by | ARTICLES, BLOG, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

Obama proposed his FY2016 budget on Monday. The budget is filled tax hikes — more than 20 — which are expected to fund more spending schemes cooked up by the President. The tax hikes total about $2 trillion in additional revenue over the next decade. “The administration contends that various spending cuts and tax increases would trim the deficits by about $1.8 trillion over the next decade, leaving the red ink at manageable levels.”

So, just like his yearly spending, so to with his decade budget outlook: despite record tax revenue, Obama’s proposals still don’t balance out. We continue to have deficit spending.

What is in this budget proposal? It’s chock-full of ambitious taxes aimed mainly at the wealthy and businesses. Most of his budget items will likely not pass Congress — and he knows this. At this point in his Presidency, it doesn’t matter anyway what he proposes, or really, what actually passes. And Obama knows this. He’s not running again.

Obama has merely given the Democrats a list of initiatives for them to push, so that they can create anti-Republican narratives using his ideas for litmus tests and sound bytes over the next year to two years heading into the 2016 elections. It’s not about solutions; it’s about creating more divide. Charles Krauthammer got it right when he said, ““Look, I don’t mind if the President sends a budget which he knows is not going to achieve anything. But when he prefaces his remarks as we just saw by saying we have to put politics aside, posing again as the one person in the country who rises above partisanship and party, speaks for the national interest, it’s really grating.”

Here’s the rundown of the list of budget tax hikes. I’ll do some follow up posts about a couple of particularly odious policies contained therein, but for the time being, you can read the entire list of tax increases here. The amounts of revenue noted below are calculated to be collected from the tax increases over the next decade, from 2016 – 2025.

“Limit deductions for top earners to 28 percent rate, even if income is taxed at 39.6 percent: $603.2 billion

Impose a 14 percent one-time tax on previously untaxed foreign income: $268.1 billion

Impose a 19 percent minimum tax on foreign income: $206 billion

Modify estate and gift tax provisions: $214.4 billion

Change the taxation of capital income: $207.9 billion

Other increases from reform of U.S. international tax system: $135.8 billion

Impose a financial fee on large financial companies: $111.8 billion

Increase tobacco taxes and index for inflation: $95.1 billion

Repeal LIFO (Last In First Out) method of accounting for inventories: $76.1 billion

Conform SECA (Self Employed Contributions Act) taxes for professional service businesses: $74.6 billion

Other revenue changes and loophole closers: $47.9 billion

Eliminate oil and natural gas preferences: $45.5 billion

Implement the Buffett Rule by imposing a new “Fair Share Tax” (making millionaires pay at least 30 percent tax rate): $35.2 billion

Reform the treatment of financial and insurance industry products: $34.4 billion

Limit the total accrual of tax-favored retirement benefits: $26.0 billion

Other loophole closers: $24.3 billion

Reinstate Superfund taxes: $21.2 billion

Tax carried interests as ordinary income: $17.7 billion

Make unemployment insurance surtax permanent: $15.7 billion

Eliminate coal preferences: $4.3 billion

Reauthorize special assessment from domestic nuclear utilities: $2.3 billion

Increase and modify Oil Spill Liability Trust Fund financing: $1.6 billion

Repeal tax-exempt bond financing of professional sports facilities: $542.0 million”

by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, QUICKLY NOTED, TAX TIPS, TAXES

Since there seems to be increased interest, and confusion, regarding tax filing and Obamacare this year, it is worth it add some more information to help navigate the process.

The IRS Tax Form 1095a is officially known as the “Health Insurance Marketplace Statement”. If a household member or members enrolled in a healthcare plan through a state or federal exchange, you will receive a 1095a in the mail by early February. You cannot file your taxes without it. It contains information regarding your coverage, such as the number of people enrolled in a marketplace plan, and the dates of effective coverage.

Please note: you will not receive a Form 1095a if you have health coverage through a job or through programs such as Medicaid, Medicare, or the Children’s Health Insurance Program (CHIP).

What you will see on a Form 1095a?

–The form will have information about every member of your household who received Obamacare coverage in 2014. Each person will be listed separately.

–The form will list month-by-month, the amount you paid for your health insurance premium. Each person will be listed separately.

