by | ARTICLES, BLOG, BUSINESS, FREEDOM, GOVERNMENT, POLITICS, TAX TIPS, TAXES

The IRS announced this morning that a hardware failure occurred sometime yesterday afternoon; because of this, tax processing systems are not currently not functioning correctly.

As a result of the failure, the IRS is unable to accept tax returns filed electronically, and may also have difficultly processing refunds; however, they do not believe that “major disruptions” will occur long-term. By-and-large, 90% of taxpayers should still be able to get their refunds within 21 days.

If you visit IRS.gov, the website is up and running by some features are unavailable, such as “Where’s My Refund?” The outage will likely continue throughout the day today. Taxpayers who use services and companies that file their electronic return will see their return filing on hold until the system is properly restored.

UPDATE:

E-filing had been restored but the cause remains unknown. The IRS has assured taxpayers that hackers don’t appear to be involved; an IRS spokesman said it looked to be a “power or electrical issue” but did not provide any more substance on the matter.

According to Bloomberg, “The system failure occurred at a center in West Virginia, according to the person with knowledge off the matter. Agency officials were trying to determine if any other facilities were affected.

The IRS website lists several facilities in West Virginia; it wasn’t clear which might have been affected. IRS sites there include at least two “enterprise computing centers” in Martinsburg and Kearneysville and the Beckley Finance Center in Beckley. The finance center, part of the IRS’s chief financial office, processes payments for manual transactions and electronic payment files and helps handle the agency’s general ledger, according to the website.”

The IRS is sure to argue that budget cuts are the reason why such an episode occurred, as basic taxpayer functions have eroded over the past few years. Of course, the IRS scandals that continue to plague the agency don’t help improve its image.

by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

As the federal debt hits $19 trillion, the Daily Caller is reporting that the government misled Congress over debt limit solutions during 2011 and 2013. A new report has just been issued by the House Financial Services Committee the outlines the behind-the-scenes machinations. You can read the report in full here.

The Daily Caller gives a full summary here; I’ve re-posted their article in its entirety below:

“Federal Reserve Bank of New York officials secretly conducted real-time exercises during the 2011 and 2013 debt-limit crisis that demonstrated the federal government could function during a temporary shutdown by prioritizing spending, even as Treasury Secretary Jack Lew publicly claimed many times that such efforts were “unworkable,” according to a new report by the House Financial Services Committee obtained by The Daily Caller News Foundation.

The staff report, to be released Tuesday, charges that Lew and other Obama administration officials deliberately misled Congress and the public during the federal budget and debt limit showdowns in both years. The committee will convene a public hearing on the report Feb. 2.

The report also states that the Obama administration crafted actual contingency plans to pay for Social Security and veterans benefits, as well as principal and interest on the national debt if the government was temporarily unable to borrow more money. The Committee concludes that over the last two years the Treasury Department has “obstructed” congressional efforts to get to the bottom of the administration’s real-time policy during the two showdowns.

The Constitution stipulates that only Congress can determine how much money the federal government can borrow. Presidents thus cannot unilaterally spend beyond congressional debt ceiling limits set. The committee — chaired by Republican Rep. Jeb Hensarling of Texas — charged that during both confrontations, the Obama administration held the country’s creditworthiness “hostage” by claiming default was the only possibility if the debit ceiling was not raised.

“These internal documents show the Obama Administration took the nation’s creditworthiness and economy hostage in a cynical attempt to create a crisis so the president could get what he wanted during negotiations over the debt ceiling,” Hensarling said in a statement to be released with the report Tuesday.

The report also revealed that the Treasury Department did not publicly divulge its plans to prioritize payments “for the express purpose of creating market uncertainty in an effort to pressure Congress to acquiesce in the administration’s ‘no negotiation’ posture on the debt ceiling.”

Wisconsin Republican Rep. Sean Duffy, the financial services panel’s oversight subcommittee chairman, said the administration “manufactured a crisis to put politics ahead of economic stability.”

