by | ARTICLES, BUSINESS, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAX TIPS, TAXES

The Fix the Debt Campaign Steering Committee is a bipartisan group of prominent leaders and experts, including luminaries such as Erskine Bowles and Alan Simpson, the co-chairs of the White House Fiscal Commission. The Fix the Debt group put together some decent graphics regarding federal spending.

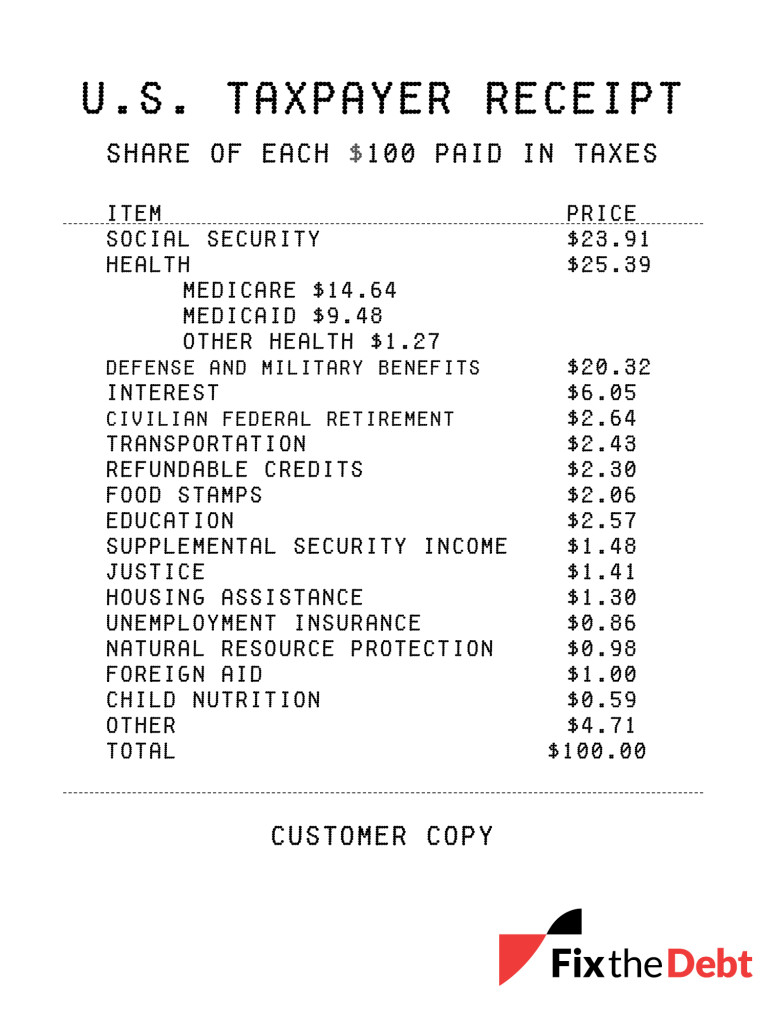

This is a “taxpayer receipt” highlighting where the money goes and highlight where it comes from in the first place.

How are our federal tax dollars spent? As the taxpayer receipt illustrates, more than $75 of every $100 paid in federal taxes goes to Social Security, federal health care, defense, and interest on the debt. And the amounts for Social Security, health care, and interest are forecast to grow considerably in the years to come.