–The form will provide the amount of the “premium tax credits” you received in 2014. They are also called “advanced payments”. This amount is what lowered your monthly premiums, and was calculated based upon income information you provided when you enrolled.

–The form will list the cost of a “benchmark” premium that your premium tax credit is based on. This was the second-lowest cost silver plan, and was considered the “benchmark” to determine subsidies for lower- and moderate-income earners who enrolled in Obamacare.

Why is the 1095a necessary?

The 1095a is your PROOF OF INSURANCE. It contains all the information you need to fill out your form 8965, which is the Premium Tax Credit form. The 8962 Form is a worksheet, whose calculation gets recorded on your 2014 Tax Return.

The main point of all of these forms is really the Premium Tax Credit portion. Remember, 85% of Obamacare enrollees received some sort of subsidy, which is properly known to the IRS as a “Premium Tax Credit”. But most people opted not to receive their tax credit at tax filing time (now). They received it in advance, during 2014, in the form of monthly amounts that were credited against the monthly healthcare premium costs. These advance payments lowered the monthly cost of insurance.

The credit was tabulated based on estimated income information furnished during the application process. But because income situations can change over the course of a year (remember you enrolled at the beginning of 2014), the IRS requires you to re-calculate your income again at tax time (now), and match it against the amount and information you provided when you enrolled.

Since your Premium Tax Credit was based upon estimated income amounts, the amount you were eligible to receive as a tax credit may be higher or lower than what you actually did receive. So, using the information you receive on your 1095a about your household and your payments and your subsidies, you then fill out the Form 8962 to calculate the ACTUAL amount of tax credit you were eligible for in 2014, and check it against what you received as an advance payment applied to your monthly premium costs. Any differences will be resolved either by either reducing or increasing your tax credit amount, which will then affect the final amount of taxes due or taxes returned to you.

Also note — if you enrolled in Obamacare, you must fill out Form 8925, which means you cannot file a 1040EZ. You must file a traditional 1040 tax return.

All the information listed above that you will see on the 1095a is important. If there are any errors, it is imperative that you contact the Obamacare marketplace immediately to resolve the inconsistencies before you file your taxes.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

Since we’ve been discussing it recently.

by | ARTICLES, BUSINESS, ELECTIONS, FREEDOM, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

Ben Casselman penned a piece a year ago in the Wall Street Journal, which documented the decline of risk-taking in business ventures. Hard data showed that both the number of new companies and the use of venture capital is waning. He rightfully suggested that this downward trend is a major contributor to the fact that the recovery from the recent recession is so painfully slow and anemic.

Casselman went on to explain that economists aren’t entirely sure what is behind the decline and gave some potential causes: health care costs, licensing requirements, an aging population, and an increase in large corporations are among some of the suggestions. While these factors do contribute, Casselman missed the glaring elephant in the room: the government, and her anti-business policies, do more to stifle free business activity than any other than any other single mitigating circumstance. Looking at the article a year later, the situation has continued to decline. Here’s how.

This administration has been exceedingly heavy-handed in its efforts to demonize businesses, while promising that businesses will be highly taxed and regulated. Whether it is labor regulation by the NRLB or environmental regulation by the EPA, government interference has been overreaching and restrictive.

Additionally, there have been huge increases in both criminal rules and regulations about what businesses are allowed and not allowed to do — from nitpicky labor rules, to dictating employee minutiae, to minimum wage requirements, all which restrict business hiring — and even employee firing. The EEOC has joined in with several lawsuits against private businesses, deemed by one judge as “laughable”, “based on unreliable data”, and “rife with analytical error”.

More unfortunately, Obama has provided the background for a litigation-friendly environment. If a larger, more financially stable company wants to steal something from a smaller company, they can sue them or just threaten with a costly legal battle. Or, if labor doesn’t like them, they can force them to shut them down as an alternative to litigation. What’s worse, Obama’s Labor Secretary, Thomas Perez, particularly favors the use of “disparate impact” theory with business labor disputes, because, as NRO noted, it “sets a very low bar for proving discrimination. Under it, prosecutors need not prove intent, merely that minorities have suffered a disparate impact from some action”. This man very nearly became the next Attorney General nominee.

