as Milton Friedman put it, “dissipate their wealth on high living.” This reduction in savings means a concomitant reduction in investment, lessening the flow of capital to businesses and organizations where countless ordinary Americans are employed.”

And yet, Sanders sees nothing “obscene” about the another kind of wealth inequality: the salary and benefits of Congress, which, at $286K, is about 95% greater than what average Americans earn. Or still yet, another kind of wealth inequality: the $17 trillion government debt and spending problem that he is purporting to fix by his punitive tax proposal.

by | ARTICLES, ELECTIONS, GOVERNMENT, OBAMA, POLITICS, TAXES

The idea of “disparate impact” is a cancer that has taken root in the business world. If we do not focus on substantially curbing or ending it, it will continue to grow, extorting huge sums from innocent companies, creating an enormous economic burden on society, and allowing the tort bar to run amok.

There are many areas in business where charges of “discrimination”, often regarding race, could and are being made every day. Employment and mortgage origination are two of the most prevalent. The law requires – as it should -that for a company to be guilty of such discrimination, there must be an intent to discriminate.

But government agencies have found a way to overrule that requirement by developing the idea of “disparate impact”. Disparate impact is the concept which allows if a protected class of citizens has a statistically lesser representation with respect to a business (hiring, mortgages origination, etc) it may be implied that the business has intentionally discriminated — because there is an adverse impact as a result. This is clearly irrational, since there may be many economic, societal, and local reasons for the particular statistical representation. Unfortunately, disparate impact puts the burden to show lack of discrimination on the employer, meaning he is guilty until proven innocent. In fact, in order for an employer to defend himself against such a charge, he would have to show that the “offending rule or practice” was a “business necessity”.

Though I find this concept outrageous, the federal and state governments and their agencies seem to love it lately. I therefore believe that they should be equally adamant in applying the concept of disparate impact in the public sector.

The IRS scandal has shown the clear practice of targeting conservative groups applying for 501c4 status (despite the subsequent cover up). By applying disparate impact theory to this situation, the charge of intentional discrimination would most certainly apply because there is no “business necessity” in the policy the IRS employed.

The Obama administration, having complete control and responsibility for the Department of the Treasury and its Internal Revenue Service is therefore guilty of such intentional discrimination. In particular, President Obama’s specific response, that there has been no evidence that anyone directed anyone to intentionally target conservatives, does not insulate him from being actually guilty.

The current administration has been keen on applying disparate impact theory to a number of private companies, and appears intent on ramping up the practice. For example, Obama’s labor secretary pick, Thomas Perez, has been particularly lucrative in this regard. Last summer, National Review Online (NRO) covered some of Perez’s cases in recent years, noting that Perez “has applied that theory vigorously to force large settlements from financial companies even in cases where there was no evidence of actual racial discrimination”. In other words, employers can be sought after for violating the law whether or not they intended to do wrong.

The White House in general, and Perez in particular, like disparate impact theory because it, as NRO notes, it “sets a very low bar for proving discrimination. Under it, prosecutors need not prove intent, merely that minorities have suffered a disparate impact from some action”. And this is a person Obama added to his Presidential Cabinet.

If disparate impact can be applied to the private sector, it should also — in the spirit of fairness and equality, of course — be applied to the IRS. Particular groups were adversely singled out and subject to excessive, burdensome, and overreaching scrutiny; of this we are certain. The targeting of conservatives was a concerted effort to slow down or dissuade the creation of their tax-exempt groups. Even if we no longer have tangible evidence of a White House link because of lost, missing, or destroyed emails and Blackberrys, it doesn’t really matter anyway under disparate impact theory. Intent needs not to be proved in court; merely the act of discrimination is enough.

Based on the White House’s unmitigated belief of their ability to use disparate impact against companies for questionable practices, the rule should be applied to the IRS for its questionable practices as well. Since the IRS falls directly under the purview of the Executive Branch, why is the President of the United States therefore not directly responsible and culpable for the IRS abuse?

by | ARTICLES, GOVERNMENT, OBAMA, TAXES

Thomas Perez’s recent appearance on “On the Money”, proved his economic naivete once again. It begs the question as to how he can be the head of the Department of Labor?