The massive, 322-page report chronicles frank, behind-the-scenes discussions among Federal Reserve Board and Federal Bank of New York officials as Congress debated whether to keep existing debt limits or allow Treasury to borrow more money. The House committee and the Treasury Department have been fighting a bitter, two-year battle over Federal Reserve documents.

The report states that “Treasury apparently directed the New York Fed not to answer valid congressional oversight inquiries because Treasury knew the answers would expose the dishonesty of the administration’s public statements.”

A Treasury Department spokesman told TheDCNF, “Treasury has been committed to working cooperatively with the Committee to provide it with the information it needs,” including providing it with the New York Fed documents. The report is based on 3,878 pages of internal documents the committee eventually acquired despite Treasury’s opposition. The panel finally obtained the documents by subpoena. The report contains 41 separate appendices.

The revelations will likely add new intensity to the long-running public debate on the proper level of federal spending as the 2016 election campaign accelerates with Monday’s Iowa presidential caucus and next week’s New Hampshire presidential primary. Obama administration officials repeatedly declared that a complete government shutdown with no partial or interim payments was the only alternative to congressional approval of an increased debt ceiling.

In testimony Oct. 13, 2013, before the Senate Finance Committee, for example, Lew said the government could not “pick and choose” the funding of individual government programs once the debt limit ceiling was reached.

“I do not believe there is a way to pick and choose on a broad basis. The system was not designed to be turned off selectively,” Lew said.

The Federal Reserve documents revealed in the report show the Obama administration was in fact prepared to pick and choose which payments to make “in order to protect the creditworthiness of the United States.”

An internal e-mail from an official in the New York Fed’s Financial Institution Supervision Group states that regardless of the congressional outcome, “Treasury is adamant they will make [Principal and Interest] payments. Not considering possibility of missing debt payments.” The P&I payments are made to Treasury bond holders.

“At the same time that Treasury was insisting to Congress and the American people that prioritization is unworkable, Treasury and New York Fed officials were working behind the scenes on a prioritization plan,” the report charges.

In private, Federal Reserve Board Federal Reserve Bank of New York officials vigorously denounced the administration’s secrecy over its contingency planning, one calling it “crazy, counter-productive, and add[ing] risk to an already risky situation.”

Federal Reserve Governor Jerome H. Powell, for example, complained that the administration tactics were part of political brinkmanship. “Treasury wants to maximize pressure on Congress by limiting communications on contingency planning,” he said in an email.

The report noted that both the Federal Reserve Board of Governors and the Federal Bank of New York had “grave concerns with Treasury’s political decision not to inform the public of the administration’s debt ceiling contingency plans.”

The Federal Reserve Board staff “strongly encouraged Treasury to reveal its plan in advance” so that the private sector could prepare properly for a debt ceiling event but Treasury officials were “very reluctant to do so,” according to the report.

The Federal Reserve documents also depict officials at the Federal Bank of New York twice engaging in intense “tabletop exercises” about how government agencies could operate under a spending limit.

A March 16, 2011, table-top exercise included an hour-by-hour simulation of how 29 governmental agencies and market players would react when the federal government reached its debt limit.

At the time, the federal government would be within $25 million of its $14.3 trillion budget limit. The Secretary of the Treasury would invoke the Federal Reserve Debt Ceiling Crisis procedures, which provide that the “The President and the Secretary of the Treasury meet with the Fed Chairman at noon and agree that the Federal Reserve should pursue actions to honor and settle SSI, veterans benefits and P&I payments.” SSI refers to Social Security and disability payments.

A similar April 9, 2013, debt ceiling table-top exercise focused on a “scenario” in which “Treasury begins controlling the flow of payments” and in which ”SSI, veterans benefits and P&I payments [would] be prioritized over all other governmental obligations.” The debt ceiling was $16.3 trillion at the time of the second exercise.