More recently, the Obama Administration has decided to wage war on business inversions, by declaring companies who wish to move their headquarters abroad to be “unpatriotic”, and “tax dodgers”. Instead of fixing the root problem — which is that the United States is the only major nation to tax American companies on foreign profits as well as domestic — he instead suddenly tightens the rules for companies and calls the perfectly legal process of inversion to be a “loophole”. Couple that with the fact that we have the highest corporate tax rate in the world, and its no wonder that the United States recently ranked 32 out of 34 countries in the new “International Tax Competitiveness Index”.

Of course, there will be some successes. It just now takes a higher level of skill, ideas, and money to exercise your entrepreneurial spirit. It’s not like there won’t be the Jeffrey Bezos or the Bill Gates or the Steve Jobs. They’ll still come through everything despite the immense impediments. The problem is that it is the middle entrepreneurs who are having a hard time getting started, and even when they do, they will likely get discouraged in the mess. Yet it is precisely this middle group, the bread-and-butter of small businesses, that have made this country great. That future is threatened, as we are seeing now in subtle shifts within the realm of business making.

The future of this country will continue to decline if the anti-business sentiment that Obama has unleashed is allowed to continue. The middle entrepreneurs, the mom-and-pops, the family businesses are the ones that make up the difference between the very tepid growth that we are seeing and the strong growth and recovery that could be better if businesses actually had better opportunity.

Businesses go into business not to comply with government dictates, but to provide a product, a service, to make things. The very liberty for Americans to have the opportunity to succeed and fail, to take risk, to survive, and to thrive is under siege.

by | ARTICLES, BLOG, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAX TIPS, TAXES

This year, taxes will get extra tricky, because filers will be required to account for their health insurance on their forms. There are four ways to do so:

1) For taxpayers who do not have Obamacare, the process is simple: check a box indicating you have insurance. This is U.S. Individual Income Tax Return for 2014, line 61

2) If a person opted not to have any insurance, he or she needs to pay the fine/tax, which has been named the “shared responsibility payment”. This is on U.S. Individual Income Tax Return for 2014, Form 1040, line 61; Form 1040A, line 38; or Form 1040EZ, line 11. The instructions to calculate that are here, on page 5.

3) If you have a Marketplace-granted coverage exemption or you are claiming a coverage exemption on your return, fill out form 8965, and mark it on the U.S. Individual Income Tax Return for 2014, Form 1040, line 62.

4) For those who enrolled in an Obamacare plan through the Marketplace, they will have a more comprehensive section and required forms. Here’s the crucial information you need to know about the Form 1095 (Health Insurance Marketplace Statement) and the Form 8962 (Premium Tax Credit, or PTC).

The 1095a

First — please note, you must have the 1095a form to file your Premium Tax Credit form. If you are filing the Premium Tax Credit form, you can’t file a 1040 EZ form and will need to file a traditional 1040.

Now, the 1095a is a form that will be mailed to each household who enrolled in an Obamacare health insurance exchanges plan, whether it was for your state or it was a federal marketplace. The IRS is very clear: This is your proof of insurance.

The 1095a forms were supposed have arrived by January 31, the same date as W-2s and 1099s, but now it seems the new date is Feb. 2nd. You should also be able to download the 1095a form for your household from the exchange website.

The 8962

“Unfortunately, the Obamacare tax form you’ll get from your health-insurance provider won’t have all of the information you’ll need to report to the IRS. The Premium Tax Credit Form (8962), requires you to refer to your adjusted gross income on your tax return, as well as looking up the appropriate federal poverty line figure for your state. In addition, you’ll need to do many of the calculations to compare the information you provide from Form 1095a with other tax information from elsewhere on your return.”

Why do I need a form for a form?

When you applied for Obamacare coverage, you estimated your earnings for 2014. The exchange used that figure to calculate your Obamacare credit/subsidy. But, things change with income and households. Therefore, the 8962 is a worksheet to calculate the income amount again based on what you actually made in 2014; and if the figures do not match, your credit amount will have to be adjusted.