When asked about inversions, he used an anecdote to set the tone of the discussion. It was about a Fortune 500 Exec who (anonymously) proclaimed “I’d rather be rich than right!” implying that a) these people were willing to do the “wrong thing” to make money and b) that inversions are wrong in general.

By implying inversions are wrong, Perez completely and conveniently ignores the fact that our tax laws currently make taxes lower when a foreign corporation owns a US business than when a US company owns that same business. How stupid is that! That not only provides incentive for US companies to do inversions, but it incentivizes US companies to sell out to foreign owners. Stated differently, it is more profitable for a foreign company to own a US company, than it is for a US entity to own that same company. The law then actively promotes the movement of multinational headquarters out of the US, taking untold numbers of jobs with them.

Only someone who is both economically ignorant and politically partisan could support this status quo, and Thomas Perez fits the bill. Perez as the head of the Department of Labor is in charge of improving the situation for workers – but by his actions, he makes it much worse. He should be making it a priority to advocate for change in our tax policy to make it more friendly for our companies in the United States, not for their foreign competitors.

by | ARTICLES, ECONOMY, FREEDOM, GOVERNMENT, HYPOCRISY, OBAMA, POLITICS, TAXES

Just like the recent rise of business inversions — moving business HQ abroad — the United States has seen an uptick (up 221%) in Americans renouncing their citizenship. The elephant in the room in both these cases is taxes: both high taxes and burdensome tax compliance in foreign jurisdictions.

Instead of facing the problems directly, the Obama Administration has resorted to punitive measures. The shame and blame tactic of calling out businesses who wish to relocate as “unpatriotic” was undignified. Perhaps realizing that using the same strategy with individuals would be even less well received, they went the more quiet, direct route: yesterday, the State Department announced their interim final rule that raises the fee for renouncing citizenship from $450 to $2,350.

Their justification for raising the fee is the time and labor involved in the process; that is, the bureaucratic red tape that they created, and then decide to charge exhorbitant fees for:

“The CoSM demonstrated that documenting a U.S. citizen’s renunciation of citizenship is extremely costly, requiring American consular officers overseas to spend substantial amounts of time to accept, process, and adjudicate cases. For example, consular officers must confirm that the potential renunciant fully understands the consequences of renunciation, including losing the right to reside in the United States without documentation as an alien. Other steps include verifying that the renunciant is a U.S. citizen, conducting a minimum of two intensive interviews with the potential renunciant, and reviewing at least three consular systems before administering the oath of renunciation. The final approval of the loss of nationality must be done by law within the Directorate of Overseas Citizens Services in Washington, DC, after which the case is returned to the consular officer overseas for final delivery of the Certificate of Loss of Nationality to the renunciant. These steps further add to the time and labor that must be involved in the process. Accordingly, the Department is increasing the fee for processing such requests from $450 to $2,350. As noted in the interim final rule dated June 28, 2010 (77 FR 36522), the fee of $450 was set substantially below the cost to the U.S. government of providing this service (less than one quarter of the cost). Since that time, demand for the service has increased dramatically, consuming far more consular officer time and resources, as reflected in the 2012 Overseas Time Survey and increased workload data. Because the Department believes there is no public benefit or other reason for setting this fee below cost, the Department is increasing this fee to reflect the full cost of providing the service. Therefore the increased fee reflects both the increased cost of the provision of service as well as the determination to now charge the full cost.

Interestingly enough, if you compare the cost of renunciation in the United States to the cost of renunciation in other countries, the new fee puts the United States way above others. You can check out this handy chart here. The next two highest are Jamaica ($1,010 in US dollars), and Sierre Leone ($663 in US dollars).

So those who wish to renounce their citizenship get to buy their freedom by paying a 422% fee increase for the express privilege of dealing with United States bureaucracy one final time.