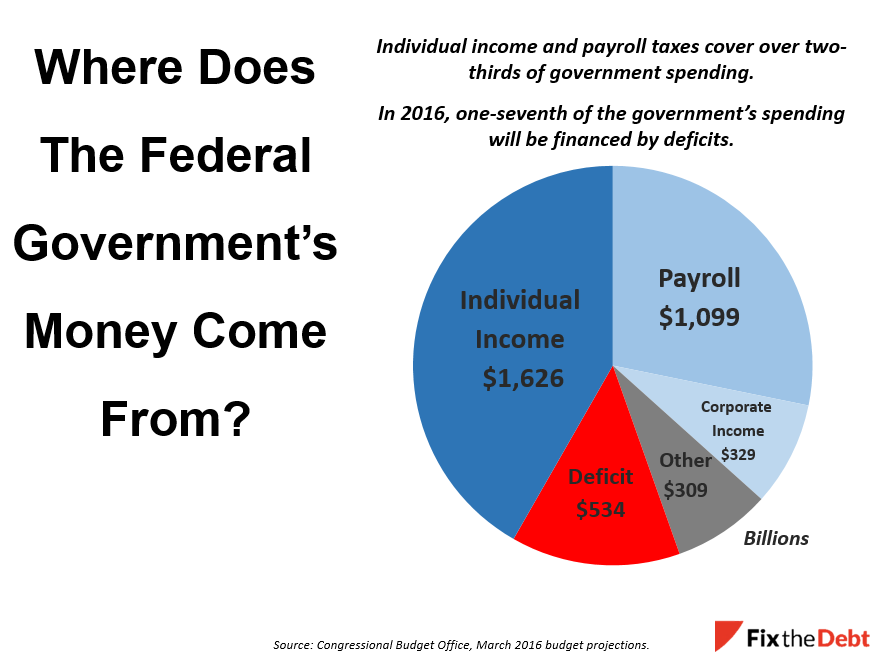

Where does the money come from? Much of the revenue for the federal government comes from the individual income tax that many of us are rushing to complete. Another major source is the payroll tax, which is the “FICA” tax that is withheld from your paycheck. It is used to fund Social Security benefits and parts of Medicare.

But a significant part of the government is deficit financed because spending exceeds revenue. That share is expected to grow substantially in the years ahead.

Check out their blog for more information.

by | ARTICLES, BLOG, BUSINESS, CONSTITUTION, FREEDOM, OBAMA, OBAMACARE, TAX TIPS, TAXES

Find Out How ACA affects Employers with 50 or More Employees

Some of the provisions of the health care law apply only to large employers, which are generally those with 50 or more full-time equivalent employees. These employers are applicable large employers – also known as ALEs – and are subject to the employer shared responsibility provisions.

Information Reporting

Applicable large employers have annual reporting responsibilities concerning whether and what health insurance they offered to their full-time employees during the prior year. In 2016, the deadline to provide Forms 1095-C to full-time employees is March 31. The deadline by which ALEs must file information returns with the IRS is no later than May 31 or June 30 if filed electronically.

All employers, regardless of size, that provide self-insured health coverage must file an annual return reporting certain information for individuals they cover. In 2016, the deadline by which self-insured ALEs must provide Forms 1095-C to responsible individuals is March 31. The returns with 2015 information are due no later than May 31 or June 30 if filed electronically.

Employer Shared Responsibility Payment

ALEs are subject to the employer shared responsibility payment if at least one full-time employee receives the premium tax credit and any one these conditions apply. The ALE:

- failed to offer coverage to full-time employees and their dependents

- offered coverage that was not affordable

- offered coverage that did not provide a minimum level of coverage

SHOP Marketplace

Employers with more than 50 cannot purchase health insurance coverage for its employees through the Small Business Health Options Program – better known as the SHOP Marketplace. However, Employers that have exactly 50 employees can purchase coverage for their employees through the SHOP.

For more information, visit the Determining if an Employer is an Applicable Large Employer page on IRS.gov/aca.

by | ARTICLES, BLOG, CONSTITUTION, FREEDOM, GOVERNMENT, POLITICS, TAX TIPS, TAXES

We’re coming up on three years since the IRS scandal broke in May 2013. Most Americans have certainly forgotten about it, especially since the former head, Lois Lerner, went wholly unpunished. But some targeted groups have not forgotten about it, and continue to fight for transparency with the entire affair.

Earlier this week, a federal appeals court “ordered the IRS to quickly turn over the full list of groups it targeted so that a class-action lawsuit, filed by the NorCal Tea Party Patriots, can proceed. The judges also accused the Justice Department lawyers, who are representing the IRS in the case, of acting in bad faith — compounding the initial targeting — by fighting the disclosure.”

The IRS, of course, claimed that no targeting happened — that it was merely an issue of poorly trained employees. Of course, we all know better. A vast majority of the targets were conservative or tea-party groups, there were secret buzz words to identify them, and some of the groups still have not attained 501c3 status after 5 years!

According to the Washington Times, Tea Party groups have been trying for years to get a full list of nonprofit groups that were targeted by the IRS, but the IRS had refused, saying that even the names of those who applied or were approved are considered secret taxpayer information. The IRS said section 6103 of the tax code prevented it from releasing that information.