In order to be extraordinarily helpful to taxpayers wrestling with how to properly file their taxes and include their health insurance information, the IRS has published a 21 page primer. You can view the 21 pages of instructions here. This has links to three long forms and nine tip sheets.

Good luck, everyone!

by | ARTICLES, BLOG, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

Obama has consistently talked about how he is for “tax reform” all during his presidency. But clearly, he has no idea what that even means. True tax reform is a mechanism that produces a cleaner and clearer tax code. A great example of this was the 1986 IRC reform, where Reagan set the highest rate at 28% in exchange for eliminating massive amounts of tax shelters and gimmicks.

Obama’s cluelessness on the topic was evident during the State of the Union, where, instead of the simplification that Obama likes to espouse, we got a myriad of proposals that will further clutter the tax code. You can’t say you are for tax reform and then present a speech filled with the very items that true tax reform would remove, such expanded child care tax credits and new community college initiatives.

It is these very type of policies that have made the tax code so byzantine. Essentially the government uses the tax code to pick winners and losers favoring some but not others such as married vs non-married, children vs non-children, education vs non-education. This is the essence of crony capitalism, where politicians trade favors and barters to support certain initiatives or restrict others via new taxes or credits. They’re basically all gimmicks to aid in reelection or pander to a portion of the electorate — and then we never get rid of all the tacked-on programs and policies because no one wants to give up their special initiatives. The code is immensely complex because of it.

The tax code should never be used in this manner. It’s either a proper tax or not — but you don’t put an item into the tax code and then restrict it to certain people and not others. If someone is making more money, they are subjected to higher tax margins. Fine. But you don’t then add on more crony restrictions or surtaxes to try to squeeze out extra revenue. If a policy is good for the middle guy, it ought to also be good for the wealthier guy — who is already getting dinged accordingly (“paying his fair share”) by paying higher tax rates.

Obama’s version of “tax reform” is unrealistic and firmly rooted in his vision of “middle class economics”. This means using the tax code to promote “fairness” by targeting the wealthy to pay for new spending programs and credits for others. That is not tax reform — that is wealth redistribution.