This is considered an administrative fee, issued by the State Department, but it is essentially an unofficial “exit tax” for regular citizens. But there is a real one too. As Forbes notes, “To leave America, you generally must prove 5 years of U.S. tax compliance. If you have a net worth greater than $2 million or average annual net income tax for the 5 previous years of $157,000 or more for 2014 (that’s tax, not income), you pay an exit tax”.

So for those who have done well in the United States, besides the higher administrative fee/exit tax, you get to pay that real “exit tax” knows as the 877A.

Alas, this isn’t the first time those wishing to leave have been targeted. A bigger, punitive measure was attempted in 2012 by Senators Chuck Schumer and Bob Casey. When the co-founder of Facebook, Eduardo Saverin, renounced his U.S. citizenship as a means to save millions in taxes before Facebook went public, the Senators reacted by proposing the “Ex-PATRIOT Act” of 2012 that essentially doubled the exit tax for high worth individuals. “People who could not prove another reason for renouncing citizenship would face a 30% tax on future capital gains on U.S. investments – twice the current 15% rate – and be barred from receiving a visa to enter the country.” Thankfully the bill died in committee the first year, and did not advance out of the Senate in 2013.

Though this new fee hike is different than the standard exit tax, and on a much smaller scale (dollars-wise), it speaks the same language: punish. All this fee hike does is prove that that current administration would rather squeeze U.S. citizens for more revenue, thus likely reiterating to those renouncing their citizenship that being a U.S. citizen lacks much of the value that it once did. And that is a very sad thing.

by | ARTICLES, BLOG, FREEDOM, HYPOCRISY, POLITICS

This would be really funny if it wasn’t so sad.

Brad Woodhouse is President of American Bridge 21st Century, a SuperPAC that “monitors what Republican politicians say and fights back when their rhetoric doesn’t match their records.” This is a PAC well known to be funded by billionaire George Soros.

So when Mr. Woodhouse pushed out a news story entitled, “GOP Senate Candidates Bow at Koch Throne”, someone else noticed the irony in attacking the conservative billionaire Koch Brothers, while simultaneously receiving PAC funding from liberal billionaire George Soros.

Andrew Kaczynski, who writes over at the popular BuzzFeed took to twitter to call out Mr. Woodhouse: “It’s almost pathetic how weak the Democrats ‘run against the Koch brothers’ strategy is.”, he wrote.

One might say this falls squarely under the “fights back when their rhetoric doesn’t match their records” mantra proudly proclaimed on the American Bridge website — except that Mr. Woodhouse clearly did not approve of this particular instance of holding people “accountable for their words and actions”. This only applies to Republicans, according to the PAC website.

Mr. Woodhouse huffily replied to Kaczynski: “it’s a shame you have no idea what you are talking about”, to which Mr. Kaczynski bluntly asked, “Since you’re outraged by billionaires influencing politics @woodhouseb will American Bridge be refunding largest-donor George Soros?”

Pointing out that American Bridge takes money from certain billionaires (approved by the Left) while attacking other billionaires (not approved by the Left) did not sit well with Mr. Woodhouse, as he retorted, “That’s a stupid question”, to which Kaczynski confirmed, “So that’s a no?”.

Mr. Woodhouse then began to rationalize the hypocrisy by applying logic Animal Farm: some billionaires are more equal than others.

“Since you don’t understand the difference I don’t think there is any reason to continue this discussion,” wrote Mr. Woodhouse, to which Kaczynski replied, “I guess @woodhouseb your billionaires are better than their billionaires,”.

Mr. Woodhouse clarified that observation by writing, “well, they’re not looking to screw the middle class to enrich themselves – so yeah – maybe you do get it.”

Kaczynski confirmed the duplicity by pointing out, “So you dislike big money @woodhouseb only when it isn’t your ideology. I understand now.”

Mr. Woodhouse’s reply (and final tweet) continued using the leftist playbook by a) casting the Koch Brothers as anti-middle class and b) his opponent as stupid, by responding, “I dislike people who want to stack the deck against the middle class and am irritated by people who don’t get the difference.” You can view the twitter exchange here:

So, American Bridge is okay with taking good billionaire money while attacking bad billionaire money. Because American Bridge “understands” and “feels” and “believes”.