The procedures also state that “based on direction from the President, Treasury will pay only selected type of payments and withhold other government payments.”

Both Moody’s and Goldman Sachs publicly suggested during the 2013 crisis that it was possible the government could assure markets by pledging to pay principal and interest, Social Social and veterans benefits.

When contacted by TheDCNF, the Treasury Department did not directly address the issue of prioritizing payments but forwarded an October 16, 2015 blog, which stated in part, “The New York Fed’s system would be technologically capable of continuing to make principal and interest payment,” but added, “this approach would be entirely experimental and create unacceptable risk to both domestic and global financial markets.”

Multiple think tanks, including the Mercatus Center, have released reports suggesting numerous alternatives to default if the debt limit ceiling is not increased.

The national debt limit has tripled under Obama and now stands at $18.9 trillion.”

by | ARTICLES, BLOG, ECONOMY, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

When President Obama took office in 2009, the United States ranked as the 6th best country in the world in terms of economic freedom. Now, in the last year of his term, the United States doesn’t even rank in the top ten anymore.

This year, the Index placed the United States as the 11th most economically free country. This is a significant loss. As noted by the Index, “Economic freedom is a crucial component of liberty. It empowers people to work, produce, consume, own, trade, and invest according to their personal choices.”

Five countries were ranked as “FREE”, meaning they scored 80-100% Those countries are: Hong Kong, Singapore, New Zealand, Switzerland, and Australia.

Rounding out the top ten are: Canada (6), Chile (7), Ireland (8), Estonia (9), and the United Kingdom (10). With the United States ranking 11th, we have our worst score ever recorded. 8 of the last 9 years have seen losses of economic freedom; with this ranking, we have essentially lost a decade worth of economic prosperity progress.

“For much of human history, most individuals have lacked economic freedom and opportunity, condemning them to poverty and deprivation.

Today, we live in the most prosperous time in human history. Poverty, sicknesses, and ignorance are receding throughout the world, due in large part to the advance of economic freedom.

The Index analyzes 186 countries. Economic freedom is based on 10 quantitative and qualitative factors, grouped into four broad categories, or pillars, of economic freedom:

1) Rule of Law (property rights, freedom from corruption);

2) Limited Government (fiscal freedom, government spending);

3) Regulatory Efficiency (business freedom, labor freedom, monetary freedom); and

4) Open Markets (trade freedom, investment freedom, financial freedom).”

Only time will tell if we will regain our freedom or continue to lose it. Much depends on a new President and changes in Congress in 2016.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, ELECTIONS, FREEDOM, OBAMA, POLITICS, TAXES

I like CNSNews, because they provide straightforward number-crunching on fiscal minutia that is tedious yet important data. This week as we enter the 8th year of Obama’s term, they have calculated that federal debt has increased more than $70,000 per household during the 7 years Obama has held office thus far.

From CSNNews:

“The debt of the federal government increased by $8,314,529,850,339.07 in President Barack Obama’s first seven years in office, according to official data published by the U.S. Treasury.

That equals $70,612.91 in net federal borrowing for each of the 117,480,000 households that the Census Bureau estimates were in the United States as of September.

During President George W. Bush’s eight years in office, the federal debt increased by $4,899,100,310,608.44, according to the Treasury. That equaled $44,104.65 in net federal borrowing for each of the 111,079,000 households that, according to the Census Bureau, were in the country as of Jan. 20, 2009, the day that Bush left office and Obama assumed it.

In the fifteen years from the beginning of Bush’s first term to the end of Obama’s seventh year in office, the federal debt increased $13,213,630,160,947.51.

That $13,213,630,160,947.51 increase in the debt during the Bush-Obama years equals $112,219.57 for each of the 117,748,000 households that were in the country as of September.

When Bush took office on Jan. 20, 2001, the federal debt was 5,727,776,738,304.64. When Obama took office eight years later, on Jan. 20, 2009, the federal debt was 10,626,877,048,913.08.