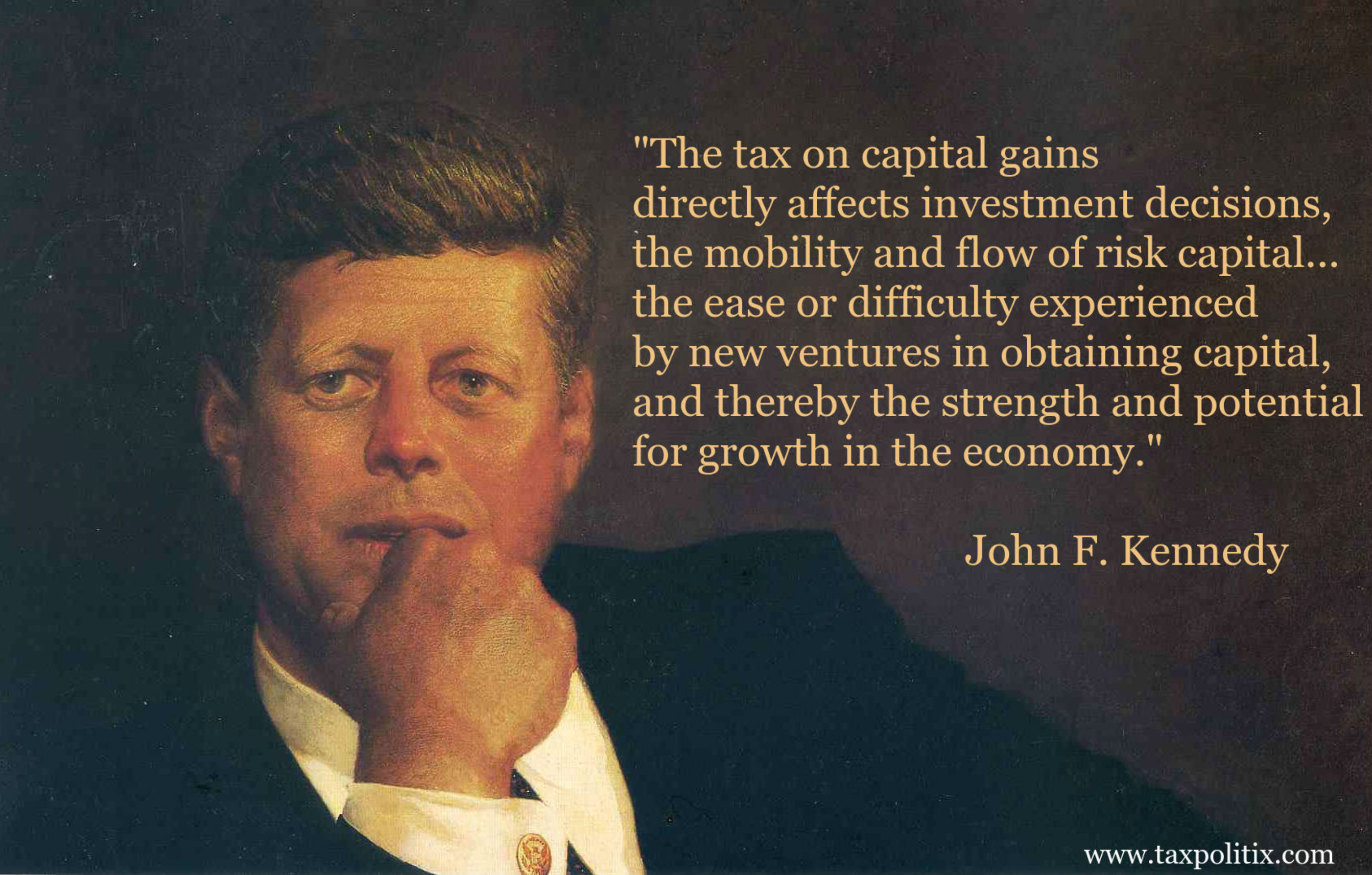

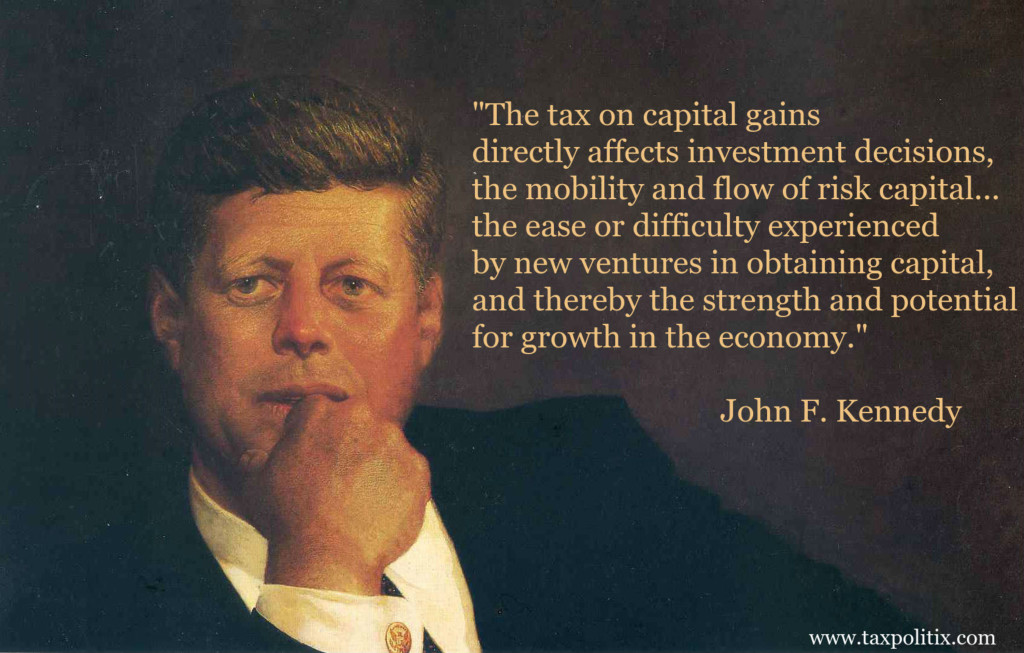

by | ARTICLES, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

President Obama just told the country during his State of the Union address that he is going to increase the capital gains rate again in order to raise revenue for new spending programs. Given that Obama already knows that raising the capital gains rate actually REDUCES revenue, we are left with a President who believes that we can pay for increased spending by reducing revenue. He acknowledged this in 2008 during a televised debate against Hillary Clinton, but went on to state that rates should be hiked – despite its effect of reducing revenue – because it was more “fair” taxation (ludicrous, but a subject for another day).