Its website describes how, “We understand the frustration you feel with elected officials who campaign on one set of principles but govern by another, because we feel it too. We believe you deserve better than that. We think our elected officials should have one set of principles, not one for each set of special interests they represent.”

Can we substitute “PAC” for “elected officials” above?

Nope — apparently this sentiment only applies to Republicans, not liberals or PACs. If you check out American Bridge’s opening description, it states that American Bridge “is a progressive research and communications organization committed to holding Republicans accountable for their words and actions and helping you ascertain when Republican candidates are pretending to be something they’re not.”

Therefore, according American Bridge, only Republicans should be accountable for their words and actions, and only Republicans can pretend to be something they are not. Certainly not Mr. Woodhouse, who became irritated when Mr. Kacyznski “helped him ascertain” that American Bridge was “pretending to be something they’re not” by taking (liberal) billionaire money in politics while attacking (conservative) billionaire money in politics.

That rule does not apply to Woodhouse at all. Not one bit. Because Mr. Woodhouse is not a Republican. So Mr. Woodhouse “gets the difference.” (He “understands” and “feels” and “believes”.)

All billionaires are billionaires. But some billionaires are more equal than others. A classical abuse of logic by the Left.

by | ARTICLES, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

According to the Treasury Inspector General for Tax Admininstration (TIGTA), the 2.3% medical device excise tax enacted to help pay for Obamacare is not meeting targets.

The tax went into affect January 1, 2013. The TIGTA report analyzed the returns for the first two quarters (6 months) of 2013, and found that the “excise tax revenue being reported are lower than estimated” for a total of $913.4 million. The IRS expected to have received “excise tax revenue of $1.2 billion for this same period.”

The report also states that the “Joint Committee on Taxation estimated revenues from the medical device excise tax of $20 billion for Fiscal Years 2013 through 2019.”. And yet, in the first six months alone, the estimate amounts are off by 25%. That does not bode well.

Many of the problems originate in the IRS. In fact, the report is aptly named “An Improved Strategy Is Needed to Ensure Accurate Reporting and Payment of the Medical Device Excise Tax”. Some of the key findings:

“The IRS is attempting to develop a compliance strategy to ensure that businesses are compliant with medical device excise tax filing and payment requirements and has taken several measures to advise medical device manufacturers of the new excise tax. However, the IRS cannot identify the population of medical device manufacturers registered with the Food and Drug Administration that are required to file a Form 720 and pay the excise tax.”

“In addition, processing controls do not ensure the accuracy of medical device excise tax figures reported on paper-filed Forms 720. Our analysis of 5,107 Forms 720 processed for the quarters ending March 31 and June 30, 2013, identified discrepancies in the amount of the medical device excise tax and/or taxable sales amount captured from 276 paper‑filed tax returns. TIGTA identified medical device excise tax discrepancies totaling almost $117.8 million when comparing the excise tax amount captured by the IRS from the Form 720 to the excise tax amount TIGTA calculated.”

And the most interesting:

“Finally, the IRS erroneously assessed 219 failure to deposit penalties totaling $706,753 against businesses filing a Form 720 for the quarters ending March 31 and June 30, 2013, which was designated a penalty relief period. The IRS had reversed 133 of the 219 penalty assessments. When TIGTA alerted the IRS of the remaining 86 penalties, IRS management reversed the penalties and issued apology letters to the affected taxpayers.”

The IRS, it seems, was unprepared to handle the collection of excise tax, and furthermore, did not seems to understand basic reporting and penalty relief periods of which it was put in charge.

Think about this: we are now in August of 2014. That means that the second half of 2013 and the first half of 2014 went by before the TIGTA report was released with its findings. If the first 6 months of revenue were found to be about 25% under estimate, it is likely the trend continued for the next full year.

The IRS did agree to the findings of the TIGTA report. However, the summary does not leave one feeling confident that there will be swift resolution now that the problems have been discovered and dissected. Note the ambiguity and qualifiers:

The IRS agreed with our recommendations and plans to consider alternative strategies for identifying noncompliant manufacturers, identify programming changes needed to improve the math verification for paper-filed Forms 720, and implement procedures for corresponding with taxpayers if the changes can be accomplished within budgetary constraints.

