On February 2nd Senator Elizabeth Warren announced that she will join the Senate Finance Committee, the committee tasked with writing this country’s tax laws. She stated, “I’m very pleased to join the Finance Committee, where I’ll continue to fight on behalf of working families and press giant corporations, the wealthy, and the well-connected to finally pay their fair share in taxes.”

Warren has often advocated for a wealth tax in the past, especially during her campaign last year for the Democratic presidential nomination. But now she is actually in a position to make proposed legislation happen. In fact, she’s promised that it will be her “first order of business.” This is wrongheaded on many levels, including fairness, constitutionality, impossibility of implementation, history of failure, negative effect on the economy, and morality.

Fairness: Senator Warren has always maintained that corporations and the wealthy are not paying their “fair share”. She has never addressed the question of what that “fair share” might be. That is not surprising, since corporations and the wealthy in the US pay a far higher share of the tax burden than is paid in virtually every other country in the developed world – and by a wide margin. This results not from very high rates, but rather from the fact that our poor and middle class – almost 50% of our population – pay almost no income tax. According to the Tax Foundation’s 2021 data analysis, in 2018 (the most recent figures available),“the top 50 percent of all taxpayers paid 97.1 percent of all individual income taxes, while the bottom 50 percent paid the remaining 2.9 percent.” Additionally, “The top 1 percent paid a greater share of individual income taxes (40.1 percent) than the bottom 90 percent combined (28.6 percent).” To add a wealth tax on top of the already extremely progressive tax system would be anything but fair.

The grotesque unfairness of a wealth tax is even more evident when it is actually calculated. This can be seen by the following example: Assume that an investor with $100M net worth in the present low interest environment (and because not all of his wealth is appreciating assets) has an average rate of return of 4%. His income therefore is $4 million. The investor would pay an income tax rate of about 45% total combined federal/state/local taxes which would be $1.8 million in taxes. Now consider a 2% wealth tax tacked on, which would be an additional $2 million. This would mean the investor would pay a total of $3.8 in taxes and he would have an effective tax rate of 95%. What’s even more sobering is that if he earns less than 4%, or if his tax rate was more than 45% (which it will be with Biden’s plans), then the investor’s taxes would be in excess of 100%.

Constitutionality: Our Constitution provides in Article 1, Section 9, Clause 4 that: “No Capitation, or other direct, Tax shall be laid, unless in Proportion to the Census or Enumeration herein before directed to be taken.”

Both our income tax and a wealth tax would run afoul of this provision. To make the income tax constitutional we had to add the 16th Amendment. But no such amendment exists for the wealth tax. It may be that wealth tax proponents would argue that this tax is somehow taxing income potential using wealth as a proxy. But no Supreme Court, other than an off-the-charts progressive one, would approve of such strained logic. In fact, there’s currently a case before the Ninth Circuit Court of Appeals challenging Trump’s Mandatory Deemed Repatriation Tax on the ground that it is, in fact, an unconstitutional wealth tax.

Implementation: Taxing someone’s wealth requires determining the fair market value (“fmv”) of his or her assets, and then (presumably since no details are currently available) subtracting all liabilities. For anyone of considerable wealth, this would be an extraordinarily expensive, time consuming, and complicated effort. Even for assets that might have a publicly available market for valuation, it isn’t that simple. Consider volume. If someone has a substantial amount of something, you normally would apply a discount, since selling large volumes of assets can upset the market and reduce the overall value of an item.

But not everything has a value that can be determined easily. Investment in a closely held business, or real estate, or even paintings are examples of assets that are not susceptible to easy valuation on an annual basis, making it not very economically feasible to try to do so. Additionally, valuation can be determined in any number of ways — such as appraisals, discount rates, and reductions in the lack of marketability– so that valuations may be varied.

Another factor that makes valuations difficult are contingencies. For example, many assets have contingencies backed up with guarantees, and it’s difficult to value those contingencies. Finally, there is a question of liquidity/ability to liquidate or pay. Most people who have extraordinary assets like that often don’t have sufficient income or liquid assets to pay a wealth tax on them. Since many assets are not easily marketable, there could be a liquidity crunch.