Judge Kethledge, however, said that turned the law on its head. ‘Section 6103 was enacted to protect taxpayers from the IRS, not the IRS from taxpayers,’ he wrote.”

This particular ruling certified the NorCal case as a class-action lawsuit. Others who were targeted may be permitted to join the case, but until that list is revealed, it is unknown who exactly among the 200 or so groups involved were actually targeted.

Now, “the case moves to the discovery stage, where the tea party groups’ lawyers will ask for all of the agency’s documents related to the targeting and will depose IRS employees about their actions.”

As a CPA intimately involved with the IRS for many years, I have been following this case since the beginning and have continued to report on updates. The actions of the IRS were particularly egregious and overreaching, and no one was appropriately punished for it. It’s good that some of the groups remain dedicated to getting more answers that what has been divulged by the Department of Justice to date.

by | ARTICLES, BUSINESS, GOVERNMENT, TAX TIPS, TAXES

Tax Refund Offsets Pay Unpaid Debts

If you can’t pay your taxes in full, the IRS will work with you. Past due debts like taxes owed, however, can reduce your federal tax refund. The Treasury Offset Program can use all or part of your federal refund to settle certain unpaid federal or state debts, to include unpaid individual shared responsibility payments. Here are five facts to know about tax refund offsets.

1. Bureau of the Fiscal Service. The Department of Treasury’s Bureau of the Fiscal Service, or BFS, runs the Treasury Offset Program.

2. Offsets to Pay Certain Debts. The BFS may also use part or all of your tax refund to pay certain other debts such as:

Federal tax debts.

Federal agency debts like a delinquent student loan.

State income tax obligations.

Past-due child and spousal support.

Certain unemployment compensation debts owed to a state.

3. Notify by Mail. The BFS will mail you a notice if it offsets any part of your refund to pay your debt. The notice will list the original refund and offset amount. It will also include the agency that received the offset payment. It will also give the agency’s contact information.

4. How to Dispute Offset. If you wish to dispute the offset, you should contact the agency that received the offset payment. Only contact the IRS is your offset payment was applied to a federal tax debt.

5. Injured Spouse Allocation. You may be entitled to part or the entire offset if you filed a joint tax return with your spouse. This rule applies if your spouse is solely responsible for the debt. To get your part of the refund, file Form 8379, Injured Spouse Allocation. If you need to prepare a Form 8379, you can prepare and e-file your tax return for free using IRS Free File.

Health Care Law: Refund Offsets and the Individual Shared Responsibility Payment

While the law prohibits the IRS from using liens or levies to collect any individual shared responsibility payment, if you owe a shared responsibility payment, the IRS may offset your refund against that liability.

Each and every taxpayer has a set of fundamental rights they should be aware of when dealing with the IRS. These are your Taxpayer Bill of Rights. Explore your rights and our obligations to protect them on IRS.gov.

Additional IRS Resources:

Tax Topic 203 – Refund Offsets

by | ARTICLES, GOVERNMENT, TAX TIPS, TAXES

Military Members: Get Free Tax Help

The IRS offers free tax help to members of the military and their families through the Volunteer Income Tax Assistance program. VITA is available both on and off base including sites for military members overseas. Here are five tips to know about free tax help for the military:

1. Armed Forces Tax Council. The Armed Forces Tax Council oversees the military tax programs offered worldwide.

2. Certified Staff. Military VITA certified employees staff their sites. They receive training on military tax issues, like tax benefits for service in a combat zone. They can help you with special extensions of time to file your tax return and to pay your taxes or with special rules that apply to the Earned Income Tax Credit.

3. What to Bring. Take the following records with you to your military VITA site:

- Valid photo identification.

- Social Security numbers for you, your spouse and dependents; or individual taxpayer identification numbers (ITINs) or adoption taxpayer identification numbers (ATINs) for those who don’t have Social Security numbers.

- Birth dates for you, your spouse and dependents.

- Your wage and earning forms, such as Forms W-2, W-2G, and 1099-R.

- Interest and dividend statements (Forms 1099).

- Health coverage information forms such as Form 1095-A, 1095-B or 1095-C.