As of Jan. 20, 2016, when Obama completed his seventh year in office, the federal debt was $18,941,406,899,252.15.

by | ARTICLES, BLOG, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAX TIPS, TAXES

The article written by Josh Zumbrun of the Wall Street Journal on December 31, entitled, “Tax Rate for Top 400 Taxpayers Climbed in 2013,” should have been fairly straightforward with interesting data on that particular tax demographic. Unfortunately, the author distorts some aspects of the tax code, which makes the article a bit suspect and disappointing.

Zumbrun begins by gleefully announcing that “Tax rates on the 400 wealthiest Americans in 2013 rose to their highest average since the 1990s, after policy changes that boosted levies on capital gains and dividends.”

Here’s the first major problem. Tax rates may have risen in 2013 — but not because of rate increases on capital gains and dividends; several other tax changes also affecting the wealthy happened due to the Fiscal Cliff negotiations. Some of these include 1) The top marginal rate increased from 35 percent to 39.6 percent; 2) a phase out of personal exemptions; 3) a phase down of itemized deductions; 4) an increase in the death tax.

However, the author fails to mention those in an attempt to focus solely on capital gains.

This is especially evident in his next section. “Over the years, these taxpayers have devised strategies to collect more of their income as capital gains—profits from the sale of property or an investment—and dividends.” Unfortunately, the author has a total lack of understanding of capital gains. He erroneously, like many others, writes as though capital gains are income and thus lumps capital gains discussions together with income discussions. But that distorts the tax picture and tax strategy.

Capital gains are unusual in that the taxpayer has the ultimate decision as to whether and when to sell his asset (stock, his business, a work of art, etc.) The higher the tax rate, the LESS likely he is to sell, seeing as he will only be able to enjoy or reinvest what is left of the proceeds AFTER TAX. History has borne this out – capital gains tax collections go down in the periods after increases, and go up in the years after decreases.

The actual impact of raising the capital gains rate is also devastating to the economy. By discouraging the sale of assets, there is reduced capital available for new projects and opportunities, reducing job creation and wages, and resulting in lower revenue collection.

Furthermore, with higher capital gain rates, the expected after tax rate of return on new projects will go down, assuring that fewer of them will go forward.

But none of this seems to matter to the author. By alluding to “strategies to collect more income as capital gain profits” and describing how, with impending rate increases, “many of the highest earners sold assets before the deadline to avoid higher taxes, leading to a huge surge in income in late 2012,” the author is subtly suggesting that these actions are somehow wrong, underhanded, or unfair.

Juxtaposing that with his opening statement about how tax rates rose on the wealthiest Americans in 2013, the author seems to be dipping his toes into the class warfare playbook of “taxing higher income earners more is a good.”

This becomes readily apparent in the second half of the article, where the author brings up how the “capital-gains rate has become a prominent feature of 2016 presidential candidates’ tax proposals” — pointing out that top Republican candidates such as Cruz or Rubio would seek to lower the rates.

He also helpfully includes quotes about the wealthy and capital gains, and all the tax revenue they bring in. ““It’s not chump change,” said Len Burman, director of the Tax Policy Center, a nonpartisan think tank. Capital-gains taxes bring in more than $100 billion in some years “and almost all of it is realized by people with very high incomes,” he said. In 2013, the 400 households earned 5.3% of all dividend income and 11.2% of all income from sales of capital assets.”

Thus, using 2013 as a bellweather year for higher tax rates for the wealthy, the author tries to correlate it with capital gains — in order to suggest to the reader that higher capital gains taxes on the wealthy is an economic good. This is where he is woefully incorrect. What could have been an interesting article was sprinkled economic ignorance and a subtle agenda.

by | ARTICLES, BLOG, CONSTITUTION, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAX TIPS, TAXES

The IRS is involved in another “erased hard drive” event — and it’s not a part of the IRS scandal of 2013. It is apparent that there is a pattern of destruction at the agency.

