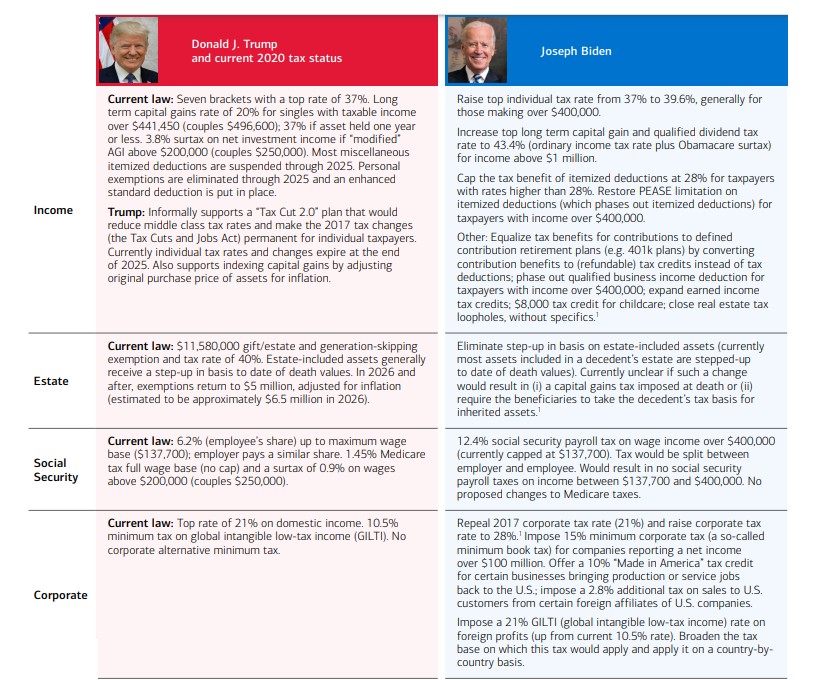

Now that Biden has been elected President, it’s important to take stock of what tax changes are likely to be coming. Merrill Lynch did a good job putting together a side-by-side comparison of current tax law in four areas: income, estate, social security, and corporate, and then possible changes in those areas according to Biden’s campaign tax plans. The summary is below.

It is notable that in just about every instance, there will be a tax increase under Biden’s plans. How this will impact the economy, jobs, wages, and investments remains to be seen.

When I read commentary by people associated with the Club for Growth — known for promoting the rule of law, low taxes, small government, low tariffs, economic growth, etc. — I expect to find analysis consistent with their principles. Therefore, the recent CNS News article on 8/10, “American Manufacturers Come Back, Thanks to Trump,” took me completely by surprise because it was essentially the rantings of someone who is economically ignorant. Ken Blackwell, former elected official in Ohio and current member of the Board of Directors for the Club for Growth advocates for protectionism, pure and simple.

Blackwell praises how Trump instituted “strategic counter-tariffs on bad actors such as China to combat the effects of illegal and abusive trade practices that previously put companies like Whirlpool at an unfair disadvantage.” But this pro-tariff position runs counter to any competent economic analysis. Tariffs clearly and consistently hurt the consumer and taxpayer by driving costs up to everybody in amounts far in excess than any benefits given to those crony beneficiary companies. To call a tariff a “pro-growth economic policy” as Blackwell does is utterly ridiculous, and his entire article reads like a cheap campaign ad.

Tariffs don’t “strengthen” American manufacturers as Blackwell believes; it is cronyism of the highest order. How the Club For Growth — as well as the National Taxpayers Union — can have someone on the board with views that are economically ignorant and destructive to our economy is beyond comprehension.

It’s really sad that Mitt Romney went off the deep end with regard to the commuting of Roger Stone’s sentence. Trump’s timing was definitely politically stupid and over the top. However, presidential pardons and commutations are often self-serving and inexplicable. Although Roger Stone was convicted of a relatively minor infraction of lying about something that was not of major significance, even that conviction was suspect because of clearly stated bias of the lead juror that should have led to a new trial. As such, his commutation was certainly less appalling compared to other pardons sometimes involving really horrific human beings.

Therefore, it is ridiculous that Mitt Romney declared Stone’s commutation was “unprecedented, historic corruption.” This is so absolutely wrong and incompetent that it could only be attributed the most vile case of Trump Derangement Syndrome. It seems that Mitt Romney either doesn’t know his history or is flat-out ignoring the fact that Stone’s commutation is one of a long line of Presidents using their Constitutional powers of pardon to benefit friends. Gerald Ford pardoned Richard Nixon. Richard Nixon pardoned Jimmy Hoffa. Bill Clinton pardoned his brother Roger Clinton and Marc Rich, the “fugitive financier.” Clinton also commuted the sentences of 16 members of FALN, the terrorists responsible for more than 130 bombings spanning several years against the wishes of Congress. Likewise, Obama commuted the sentence of one of the FALN masterminds, Oscar Lopez Rivera, who rejected the original commutation in 1999. Surely these pale in comparison to Roger Stone? As it is, Stone remains a convicted felon because he did not receive a full presidential pardon so he is not completely off the hook.

Romney’s assertions are completely unfounded and shows that his judgement continues to be unreliable. His response was so off the charts that it should make everyone doubt the credibility of anything that he says.

Are we past the tipping point for economic reform? I would argue that Obama’s budgets and spending accelerated the deficits beyond repair. Some people will go back to Reagan and say that the deficit and the debt ballooned during the Reagan Administration and they will blame it on his tax cuts. But what is actually true is that the tax cuts generated a large increase in revenue, and the only reason why he had deficits was that the Democrat-led Congress increased spending even over the increased revenue. The same thing happened with the Bush tax cuts which were very pro-growth; the revenue went up sharply, but spending went up even faster. But at this point the debt was still manageable.