Never mind the fact that the Affordable Care Act passed in March 2010 with the excise tax being a key, but controversial, revenue-raiser. The IRS had nearly three years to come up with a) a system to identify companies who owed the tax and b) a system to process the associated forms. And it couldn’t do it.

With the tax being so controversial from the get-go, there have been measures in Congress calling for its repeal because of its impact on the cost of devices and well as jobs in the medical device field.

“The medical device industry has been lobbying hard to get the tax repealed, and there has been movement in Congress. Both the House and the Senate have passed separate pieces of legislation calling for the tax to be repealed, though the Senate vote was on a nonbinding resolution.”

The problem at this point with excise tax repeal is the question of how to make up for even more lost revenue to pay for Obamacare. Taxpayers should be indeed be nervous that the tax collection is showing to be only 75% and we actually have no idea if it improved or worsened at all over the following year because data is not available for it.

The only thing we do know is that we are certain to see a premium rate increases this coming year because the projections have been so off-estimate.

by | ARTICLES, BLOG, ECONOMY, FREEDOM, GOVERNMENT, HYPOCRISY, OBAMA, POLITICS, TAXES

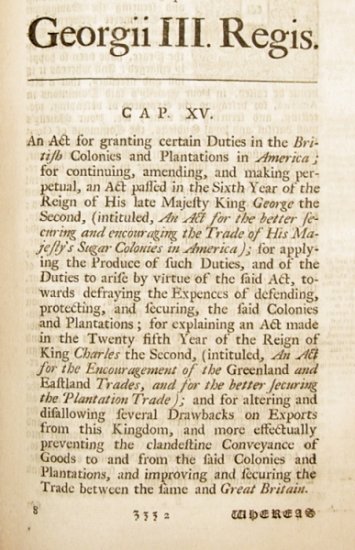

On April 5, 1764, Parliament passed something called “The Sugar Act”, which, interestingly, had another name: “The American Revenue Act”. It was a modification of the 1733 Molasses Act, and it also affected other goods, such as wine and coffee.

The Preamble to this Act states: “it is expedient that new provisions and regulations should be established for improving the revenue of this Kingdom … and … it is just and necessary that a revenue should be raised … for defraying the expenses of defending, protecting, and securing the same.”

The Sugar Act/American Revenue Act, therefore, was a revenue raising measure (and not just a regulation measure), whose revenue was intended to help defray the costs of defending the colonies during the 7 Years War which ended in 1763. Instead, it wreaked havoc in the colonies:

“The situation disrupted the colonial economy by reducing the markets to which the colonies could sell, and the amount of currency available to them for the purchase of British manufactured goods. This act, and the Currency Act, set the stage for the revolt at the imposition of the Stamp Act.”

Fast forward to 2014. A new measure was introduced by Rep. Rosa deLauro called the SWEET Act, also known as the “Sugar-Sweetened Beverages Tax” — a proposed tax of “one cent per teaspoon – 4.2 grams – of sugar, high fructose corn syrup or caloric sweetener”.

The Act sounds eerily like a revenue-raiser, much like its ancestor, the Sugar Act. From the text of the SWEET Act:

“This Act is intended to discourage excessive consumption of sugar-sweetened beverages by increasing the price of these products and by creating a dedicated revenue source for programs and research designed to reduce the human and economic costs of diabetes, obesity, dental caries, and other diet-related health conditions in priority populations”

Let’s compare:

Sugar Act: “improving the revenue of this Kingdom”… “just and necessary that a revenue should be raised”… “for defraying the expenses of defending, protecting, and securing the same.”

SWEET Act: “dedicated revenue source for programs and research”… “to reduce the human and economic costs of diabetes, obesity, dental caries, and other diet-related health conditions”.

Same over-reaching thinking, different government.

As a response to the Sugar Act in May 1764, Samuel Adams drafted a report on the Sugar Act for the Massachusetts assembly, in which he denounced the act as an infringement of the rights of the colonists as British subjects:

For if our Trade may be taxed why not our Lands? Why not the Produce of our Lands & every thing we possess or make use of?