Of course, a wealth tax would add even more burdensome complexity to the already byzantine tax code. The IRS would have to substantially increase its number of agents and its budget just to have the manpower to devote to compliance and enforcement. Given the IRS’s history of being discriminatory and incompetent, this is not a good thing.

Failure: It should also be noted that the wealth tax has already been tried — and failed — repeatedly. At one point, 15 European countries had a wealth tax. To date, all but four nations have since repealed it because it was ineffective in accomplishing its goals and was extraordinarily complicated and expensive to administer. Additionally, the wealth tax induced capital flight and asset hiding. For instance, in 2017 France decided to abandon its wealth tax after it caused the loss of “10,000 people with about 35 billion euros ($41 billion) in capital abroad” over a 15 year period according to the Prime Minister. Likewise, Switzerland — one of the four remaining wealth tax countries — experienced substantial tax evasion, noting that a mere “.1% wealth tax lowers reported wealth by 3.4%” according to a study by the National Bureau of Economic Research. As Switzerland has a wealth tax rate of 1%, that amounts to 34.5% in unreported assets.

Effect on the Economy: The growth of our economy is dependent on putting capital to productive use. Every time a corporation reinvests its retained earnings, or an individual puts his wealth to work by investing in an ongoing or new venture, the economy grows. This growth results in new purchases of equipment, facilities, hiring of employees, research and development, etc. Conversely, when capital is removed from the economy, such as by requiring the payment of a wealth tax, the economy shrinks. In fact, the wealth tax is a form of double taxation. Wealthy Americans already pay taxes on their income; under a wealth tax, they would then be taxed again for keeping that income in various assets. This not only punishes success, but discourages investment and savings.

Though progressives may argue that the capital taken out of circulation will be used to redistribute income to those who will spur the economy by consuming those funds, we revert back to Economics 101 – consumption has a much smaller effect on the economy than investment.

Morality: There is no moral justification to take something from someone just because they have it, even if they have a lot of it. One is reminded of the great scholar Thomas Sowell, who understands this quite well: “Since this is an era when many people are concerned about ‘fairness’ and ‘social justice,’ what is your ‘fair share’ of what someone else has worked for?” The wealthy in this country are an extraordinarily charitable group. But it should be their choice as to how charitable they wish to be with their hard-earned assets.

Senator Warren has argued that a real benefit of this tax is that it will only affect a relatively small number of people. This reveals what this tax really is – an attempt to foment class warfare by giving a large number of people (read: voters) a benefit through confiscating substantial amounts of money from a small group.

A wealth tax will certainly not bring in the revenue expected by the progressives – who relish the thought of punishing wealthy Americans in order to throw more money at their failed policies. Wealth redistribution is inherently the antithesis of the American Dream. Bastiat was right. No matter how you spin it, explain it, try to justify it, a wealth tax is simply “legal plunder.” Perhaps Senator Warren is being disingenuous (since the wealth tax would never be passed) but she will nevertheless score political capital among her constituents who do not know any better. She is taking advantage of the lack of economic knowledge among people who don’t understand the complexity and stupidity of a wealth tax.

One of the most outrageous and economically stupid measures to pass on Election Day came out of San Francisco: a new tax called the “Overpaid Executive Tax.” It’s really as bad as it sounds. This law levies a .1% surcharge on any company in San Francisco whose top executives earn 100 times more than the “typical worker.” It was enacted as a means to fight against pay inequality, but all it does is show how incompetent its proponents really are.

It’s worth noting that this tax applies to both publicly traded companies and private companies within San Francisco and it ensnares both local companies and large companies that conduct business within the city. What’s more, it’s completely arbitrary. What are you comparing when you say 100x or 200x the typical local worker? Does that mean on an hourly basis? Does it mean a part time typical worker compared to a high level overtime executive? Do you include overtime? Do you include benefits? It’s a virtually impossible number to calculate. And even if you did have a number to calculate, why is it 100x and not just 50x? Let’s say you compare a high tech company with a retail company such as a supermarket. The supermarket will have a lot of lower wage workers, whereas a tech company will have a lot of higher paid workers. It’s comparing apples to oranges in an effort to get someone to “pay their fair share.”