- Exemption Certificate Number for exemptions that you obtained through the Marketplace.

- A copy of your last year’s federal and state tax returns, if available.

- Routing and account numbers for direct deposit of your tax refund.

- Total amount you paid for day care and the day care provider’s identifying number. This is usually an Employer Identification Number or Social Security number.

- Other relevant information about your income and expenses.

4. Joint Returns. If you are married filing a joint return, generally both you and your spouse need to sign. If you both can’t be present to sign the return, you should bring a valid power of attorney form unless you are eligible for an exception. Publication 501, Exemptions, Standard Deduction, and Filing Information, has more details.

5. Health Care Tax Law Help. IRS Free File can help with tax provisions of the health care law. The software will walk you through the lines on the tax forms that relate to the Health Care Law. If your income was $62,000 or less, you qualify for Free File software. If you made more than $62,000, you can use Free File Fillable Forms.

Each and every taxpayer has a set of fundamental rights they should be aware of when dealing with the IRS. These are your Taxpayer Bill of Rights. Explore your rights and our obligations to protect them on IRS.gov.

Additional IRS Resources:

Military Pay Exclusion – Combat Zone Service

Publication 4940, Tax Information for Active Duty Military and Reserve Personnel

Publication 3, Armed Forces’ Tax Guide

Gathering Your Health Coverage Documentation

IRS YouTube Videos:

Military Tax Tips – English | Spanish

by | ARTICLES, GOVERNMENT, TAX TIPS, TAXES

Interest Rates Remain the Same for the Second Quarter of 2016

WASHINGTON – The Internal Revenue Service today announced that interest rates will remain the same for the calendar quarter beginning April 1, 2016. The rates will be:

- three (3) percent for overpayments [two (2) percent in the case of a corporation];

- one-half (0.5) percent for the portion of a corporate overpayment exceeding $10,000.

- three (3) percent for underpayments; and

- five (5) percent for large corporate underpayments.

Under the Internal Revenue Code, the rate of interest is determined on a quarterly basis. For taxpayers other than corporations, the overpayment and underpayment rate is the federal short-term rate plus 3 percentage points.

Generally, in the case of a corporation, the underpayment rate is the federal short-term rate plus 3 percentage points and the overpayment rate is the federal short-term rate plus 2 percentage points. The rate for large corporate underpayments is the federal short-term rate plus 5 percentage points. The rate on the portion of a corporate overpayment of tax exceeding $10,000 for a taxable period is the federal short-term rate plus one-half (0.5) of a percentage point.

The interest rates announced today are computed from the federal short-term rate determined during Jan. 2016 to take effect Feb. 1, 2016, based on daily compounding.

Revenue Ruling 2016-06, announcing the rates of interest, is attached and will appear in Internal Revenue Bulletin 2016-13, dated March 28, 2016.

by | ARTICLES, BUSINESS, ECONOMY, GOVERNMENT, OBAMA, POLITICS, TAX TIPS, TAXES

CNSNews remains a go-to source for analyzing information on the U.S. Treasury, tax revenue, and such. Here they are again, scrutinizing tax receipts for FY2016 through the end of February. In a nutshell, the U.S. government continues to run a deficit, and the amount of taxpayer responsibility continues to increase. From CNSNEWS:

The U.S. Treasury hauled in a record of approximately $1,248,371,000,000 in tax revenues in the first five months of fiscal 2016 (Oct. 1, 2015 through Feb. 29, 2016), according to the Monthly Treasury Statement released today.

Despite these record tax revenues in the first five months of the fiscal year, the federal government nonetheless ran a deficit of approximately $353,005,000,000 during the same period.

In February alone, the Treasury ran a deficit of $192,614,000,000.

The record five-month tax haul of $1,248,371,000,000 equaled approximately $8,263 for each of the 151,074,000 people in the country who had either a full or part-time job in February.

The record taxes in the first five months of this fiscal year exceed by about $63,263,220,000 in constant 2016 dollars the then-record $1,185,107,780,000 in tax revenues (in constant 2016 dollars) that the Treasury took in during the first five months of fiscal 2015.

However, even while taking in a record $1,248,371,000,000 in tax revenues from October through February, the Treasury was spending $1,601,375,000,000, according to the Monthly Treasury Statement. Thus, so far this fiscal year, the Treasury has run a deficit of $353,005,000,000.