Extraordinarily and equally disappointing about this fundamental economic error is that no one in the major press outlets, on the day after the State of the Union speech, pointed out the President’s gaffe. Do we really have a President who pushes for paying for increased spending projects with policies that reduce revenue? Or do we have a President who puts forth an initiative that he knows has very little chance of realization, but chooses to do so anyway so he can characterize the Republicans as protecting the wealthy while he can claim to protect the middle class? And did he believe that the press was so clueless that they would not laugh at him the following day?

Capital gains are unusual in that the taxpayer has the ultimate decision as to whether and when to sell his asset (stock, his business, a work of art, etc.) The higher the tax rate, the LESS likely he is to sell, seeing as he will only be able to enjoy or reinvest what is left of the proceeds AFTER TAX. History has borne this out – capital gains tax collections go down in the periods after increases, and go up in the years after decreases.

The actual impact of raising the capital gains rate is also devastating to the economy. By discouraging the sale of assets, there is reduced capital available for new projects and opportunities, reducing job creation and wages, and resulting in lower revenue collection.

Furthermore, with higher capital gain rates, the expected after tax rate of return on new projects will go down, assuring that fewer of them will go forward.

Additionally, there are a number of localities, like the state of California and New York City, which have tax rates of 12% or more and also a large concentration of wealthy people and high performing businesses. Couple that with the proposed increase to the federal capital gains rate and you could see total capital gains rates of more than 44%, A capital gains rate this high would virtually bring elective capital to a standstill. This would amount to a rate more than twice the rate during the Bush Administration (15%) – when growth and the economy were very strong..

Raising the capital gains rate will put a stranglehold on risk taking and available capital. Why sell an asset to fund further investment and opportunity when the government takes a large share of the gain with the loss remaining all yours. It makes virtually no economic sense to do so, and the result means an already anemic economy will continue to struggle.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, OBAMACARE, POLITICS, TAXES

Back in 2008 when Obama was debating Hillary Clinton on national TV, Obama discussed with the moderator how raising the capital gains rate would likely reduce federal revenue collections, but he insisted it was good policy anyway — because it was a policy of “fairness”.

Why would raising the capital gains tax be a revenue loss? The effect of higher taxes slows the economy because those paying the higher capital gains have less money to invest. Unfortunately, such a policy was implemented in 2013 when capital gains went from 15-20% and was coupled with the new 3.8% surtax on investment income to pay for Obamacare, making the rate 23.8%.

Now he wants to tax, yet again, the very type of taxpayers who have money to create jobs and/or invest, by raising the capital gains rate up to 28%. This is essentially about an 18% tax hike on high income earners — two years after the last capital gains rate increase. That’s practically doubling the rate in just a few short years. And during this time, the economy has remained sluggish.

It’s a shame that Obama continues to push for policies that would have a negative effect on jobs and the economy in an effort to promote “fairness through taxation” and pay for his pet projects (such as free community college!). The concept of an American President continuing to go after people making a lot of money it is particularly loathsome; it also displays an absolute lack of familiarity with and respect for how people get wealthy — he just wants their hard-earned money.

Back in 2008 during that same debate, Obama claimed, “What I want is not oppressive taxation. I want businesses to thrive, and I want people to be rewarded for their success. But what I also want to make sure is that our tax system is fair and that we are able to finance health care for Americans who currently don’t have it and that we’re able to invest in our infrastructure and invest in our schools. And you can’t do that for free.”

But with Obama, you can do it by wealth transfer.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAXES

The question of raising the minimum wage keeps getting pushed at the federal level, as well as across many states. If we are to educate the populace on the pitfalls of arbitrary “minimum wage” hikes, we must be sure to argue the inherent flaws of suggestion that minimum wage hikes help some people and therefore are good for everyone.