I hope this has the economically expected effect of them losing a lot of money and business, which is obviously the opposite of what San Francisco probably wants during a pandemic. Current companies will likely change their hiring plans to eliminate or reduce the amount of lower-lever/lower paid workers. Likewise, companies considering doing business in San Francisco will undoubtedly hesitate or entirely change their mind. Why do business in a locality that is particularly anti-business with such ridiculous rules. Furthermore, this surcharge is basically not a tax, it’s a forced donation (because those affected have the option of leaving if they want to). It puts a responsibility on the company to leave San Francisco because the tax affects all the shareholders of the company. This also means that any company that doesn’t leave San Francisco because the tax applies to them is someone who is ultimately abusing their shareholders to whom they have a fiduciary responsibility.

This tax is utterly meaningless and it just shows that people proposing this are so economically ignorant that they should be embarrassed. The problem is that the people on the Left who come up with such ridiculous ideas are never actually embarrassed by that ignorance.

One of the most overlooked yet troubling aspects of Biden’s plan is his doubling of the Global Intangible Low-Taxed Income (GILTI) tax. GILTI taxes items that generate foreign income and profits owned by American companies with foreign affiliates. This is troubling, because GILTI taxes American companies on income that has virtually nothing to do with anything in the United States. It’s bad enough that the current tax rate is 10.5%; Biden wants to raise this to 21%.

The tax laws of every developed country – except the US – provide that their companies do not pay tax on earnings from outside their country. Thus a German company earning money from activities in China or the UK pay taxes only to that jurisdiction – not to Germany. The US always taxed US companies on earnings from abroad, as soon as that money was returned to the US. That created a pretty stupid situation, encouraging these companies to leave this money outside of the US, and invest it in foreign, non US ventures.

The GILTI tax was created as part of the Tax Cuts and Jobs Act (“TCJA”) of 2017 as part of the attempt to fix this situation. What the TCJA did was require that all companies with foreign operations have to pay a penalty tax on all the money accumulated abroad, going back to the ‘80s; this rate was low and spread over 8 years. In exchange for it, the idea was that US companies would now be on par with other countries, in a territorial formation. In other words, pay a low tax on the money the US company never repatriated, repatriate it, and then in the future, you don’t pay tax on it, thereby discouraging profit shifting.

But Congress lied. In addition to paying the upfront tax at a low rate and thereby getting a tax for the future, they couldn’t help themselves. They added the GILTI tax, so now it’s taxed whether it’s repatriated or not. And this is bad. Congress reneged a little bit, because the GILTI is a relatively low tax but because it is worldwide, and now they have to pay tax every year on these foreign profits. So companies paid upfront and now they have to pay this tax every year — albeit at a low rate — so now it’s worse.

Now what Biden is suggesting with the GILTI tax is basically fraudulent. People paid that upfront fee so not to have to pay taxes — and now with this proposed 21% rate — is like fraud against American international companies. The 2017 tax act required an upfront benefit that got future benefits, now Biden wants to take away the future benefits.

GILTI puts American companies operating abroad at a competitive disadvantage. The foreign affiliates already have to pay a penalty tax just to be on equivalent footing with other companies abroad (companies that don’t have to pay the GILTI tax here, mind you). GILTI then tacked on a 10.5% tax and now Biden wants to double it — when it should be ZERO.

Biden’s plan to double GILTI goes hand-in-hand with his overall plan to tax U.S. businesses (he also wants to raise the corporate tax rate to 28% and add a 15% minimum tax based on profit reported on financial statements.) Going after businesses is already bad policy and his desire to double GILTI shows his ignorance and his willingness to further erode American competitiveness.

The amount of money Biden’s plan will raise is relatively insignificant (roughly $300 billion over the next ten years) but his attack on businesses is mean-spirited; it hurts our country by making our domestic companies less able to compete abroad in foreign markets. Nevermind that foreign income shouldn’t even be taxed at all! How can Biden justify raising taxes in a way that will make the United States less competitive and will reduce jobs? Increased taxes are a disincentive towards investing and job creation and will only hurt our economy.