This time, the hard drive that was erased belonged to “Samuel Maruca, former director of transfer pricing operations at the IRS Large Business and International Division.” Maruca was also a top level employee at the IRS, and was also involved in a controversy; this time, the scrutiny involved the IRS’s decision to hire an inexperienced yet elite law firm to handle tax data.

In this particular incident, “although there was a court preservation order on all documents related to the IRS hiring of the outside firm, the hard drive was erased anyway. The order was borne of a Freedom of Information Act (FOIA) request submitted by Microsoft.

Even though the white shoe law firm has zero experience handling sensitive tax data, taxpayers have been footing bills of over $1,000 per hour for its services.”

And more:

“Despite its complete inexperience handling audits or taxpayer data, Quinn Emanuel was hired under an initial $2.2 million contract.

This unusual decision prompted a probe by Finance Committee Chairman Orrin Hatch (R-Utah), based on concerns that the decision to hire outside contractors was expensive and entirely unnecessary.

As Sen. Hatch pointed out in his letter to the IRS, the agency already has access to around 40,000 employees responsible for enforcement. The IRS can also turn to the office of Chief Counsel or a Department of Justice attorney, both of which have the expertise to conduct this kind of work, without risking sensitive information.

The fact that another important hard drive is permanently gone can only lead to two conclusions: 1) that the IRS is still thoroughly incompetent or 2) the IRS is exceedingly corrupt. Neither of these are good for the taxpayer. The only immediately remedy should be to remove IRS Commissioner John Koskinen.

by | ARTICLES, BLOG, ECONOMY, GOVERNMENT, TAX TIPS, TAXES

Tax season has begun. Normally, the deadline for filing your federal tax return is April 15. But because the Washington D.C. Emancipation Day holiday falls on April 15 this year, Tax Day is the Monday after, April 18th.