This was illustrated recently on an episode of CNBC’s “On the Money” with Becky Quick. On one side was Dan Mitchell of CATO, who has done admirable work on fiscal policy and economics over there for many years. Opposite him was Jared Bernstein, a former Chief Economist and Economic Adviser to Vice President Joseph Biden. Mitchell’s appearance on the show, however, was a bit of a disappointment on the issue of minimum wage.

There were two major points he seemed to miss. The first was in regard to the effect of a minimum wage hike on workers. Mitchell pointed out, correctly, that 500,000 people would lose their jobs, to which his opponent, Jared Bernstein, countered that 24 million people would gain more money (“get out of poverty” per the CBO), and therefore, quantitatively, people would benefit in a 50-1 ratio. But that is wrong!

Those 24 million, though they may benefit from a raise, will really one see a few cents more an hour. Those that lose their jobs, will lose not only $7.50 an hour in comparison, but also the opportunity to learn working skills and actually have a job from which they can advance in the workforce. Even if Bernstein’s figures were perfectly accurate – which they were not – having 24 million people earn a few more cents per hour versus the entire loss of jobs and livelihood do not make raising the minimum wage worthwhile.

But that point is secondary. The primary issue – and the one that Mitchell (as well as all of us who understand the economics of minimum wage) seem to be unable counter to the Jared Bernsteins of the world – relates to the economic cost of a minimum wage. He needed to explain to Mr. Bernstein that the apparent extra money going to those getting the higher minimum wage is, in fact, detrimental to the economy as a whole, and therefore ultimately to even those people it was intended to help.

Economics 1a would explain (looking for “what is unseen” ) that the extra money going to those benefiting must be coming from somewhere (though providing no extra result). It is coming from either a) lower wages paid to other employees, b) lower profits to the business, which lowers rate of return directly reducing new investments in that business and reducing the likelihood that new businesses will be started, or c) higher prices to the consumer, which (Economics 1a again) shows will reduce total sales volume, and therefore GDP as a whole..

Though Mitchell did successfully argue the merits of how minimum wages certainly shouldn’t be a federal law, but rather a state consideration, he missed entirely the ability to counter the false argument concerning the minimum wage altogether. If we don’t oppose and expose the core flaws, we will certainly continue to lose in the public square on the issue of minimum wage.

by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, HYPOCRISY, OBAMA, POLITICS, TAXES

President Obama ended the State of the Union address in a new way. He didn’t say, as tradition, “God bless you, and God bless these United States of America”

He said, “Thank you, God bless you, and God bless this country we love.”

A quick check on his prior SOTU speeches reveals he used the customary phrasing in past years:

2014: God bless you, and God bless the United States of America.

2013: “Thank you. God bless you, and God bless these United States of America”

2012: “Thank you. God bless you, and God bless these United States of America”

2011: ” Thank you. God bless you, and may God bless the United States of America. ”

2010: “Thank you. God bless you. And God bless the United States of America.”

What happened to “God bless the United States of America”?

Update #1: It is fairly standard for the President to end his speech this way, at least in modern times. Curious as to the reason for the shift. Here’s a little background comparison:

“Presidents from Roosevelt to Carter did sometimes conclude their addresses by seeking God’s blessing, often using language such as ‘May God give us wisdom’ or ‘With God’s help.’ But they didn’t make a habit of it. In fact, five of the eight presidents during this period concluded this way in less than 30% of their speeches. Harry Truman, Lyndon Johnson and Ford did so a bit more often, but still none of these presidents concluded even half of his addresses this way. Reagan, on the other hand, ended 90% of his major addresses by requesting divine guidance. George H.W. Bush also did so in 90% of his speeches, and Bill Clinton and George W. Bush followed suit 89% and 84% of the time, respectively.”

Update #2: Apparently, Joni Ernst said roughly the same thing. “”May God bless this great country of ours, the brave Americans serving in uniform on our behalf, and you, the hardworking men and women who make the United States of America the greatest nation the world has ever known.”

Was it a mirror to Obama’s ending? The custom, obviously, is not expected by others as it is by the President, which is why it was noticeable when Obama ended his speech. Thoughts?