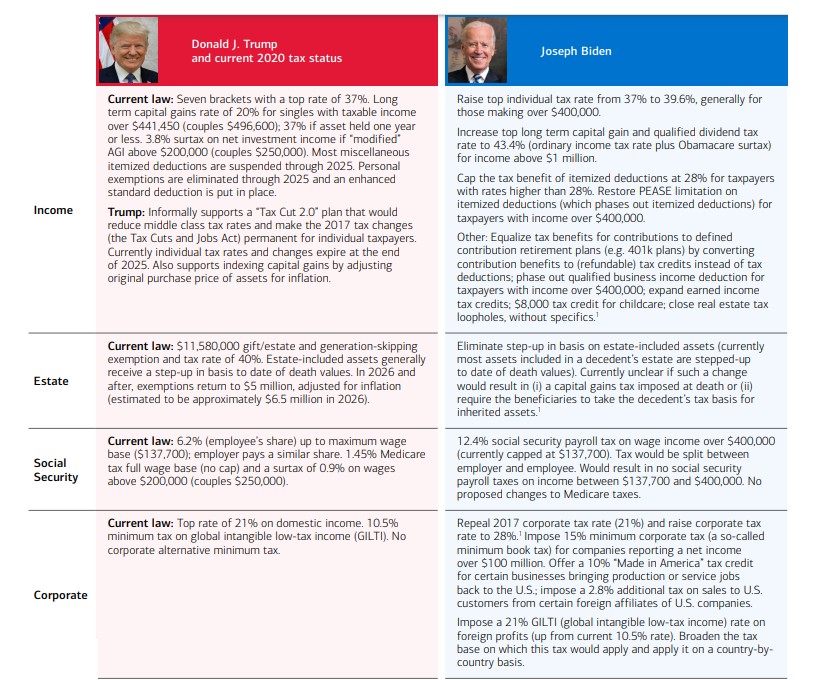

Now that Biden has been elected President, it’s important to take stock of what tax changes are likely to be coming. Merrill Lynch did a good job putting together a side-by-side comparison of current tax law in four areas: income, estate, social security, and corporate, and then possible changes in those areas according to Biden’s campaign tax plans. The summary is below.

It is notable that in just about every instance, there will be a tax increase under Biden’s plans. How this will impact the economy, jobs, wages, and investments remains to be seen.

Earlier this year, California passed AB5, a measure that would require companies to reclassify independent contractors as employees. The problem is that the government is yet again intruding on employer-employee relationships under the guise of worker protections. Furthermore, it’s an attempt to put unions even more in charge of things in California while also purporting to provide more revenue to a nearly-bankrupt state, all doomed to failure because of its economic ignorance.

AB5 affects those workers who belong to the gig economy. “Gig economy” is the catchphrase for the portion of the economy made up of freelancers and independent consultants. It’s estimated that 1 in 3 workers now, about 55 million, fall into this category. The gig economy has grown to be very good because it provides much-needed work flexibility and independence that many workers prioritize.

The mechanism by which freelance workers are deemed employees is the “ABC test.” This is the court created formula that companies must apply in order to determine if workers are contractors instead of employees, and it puts the burden of proof on employers. A worker is a contractor if he meets the following three criteria:

1) The worker is free from the control and direction of the hiring entity in connection with the work’s performance, both under the contract for the performance of the work and in fact.

2) The worker performs work that is outside the usual course of the hiring entity’s business.

3) The worker is customarily engaged in an independently established trade, occupation, or business of the same nature as the work performed

There is no economic or business rationale to these tests – they were created solely to destroy the concept of independent contractor by making virtually all relationships that of employer/employee. The IRS, on the other hand, has established criteria for what constitutes a real employee based on behavioral control, financial control and relationship of the parties. It should also be noted that if the IRS follows the AB5 definition of employee for Californians, the employees will be devastated! That is because under IRS tax rules, employees may not deduct any business expenses, which is a critical tax benefit to the independent contractor relationship.