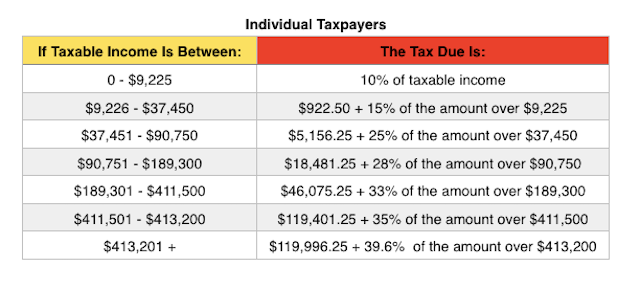

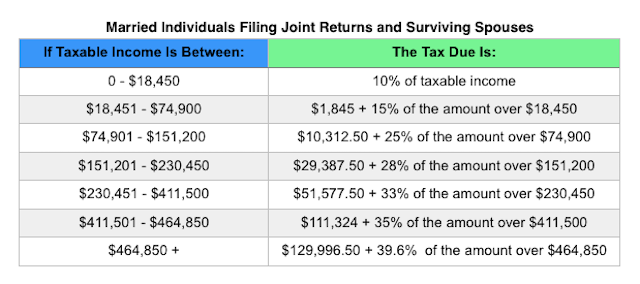

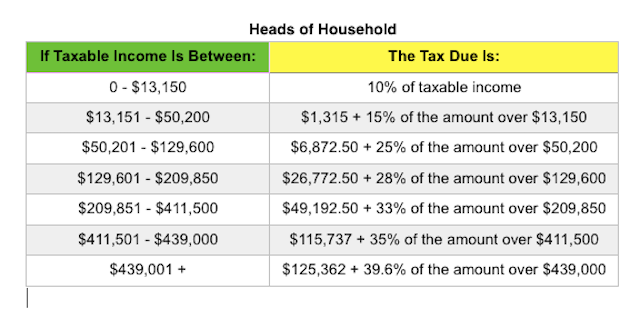

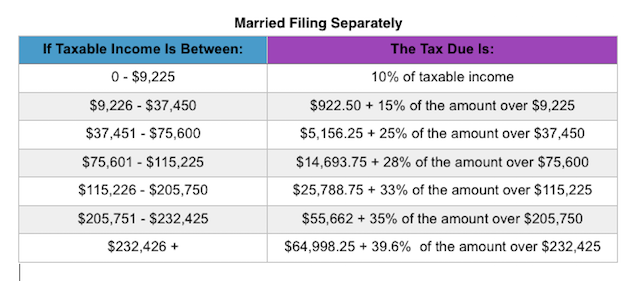

Last spring, Forbes put together a nice, extensive list of all the tax rates and adjustments for 2015. I have posted below some of the most pertinent information. For an all-inclusive list, you should check out the article in its entirety.

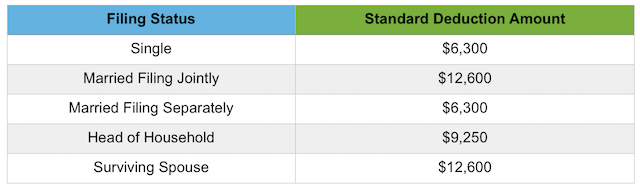

The standard deduction amounts are:

Some tax credits are also adjusted for 2015. Some of the most common tax credits are:

Earned Income Tax Credit (EITC). For 2015, the maximum EITC amount available is $3,359 for taxpayers filing jointly with one child; $5,548 for two children; $6,242 for three or more children (up from $6,143 in 2014) and $503 for no children. Phaseouts are based on filing status and number of children and begin at $8,240 for single taxpayers with no children and $18,110 for single taxpayers with one or more children.

Child & Dependent Care Credit. For 2015, the value used to determine the amount of credit that may be refundable is $3,000 (the credit amount has not changed). Keep in mind that this is the value of the expenses used to determine the credit and not the actual amount of the credit.

Hope Scholarship Credit. The Hope Scholarship Credit for 2015 is an amount equal to 100% of qualified tuition and related expenses not in excess of $2,000 plus 25% of those expenses in excess of $2,000 but not in excess of $4,000. That means that the maximum Hope Scholarship Credit allowable for 2015 is $2,500. Income restrictions do apply and for 2015, those kick in for taxpayers with modified adjusted gross income (MAGI) in excess of $80,000 ($160,000 for a joint return).

Lifetime Learning Credit. As with the Hope Scholarship Credit, income restrictions apply to the Lifetime Learning Credit. For 2015, those restrictions begin with taxpayers with modified adjusted gross income (MAGI) in excess of $55,000 ($110,000 for a joint return).

Changes were also made to certain tax Deductions, deferrals & exclusions for 2015. You’ll find some of the most common here:

Student Loan Interest Deduction. For 2015, the maximum amount that you can take as a deduction for interest paid on student loans remains at $2,500. Phaseouts apply for taxpayers with modified adjusted gross income (MAGI) in excess of $65,000 ($130,000 for joint returns), and is completely phased out for taxpayers with modified adjusted gross income (MAGI) of $80,000 or more ($160,000 or more for joint returns).

Flexible Spending Accounts. The annual dollar limit on employee contributions to employer-sponsored healthcare flexible spending accounts (FSA) edges up to $2,550 for 2015 (up from $2,500).

IRA Contributions. The limit on annual contributions to an Individual Retirement Arrangement (IRA) remains unchanged at $5,500. The additional catch-up contribution limit for individuals aged 50 and over remains at $1,000.

Also note that the floor for medical expenses remains 10% of adjusted gross incocome (AGI) for most taxpayers. Taxpayers over the age of 65 may still use the 7.5% through 2016.