The largest source of revenue in the first five months of this fiscal year was the individual income tax, which brought the Treasury $597,524,000,000. The second largest source was Social Security and other payroll taxes, which brought in $428,181,000,000.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, GOVERNMENT, POLITICS, TAX TIPS, TAXES

Every year, the various tax agencies calculate how many Americans do not pay a federal income tax. The 2015 tax year number estimates that 77.5 million households, which is 45.3%, according to the research Tax Policy Center. This number is only for federal taxes and does not include state income taxes.

There are two main reasons for the lack of federal taxes: either the household has no taxable income, or their tax liability is reduced and offset by tax breaks.

The research also calculated the various income levels from the richest and the poorest.

“The top 1 percent of taxpayers pay a higher effective income tax rate than any other group (around 23 percent, according to a report released by the Tax Policy Center in 2014) — nearly seven times higher than those in the bottom 50 percent.

On average, those in the bottom 40 percent of the income spectrum end up getting money from the government. Meanwhile, the richest 20 percent of Americans, by far, pay the most in income taxes, forking over nearly 87 percent of all the income tax collected by Uncle Sam.

The top 1 percent of Americans, who have an average income of more than $2.1 million, pay 43.6 percent of all the federal individual income tax in the US; the top 0.1 percent — just 115,000 households, whose average income is more than $9.4 million — pay more than 20 percent of it.”

Federal taxes are not the only taxes that Americans pay. Income, payroll, corporate income, state, local, property taxes, estate taxes, and excise taxes (which include taxes on gasoline, alcohol and cigarettes), are all various forms of taxation that are spread out and paid by households daily.

by | ARTICLES, GOVERNMENT, TAX TIPS, TAXES

Capital Gains and Losses – 10 Helpful Facts to Know

When you sell a capital asset, the sale normally results in a capital gain or loss. A capital asset includes most property you own for personal use or own as an investment. Here are 10 facts that you should know about capital gains and losses:

1. Capital Assets. Capital assets include property such as your home or car, as well as investment property, such as stocks and bonds.

2. Gains and Losses. A capital gain or loss is the difference between your basis and the amount you get when you sell an asset. Your basis is usually what you paid for the asset.

3. Net Investment Income Tax. You must include all capital gains in your income and you may be subject to the Net Investment Income Tax if your income is above certain amounts. The rate of this tax is 3.8 percent. For details, visit IRS.gov.

4. Deductible Losses. You can deduct capital losses on the sale of investment property. You cannot deduct losses on the sale of property that you hold for personal use.

5. Limit on Losses. If your capital losses are more than your capital gains, you can deduct the difference as a loss on your tax return. This loss is limited to $3,000 per year, or $1,500 if you are married and file a separate return.

6. Carryover Losses. If your total net capital loss is more than the limit you can deduct, you can carry it over to next year’s tax return.

7. Long and Short Term. Capital gains and losses are treated as either long-term or short-term, depending on how long you held the property. If you held it for one year or less, the gain or loss is short-term.

8. Net Capital Gain. If your long-term gains are more than your long-term losses, the difference between the two is a net long-term capital gain. If your net long-term capital gain is more than your net short-term capital loss, you have a net capital gain.

9. Tax Rate. The tax rate on a net capital gain usually depends on your income. The maximum tax rate on a net capital gain is 20 percent. However, for most taxpayers a zero or 15 percent rate will apply. A 25 or 28 percent tax rate can also apply to certain types of net capital gain.

10. Forms to File. You often will need to file Form 8949, Sales and Other Dispositions of Capital Assets, with your federal tax return to report your gains and losses. You also need to file Schedule D, Capital Gains and Losses, with your tax return.

For more information about this topic, see the Schedule D instructions and Publication 550, Investment Income and Expenses. You can visit IRS.gov to view, download or print any tax product you need right away.

Each and every taxpayer has a set of fundamental rights they should be aware of when dealing with the IRS. These are your Taxpayer Bill of Rights. Explore your rights and our obligations to protect them on IRS.gov.