It is particularly frustrating that advocates of AB5 purposefully ignore the fact that the gig economy arose during the weak Obama economy, which was littered with ever-increasing government regulations and crushing legislation such as Obamacare. This combination made it difficult to become a business or stay in business. It was certainly no wonder that businesses sought alternative forms of employer-employee relationships, which is their inherent right to do so. AB5 now undermines those relationships.

Furthermore, AB5 essentially picks winners and losers; large swaths of independent contractors are exempt, while others have restrictions, and still others are not exempt at all. Among those exempt include: “insurance brokers, doctors, dentists, lawyers, architects, engineers, private investigators, accountants, investment agents, salespeople, commercial fishermen, and real estate agents.” Among those partially exempt include journalists and freelance media-makers such as photographers, but they are now limited in their number of contributions to 35 items per year. Those industries not exempt at all include Uber and Lyft, companies who successfully arose as alternative transportation options during the rise of the gig economy.

And yet, there are really no winners here. Certain industries are exempt, but there’s no justification to do that from a logical point of view. The sole reason why some have an exemption is because they have too strong of a lobby or union presence — which is an irrational justification. There will also be a never-ending succession of lawsuits, as workers try to avoid being treated as an employee. The only winners will be the lawyers.

The gig economy has proven to be a resourceful alternative for workers who seek a myriad of benefits, including work independence, flexible schedules, side money, and increased quality of work-life balance. Now that the economy has recovered from the anemic and over-regulated Obama years, governments such as California are happy to cash in on its success while strangling its workers and businesses with unnecessary, burdensome measures. AB5 will ultimately weaken the economy and destroy some businesses in its wake.

On November 3, Illinois residents have a Constitutional referendum to change their method of taxation from a flat tax to a “fair tax.” The current system treats all Illinois taxpayers the same by levying a modest 4.95% rate. Under the proposed change, taxpayers would be divided among multiple tiers with a progression of increased rates based on higher levels of income, and both individual and corporate rates would be affected. By removing the Constitutional provision against graduated-rate taxes, the power of taxation is given to the state lawmakers who can decide varying levels of rates for various groups of taxpayers with a simple majority vote. In contrast, the flat tax provides some protection against outrageously high rates because it is impractical and politically unpopular to do so among certain segments of the population.

In anticipation of the referendum passing, the Illinois legislature passed a tax plan that would be implemented on January 1, 2021. Although the Illinois governor — like most progressive morons — has assured taxpayers that the change won’t affect most residents, the impact of the new plan will indeed have dire consequences for many individuals. The new tax rates range from 4.75% to 7.99%. While the lowest 20% of earners will see a decrease in rates, that translates into a whopping $6.00 on the median average earnings of $12,400. On the other end of the spectrum, the new plan includes not only higher rates, but also a recapture provision for highest earners, so that not just their marginal income, but their entire income, is taxed at the 7.99% rate. What’s more, the new plan does not index for inflation on marginal income levels which will result in taxes consuming a greater percentage of taxpayer income if income levels do not increase.

Businesses will also be adversely impacted. The base corporate rate will increase to 7.99%. However, Illinois also has an additional set of taxes (called the PPRT) levied on corporate and pass-through income of 2.5% and 1.5% respectively. Combined with the new business rate, corporate income tax would be 10.49% and pass-through income tax would be 9.49%. At a time when businesses are struggling due to the pandemic, increased taxes only worsen the situation. Additionally, the business rate will be one of the highest in the nation, making Illinois a less competitive state in which to do business.

The new tax plan is intended to be a revenue raiser, originally calculated to be $3.6 billion in the first year — but that was before COVID-19. Yet the fiscal woes facing Illinois are overwhelmingly derived from massive overspending and ballooning pension obligations, and no tax hike will begin to fix it. According to Illinois Policy, the upcoming budget includes nearly $6 billion in deficit spending, with pension costs consuming more than 27% of expected general revenues. Furthermore, Illinois faces a current $4.6 billion shortfall. Without a balanced budget to restrain spending — Illinois has not seen one in 20 years — tax hikes will be inevitable. And by enacting the “fair tax,” Illinois lawmakers have the power of the purse to raise taxes and levy surcharges at their discretion.