”

Will there also be a similar rebuke over the Sweet Act of 2014? The Sugar Act was subsequently repealed in 1766 because it was such a disastrous piece of legislation. Let’s hope history doesn’t repeat itself and the SWEET Act never comes to fruition.

by | ARTICLES, BUSINESS, GOVERNMENT, OBAMA, POLITICS, RETIREMENT, TAXES

A study was released today that showed more than a third of Americans, (36%)a have saved nothing for retirement. That got me thinking about the idea of retirement and the state of retiring in this country.

Everyone thinks they can retire at age 65. It’s an American ideal born in the last century with the rise of unions, the defined benefit plan, and generous pension systems. In reality, especially due to advances in health, medicine, and nutrition, many people have great capability to continue to work and contribute to society and themselves until 80. And they should — because they need to.

There is a crisis of affordability looming. Besides the enormously wealthy, for the most part no average person can afford to retire at 65. It is simply not possible, living a normal lifestyle, for anyone to put enough toward retirement that will enable him to live another 20-30 years. A life span of 85-95 is swiftly becoming the new norm. The only workers today who are the exception to this reality, and have any hope of a lengthy retirement with comfort, are public service employees.

Taxpayers have been long bamboozled into making generous commitments to the retirement systems of public service workers. All over the country, in all levels of federal and state governments, these defined benefit plan pension funds have proven to be vastly untenable. Yet to sustain the plans in their current arrangements and cover the obligations that have already been promised, the rest of society will be duty-bound/compelled to contribute to the retirement of those public service workers via higher taxes. This is turn makes the rest of the populace poorer — because their hard-earned money is being levied to the promised public pensioner, and not for able to be saved for themselves.

The grand scheme is becoming unhinged. One must realize that the more people continue to buy into the idea that they are supposed to “retire at 65”, the more they are suckered into continuing make their retirement years poorer and subsequently make the retirement years of public service employees richer. People see a public service worker being able to retire at that age and they think “I should be able to also do so”. This idea needs to change.

There are two reasons why most people think that such pension programs are still sustainable and normal: their troubles are largely masked because they encompass the larger budget process of federal/state/local governments (and how many people pay attention?) and the costs to keep the programs afloat are borne by all the rest of society — the taxpayers. This arrangement enables a small group of people to be paid a sizeable and continuous pension for until death. It is not out of the ordinary anymore for a person to receive $65K- $100K for the rest of their life. But the actuarial cost to provide that promised benefit is astronomical.

With the lifespan of Americans growing longer, retiring at 65 is no longer viable; the systems are badly strained. And it is certainly not rational for the longevity of Social Security and Medicare either. Yet the steadfast refusal of most of government to overhaul retirement systems or make age and formula adjustments to entitlement programs — in order to maintain this retirement facade — only compounds the problem. (See the latest regarding the annual Social Security report here)

Another one of the biggest detriments of being able to retire at 65 is investment return. Interest rates have been historically low for the last five years and there is a strong likelihood of them staying low for another few. As a result, peoples’ retirement portfolios have lagged in their anticipated growth and goals. The low rates mean less money overall for retirement time, a problem which can be offset by continuing to work and contribute to a retirement fund past the basic age.

Likewise, inflation is not just the issue that everyone thinks it is. The cost of “modern living”, the “keeping up with the Jones”, is a form of lifestyle inflation that adds to the problem. For example, newer models of everything due to technology constantly changing — upgrading TVs, cell phones, etc. are raising the bar for how much pensioners want to comfortably live on and live with.

In sum, with living longer, low rates of return, and the “cost of Jones’s increase”, people must begin to realize that the timespan between 65 – 80 can be, and should be, a healthy and productive time of life. Working, staying active, and continuing to save will be beneficial in the long run. The mindset of older citizens needs to change and they need to understand that they can should aim to be productive until they are 80. At 65 they can certainly slow down, but the concept of retiring and not working anymore at that age is unrealistic and unaffordable.

by | ARTICLES, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

Earlier this week, the business world was chattering about the news that Kinder Morgan, pioneer of the Master Limited Partnership (MLP) business model, was surrendering the MLP structure in favor of a more traditional corporation. This happened last Sunday.