Additional IRS Resources:

Form 8960, Net Investment Income Tax— Individuals, Estates, and Trusts

Capital Gains and Losses

by | ARTICLES, GOVERNMENT, TAX TIPS, TAXES

Free Help Preparing Tax Returns Available Nationwide

IRS YouTube Videos:

Free Help Preparing your Tax Return: English | Spanish | ASL

WASHINGTON –– The Internal Revenue Service reminded taxpayers today that they may be eligible to receive free tax help at more than 12,000 preparation sites available nationwide. The sites, generally located at community and neighborhood centers, provide tax assistance to taxpayers with low- and moderate-incomes and the elderly.

The IRS Volunteer Income Tax Assistance (VITA) program offers free tax help to individuals who generally make 54,000 or less, persons with disabilities, the elderly and individuals with limited English proficiency who need assistance in preparing their taxes. The Tax Counseling for the Elderly (TCE) program offers free tax help for all taxpayers, particularly those who are 60 and older. VITA and TCE volunteers are trained and certified by the IRS to help with many tax questions, including credits such as the Earned Income Tax Credit (EITC) and the Child and Dependent Care Credit.

The Earned Income Tax Credit (EITC) is a significant tax credit for workers who earned $53,267 or less in 2015. Last year, more than 27.5 million eligible workers and families received almost $66.7 billion in EITC, with an average EITC amount of more than $2,400. The maximum EITC amount for 2015 is $6,242 for qualifying families. In order to receive the credit, eligible taxpayers must file a tax return, even if they do not have a filing requirement. The VITA and TCE programs can help answer many EITC questions and help taxpayers claim the credit if they qualify. Taxpayers may also use the IRS.gov EITC Assistant to help them determine their eligibility.

Before visiting a VITA or TCE site, taxpayers should review Publication 3676-B to be aware of the services provided. To find the nearest VITA or TCE site, taxpayers can use the VITA and TCE locator tool available on IRS.gov, download the IRS smartphone app IRS2GO or call 800-906-9887.

For assistance preparing a tax return at a VITA or TCE site, taxpayers must bring all required documents and information including:

Proof of identification (photo ID)

Social Security cards for the taxpayer, spouse and dependents

An Individual Taxpayer Identification Number (ITIN) assignment letter may be substituted for those who do not have a Social Security number

Proof of foreign status, if applying for an ITIN

Birth dates for the taxpayer, spouse and dependents

Wage and earning statements (Form W-2, W-2G, 1099-R,1099-Misc) from all employers and other payers

Interest and dividend statements from banks (Forms 1099)

All Forms 1095, Health Insurance Statements

Health Insurance Exemption Certificate, if received

A copy of last year’s federal and state returns, if available

Proof of bank account routing and account numbers for direct deposit such as a blank check

To file taxes electronically on a married-filing-joint tax return, both spouses must be present to sign the required forms

Total amount paid for daycare services and the daycare provider’s tax identifying number such as their Social Security number or business Employer Identification Number

Form 1095-A, Form 1095-B or Form 1095-C, Affordable Health Care Statements

Copies of income transcripts from IRS and state, if applicable

The military also partners with the IRS to provide free tax assistance to military personnel and their families. The Armed Forces Tax Council (AFTC) consists of the tax program coordinators for the Army, Air Force, Navy, Marine Corps and Coast Guard. The AFTC oversees the operation of the military tax programs worldwide, and serves as the main conduit for outreach by the IRS to military personnel and their families. Volunteers are trained and equipped to address military specific tax issues, such as combat zone tax benefits and the effect of the EITC guidelines.

In addition to free tax return preparation assistance, most sites will file returns electronically for free. Combining e-file with direct deposit is the fastest and most accurate way to file. The IRS issues nine out of 10 refunds in 21 days or less. Paper returns take longer to process. Taxpayers who chose to file electronically and owe, can make a payment by the April 18, 2016 deadline using Direct Pay. This IRS free service allows taxpayers to make secure payments from a checking or savings account.

Taxpayers that prefer to file their own tax returns electronically have the option of using IRS Free File. IRS Free File offers brand-name tax software to taxpayers who earned 62,000 or less in 2015 to file their returns for free. Taxpayers who earned more can use Free Fillable Forms, the electronic version of IRS paper forms. IRS Free File is only available through the IRS website by visiting IRS.gov/freefile.