According to revised revenue forecasts from the governor’s office, if the fair tax is enacted, the budget gap is approximately $6.2 billion; if the fair tax is not enacted, the estimated budget gap is approximately $7.4 billion. The change from a flat tax to a graduated tax imposed on Illinoisians is simply not worth the $1.2 billion in possible additional revenue when the legislature can’t even be bothered to find a way to cut spending. Governor Pritzker’s attempt to introduce equity in the tax code by making higher earners pay their fair share will hurt all taxpayers and businesses, especially at a time when the effects of COVID-19 on the economy are devastating across the board. The proposed “fair tax” is anything but for the taxpayers of Illinois.

As Biden is gaining closer to winning the upcoming election, his economic plan deserves more scrutiny. So far, Biden is clearly looking to Obama for his policy aspirations. Unfortunately, Obama was following FDR’s playbook to the detriment of our economy. Let’s take a look:

Obama’s policies resulted in the poorest recovery since the New Deal, just as FDR’s meddling only prolonged America’s longest depression ever. Obama followed FDR’s failed playbook – he raised taxes, over-regulated businesses, gave organized labor excessive power, instituted policies that discouraged people from working, and hurt international trade.

Firmly entrenched in Keynesian economics, Obama believed in government spending while wholeheartedly crowding out private spending; he substituted inefficient political and crony-based spending for free-market, give-the-public-what-they want spending.

This week in the WSJ, Jay Starkman issued a warning on Biden’s plans, in “Bidenomics May Repeat FDR’s Blunder.” He notes, “Today the U.S. economy is recovering from a great crash, as it was before Roosevelt’s tax onslaught. Unfortunately, Mr. Biden doesn’t seem to have learned the right lessons. Should he win in November, he proposes to cancel the Trump tax cuts, raising the top federal income-tax rate back to 39.6%, and raise the corporate income tax from 21% to 28%. He also promises to limit low capital-gains tax rates to the first $1 million in profits and extend the full Social Security tax to income above $400,000.” With Biden also promising to increase regulation and institute energy policy that will produce less energy at a much higher cost, danger is in the wind.

Why go back to the policies that have so clearly failed us before. After three years of robust economic activity during Trump’s administration before the onslaught of COVID, this country can neither risk nor afford Biden’s plans.

Are we past the tipping point for economic reform? I would argue that Obama’s budgets and spending accelerated the deficits beyond repair. Some people will go back to Reagan and say that the deficit and the debt ballooned during the Reagan Administration and they will blame it on his tax cuts. But what is actually true is that the tax cuts generated a large increase in revenue, and the only reason why he had deficits was that the Democrat-led Congress increased spending even over the increased revenue. The same thing happened with the Bush tax cuts which were very pro-growth; the revenue went up sharply, but spending went up even faster. But at this point the debt was still manageable.

Then you come to Obama. At the beginning of his administration, we had the deep recession -which arguably could have benefited by one year of stimulus. The concept of a stimulus is supposed to be a one-off event. In other words, you engage in big one-time expenditures to get the economy on track and then spending goes back to previous levels as the recovery occurs. The problem is that Obama didn’t put things in for just one year. He did long term things, like food stamps, teacher’s compensation, etc., knowing full well that once put into effect they could not easily be withdrawn. And it was pretty clearly his intent all along, for political reasons, to bake them into the budget. So now when we started to have a recovery, you had ballooning deficits — even with a growing economy. Then by the time Trump was elected, the locked-in recurring spending with its locked-in annual increases made the deficit – and the debt – almost impossible to rein in.

Now we have the pandemic and we have no place to go. There’s no surplus to go to the deficit. Millions of Americans are unexpectedly unemployed, which means they’re not paying into Social Security. At the same time, we see older workers who have lost their jobs choose to draw their benefits as soon as they become eligible. This will speed up the insolvency train. But then Trump did something that was very stupid (though his political motivation is clear). He said that entitlements are off the table. If entitlement reform is off the table at this point, we’re headed to bankruptcy.