For a more complete list of tables and rates, check out the Forbes article or visit the official IRS website.

by | ARTICLES, BLOG, BUSINESS, ECONOMY, GOVERNMENT, NEW YORK, POLITICS, TAXES

On Wednesday, January 6, Mayor DeBlasio proclaimed a $15/hr minimum wage for the public workers in New York City. The cost for such a plan is expected to be more than $200 million over the next five years. Both De Blasio and Gov. Cuomo seem intent on playing the role of wage-crusader during their respective terms — but only for some New Yorkers.

Just like DeBlasio, Gov. Cuomo announced in early January that “he would provide a $15-an-hour minimum wage to some 28,000 state university workers.” And last November, “the governor made New York the first state to set a $15 minimum wage for public employees; he also took steps to secure $15 an hour for workers at fast-food chain restaurants.” DeBlasio, too, has sought other ways to provide more generous benefits. Late in December, he announced that NYC “would begin offering six weeks of paid parental leave to 20,000 city employees.”

The problem is that these minimum wage hikes not only add to the budget woes, it also creates inequalities between the public and private sector (except for fast-food workers). How is it good for New York that a McDonald’s open next door to a pizza shop with a $5 minimum wage difference? And how can Cuomo attract more businesses to New York state with costs that are already the highest in the entire country — when he is going to make them even higher?

Here in New York City, a minimum wage hike for public workers would mean that New York City will pay more for its labor than it currently has calculated to pay, in order to produce the exact same product or services. Looked at it another way, to then keep to the operating budget, NYC will get less goods and services for the taxes it receives. This would result in a bigger budget deficit — because of having to spend more overall to maintain the current goods and services.

Minimum wage hikes no one anyone except the pockets of the public sector workers, while pushing the budget on an even more unsustainable trajectory. The rest of the taxpayers will be expect to either 1) have yet another tax increase in the near future or 2) see diminished services. Neither of these scenarios benefits New Yorkers.

by | ARTICLES, BLOG, ECONOMY, ELECTIONS, FREEDOM, GOVERNMENT, OBAMA, POLITICS, TAXES

After nearly 8 years of listening to Obama talk incessantly about the need for the wealthy to “pay their fair share,” Hillary Clinton has picked up the mantle in her new tax proposal unveiled this week.

Clinton spoke about the need for “an additional 4 percent tax on people making more than $5 million per year, calling the tax a “fair share surcharge.” It is reminiscent of the failed “Buffet Rule” proposal put forth by Obama a few years back.

According to a Clinton staffer, “This surcharge is a direct way to ensure that effective rates rise for taxpayers who are avoiding paying their fair share, and that the richest Americans pay an effective rate higher than middle-class families.”

The tax proposal is calculated to bring in $150 billion on revenue over a ten-year span. Nowhere does it calculate the cost of implementing such a plan, additional paperwork, hours spent on compliance and enforcement, and so forth. As a revenue raiser, it amounts to $15 billion a year for the federal government, pocket change really — something that could be more easily attained by cutting the size and scope of many federal budgets.

It’s not really about revenue anyway. It’s more about pandering to a segment of voters, vilifying the high income earners and stirring up class warfare. It was the one message that resonated most with Obama supporters in 2012; he continuously and intentionally railed against “millionaires and billionaires”, and talked about “the wealthy paying their fair share” in order to create a divide and separate that particular fiscal population from the rest of “mainstream America”. Hillary is merely following the leftist playbook and recycling stale ideas as her candidacy flounders.

by | ARTICLES, BLOG, CONSTITUTION, ELECTIONS, FREEDOM, OBAMA, POLITICS, TAXES

Earlier this week, the Supreme Court heard arguments about the constitutionality of union fees. The case involves an Orange County teacher who has sued to strike down the mandatory fees which pay for both collective bargaining and union activities.

A ruling is expected in June. If the mandatory fees are struck down, the unions will undoubtedly face financial difficulty, as it can no longer compel citizens to pay up. How this plays out in a Presidential election year will be even more interesting.