While many questioned what this meant for the MLP model in general, the more pressing questions began to emerge when, the following day, the Treasury Department came out with a statement regarding MLPs: “We at the Treasury are looking into the effects of these transactions on future tax revenues. Instances where the tax base may be eroded serve as a reminder of why we need Congress to enact business tax reform that broadens the tax base and lowers tax rates.”

Much like that false crusade on inversions, here we have another instance of anti-business sentiment coming out of the Executive Branch. Obama’s abuse of the law is clearly now seeping down to his cabinet underlings who also think now they have the authority to rewrite the law as well — especially under the cloak of getting more tax revenue.

Starting this past April, the government issued a temporary pause in the formation of new MLPs. The way the process works is that the IRS would issue what’s known as “private letter rulings” that examine qualifying income, and then therefore allow an MLP to be formed. However, the Treasury Department decided to examine the standards being used, meaning that the creation of new MLPs have been on hold for a few months.

The internal committee has been tasked with evaluating the “aggressive” rulings regarding qualifying income of MLPs issued in recent years. The internal committee may determine that such rulings are too expansive and recommend stricter interpretations of what types of natural resources income constitute qualifying income.

Most folks in the business world fully expected the formation of MLPs to resume after rules were reviewed. Barrons noted that, “They went through a similar review process for REITs in 2013 and concluded that the approvals were in line with the law. The same results were expected for MLPs and that private letter rulings would resume. But Treasury seems to say they are looking at issues larger than the IRS which would seem like another attempt to jawbone companies in the future from seeking MLP approvals.”

This sudden interest in MLPs sounds eerily similar to the recent interest the government has taken in business “inversions”; the government claims (erroneously) that inversions also deprive the government of supposed-entitled tax revenue, the same flimsy justification for looking more closely at, and ceasing the formation of, MLPs.

The worst part about this new anti-business targeting is that it is completely unfounded. The Treasury Department makes it sound like MLPs somehow are avoiding paying tax revenue by the way the company is structured and calls on the need for “Congress to enact business tax reform”. Except that MLPs ARE a perfect example of a type of reformed business tax structure that Congress should be welcoming.

With MLPs, the business is only taxed once, (the way most business structures around the world already operate.) In the United States, however, corporations face an abominable problem in our tax code known as “double taxation”. Basically if a corporation pays its corporate taxes and then reinvests its profits, there is no extra tax. But if its profit earnings are given to the owner(shareholders), they are taxed again on that amount — hence the double taxation.

Contrast that with MLPs, which “does not incur income taxes. Its income is allocated among all partners in proportion to their ownership interest.” Hence, the taxation only occurs once. This singular taxation of businesses is what real broad-based tax reform should aim for.

The real inequality in the tax code is not the MLP structure, which only taxes businesses one time; it is the double taxation that major corporations face. If Obama is truly for tax reform — like he says he is when he talks about inversions — the MLP structure for businesses is one way to achieve that reform. (Another would be to lower the corporate tax rate.)

Going after MLPs now and reducing the number of them in existence is the opposite of tax reform. Allowing the Treasury Department to play with business rules willy-nilly is egregious. This MLP attack is just another example of how anti-business the Obama Administration really is.

by | ARTICLES, BUSINESS, POLITICS

At the end of June, I penned a piece about Chuck Todd with the opening salvo, “You can’t have anyone that stupid be in charge at NBC.” Now I hear that Chuck Todd is planning on taking over David Gregory’s spot on Meet the Press. That is an utter trainwreck.

Chuck Todd is often uninformed on the topics he is tasked with discussing. Otherwise, he must be disingenously preying on low-information viewers to not know information in the first place.

David Gregory was not that great in his role of Meet the Press moderator. But to hire NBC’s political director, chief White House correspondent, and MSNBC host as the replacement, is ridiculous. Meet the Press will continue to decline as a formidable weekend talk show force.