We’ve been talking about the coming insolvency of the Social Security and Medicare programs for many, many years now and Congress has done nothing to stave off the inevitable. Couple that with Obama budgets, Trump’s lack of action, and the pandemic, and the deficits are even larger now. Anyone seriously looking at the situation knows that absent a major change to entitlements, the mandated annual increases, both because of cost of living adjustments and demographics, will bankrupt both programs in the next ten to fifteen years. It’s very safe to say that absent major entitlement reform, we’re basically past the tipping point.

For years, I’ve been pounding the table about how public sector wages and compensations have steadily outpaced those found in the private sector. This is no more readily apparent than in New York where runaway budgets and deficits continuously fleece the taxpayer.

The private sector has several factors in place that help control runaway costs, chief among them being competition. The profit motive in the private sector keeps compensation at levels where economic factors limit them to their true market value, reflecting economically rational and fair compensation levels. On the other hand, there are no such competitive inhibitions in the public sector where politics and cronyism, rather than economics, create a fairy-tale negotiation for wages and benefits.

Here’s a tale of two states: New York and Florida. In New York, it is clear that public service unions are a significant reason why the cost of living is higher. In 2010, Florida’s population was 18.8 million while New York’s was 19.3 million. In the past ten years, New York experienced population stagnation (19.4m) while in Florida, the population grew to 21.8 million and continues to be one of the fastest growing states in the country. Yet crucially, over the same period, New York’s budget increased to $177 billion while Florida’s was a mere $93 billion, up from 70.4 billion in 2010. One could argue that New York does more for its people than Florida does, but the reality is that they just spend more money. Bloated public service payrolls and off-the-charts cost burdens of regulation are the main culprits. And that’s the problem.

I propose that the people of New York withdraw its authorization to its elected officials to enter into any contracts with public service unions that provide compensation, benefits, and terms in excess of those being paid for similar work and skills in the private sector. Furthermore, there should be a requirement that restricts any federal government employee from receiving a raise if it puts his compensation in excess of the benefits and wages paid for the same work in the private sector.

By “competing” per se with the private sector for compensation, the government can do its part to help keep its budget and deficits from getting any more out of control.

New York’s state budget director, Robert F. Mujica, Jr., wrote an anemic, laughable Letter to the Editor (printed in the Wall Street Journal) trying to defend New York’s fiscal record in an effort to get a federal bailout. Those of us who live in New York couldn’t help but notice it was full of half-truths. For instance, Mr. Mujica boasted lowering income-tax rates, but neglected to include the fact that Florida doesn’t even have an income tax yet still manages to operate on a budget of $93 million vs NY’s $177 million — in a state with 2 million more people!

Furthermore, he talks about a 20% increase of private-sector jobs, but leaves out the fact that “private job growth in Florida has been about 60% higher than in New York from Jan 2010 to Jan 2020.”

Likewise, he claims that New Yorkers send $29 billion more in taxes to the federal government than it gets back, but fails to mention that the reason for this is New York’s tax code punishes high income earners by adding extra taxes, so much that some earners pay nearly 50% of their earnings in taxes! Nor does he mention that many wealthy New Yorkers have wised up to being fleeced over the last decade, making New York one of the top ten out-migration states in order for earners to try to keep their own income — some going to Florida, no less. This loss undoubtedly contributes to the $6 billion budget shortfall that existed before Coronavirus even hit, something that was also conveniently left out of his defense.

Finally, Mr. Mujica tries to suggest that the $29 billion New Yorkers send to the federal government somehow subsidizes Florida’s budget because Florida receives $30 billion more from the federal government than Floridians send. But he leaves out the fact that New York’s budget contains 35.9% of federal money compared to Florida’s 32.8%. With a budget of $177 billion, that’s $63 billion of spending from federal dollars compared to $30 billion in Florida. Who is more fiscally irresponsible?

If states like New York are not willing to take any of the economic risk going forward, they should not get any money. They have willfully chosen to engage in a prolonged economic lockdown in hopes that someone else pays for it. Florida was one of the last states to shut down and has begun opening up once again, understanding the need for economic recovery. If New York wants to continue to take the economic risk of staying closed while other localities choose to reopen, they should be the ones to pay for it.