Then you come to Obama. At the beginning of his administration, we had the deep recession -which arguably could have benefited by one year of stimulus. The concept of a stimulus is supposed to be a one-off event. In other words, you engage in big one-time expenditures to get the economy on track and then spending goes back to previous levels as the recovery occurs. The problem is that Obama didn’t put things in for just one year. He did long term things, like food stamps, teacher’s compensation, etc., knowing full well that once put into effect they could not easily be withdrawn. And it was pretty clearly his intent all along, for political reasons, to bake them into the budget. So now when we started to have a recovery, you had ballooning deficits — even with a growing economy. Then by the time Trump was elected, the locked-in recurring spending with its locked-in annual increases made the deficit – and the debt – almost impossible to rein in.

Now we have the pandemic and we have no place to go. There’s no surplus to go to the deficit. Millions of Americans are unexpectedly unemployed, which means they’re not paying into Social Security. At the same time, we see older workers who have lost their jobs choose to draw their benefits as soon as they become eligible. This will speed up the insolvency train. But then Trump did something that was very stupid (though his political motivation is clear). He said that entitlements are off the table. If entitlement reform is off the table at this point, we’re headed to bankruptcy.

We’ve been talking about the coming insolvency of the Social Security and Medicare programs for many, many years now and Congress has done nothing to stave off the inevitable. Couple that with Obama budgets, Trump’s lack of action, and the pandemic, and the deficits are even larger now. Anyone seriously looking at the situation knows that absent a major change to entitlements, the mandated annual increases, both because of cost of living adjustments and demographics, will bankrupt both programs in the next ten to fifteen years. It’s very safe to say that absent major entitlement reform, we’re basically past the tipping point.

Democrat Presidential Candidate Joe Biden not only wants to return capital gains to Obama-era rates, but furthermore he would increase them while simultaneously returning the top rate on ordinary income. Biden has said, “I believe we should, in fact, the capital gains tax should be at what the highest minimum tax should be; we should raise the tax back to 39.6 percent instead of 20 percent.”

Add to that the 3.8% Obamacare tax (NIIT) instituted in 2013, and he would have some taxpayers effectively paying a 43.4% long-term capital gains tax! The current total top rate is 23.8%

Biden should know better. The actual impact of raising the capital gains rate by the Obama administration was devastating to the economy. By discouraging the sale of assets, there was reduced capital available for new projects and opportunities, reducing job creation and wages, and resulting in lower revenue collection. Furthermore, the expected after tax rate of return on new projects went down, assuring that fewer of them went forward.

Additionally, there were a number of localities, like the state of California and New York City, which have tax rates of 12% or more and also a large concentration of wealthy people and high performing businesses. Obama’s capital gains rates of more than 37% brought elective capital projects to a crawl. And Biden wants to raise them even higher?

Shame on Biden. Why sell an asset to fund further investment and opportunity when the government takes a large share of the gain with the loss remaining all yours? It makes virtually no economic sense to do so. A higher capital gains rate put a stranglehold on risk-taking and available capital, and would negatively impact the economy.

I came across this article describing how the FDA is holding up a vaccine that’s being used in other countries. This the best concise explanation I have seen to describe the truth that the FDA drug oversight is a net negative to American’s health. From the article:

“In March, when the coronavirus arrived in the US in earnest, governments around the country locked down economies to prevent the spread of a virus that to date has claimed the lives of nearly 400,000 Americans. While these actions were being taken, a vaccine had already been developed. The mRNA-1273, a lipid nanoparticle–encapsulated mRNA-based vaccine, was made in a single weekend in January, two days after Chinese researchers published the coronavirus’ genetic code.

Developing the vaccine was the easy part, it turns out. Testing the vaccine and navigating it through the federal bureaucracy was the real challenge. Not until March 16, more than two months after the vaccine was developed, were the first trial participants vaccinated. And these trials were followed by more later-stage clinicals.

There was another option that would have made the vaccine available much sooner: challenge trials, a process that would have involved deliberately infecting healthy volunteers with SARS-CoV-2 to accelerate vaccine development. Reports show at least 25,000 people volunteered to do just that.

Democrat Kamala Harris is the latest Presidential candidate to peddle the myth about “pay gaps” for female workers, going so far as to make this an essential part of her platform. Harris has a plan to require larger companies with 100 or more employees to obtain an “equal pay certification” every two years in order to ensure that men and women are paid equally.

There are many reasons a pay gap to exist — but it isn’t because of one’s gender. It has been shown time and again that many women have alternative career paths by choice: different jobs, amounts of time worked, lifestyle flexibility, and risks in occupation to name a few; therefore, any difference in the pay is a result of those choices and not discrimination.

Taking these items into consideration, the pay gap myth shrinks almost entirely, likely no more than a 2% variance. This empirical analysis should not be surprising — in fact, it should be what any normal person, certainly any business person, would expect. Because the simple economic reality is that if women actually did make 23% less than men in wage costs for the same work, businesses would almost entirely hire women as a means to minimize labor costs and maximize profits. Since this does not actually happen, it is obvious that the 23% wage disparity merely a distortion perpetuated by the Left to score easy talking points.

It is also a false conclusion that a gender pay gap is damaging to women because women will likely have substantially less money saved and earned over her lifetime. Those such as Harris that push such nonsense don’t even consider that, for many women, working full time may be “damaging” to women who have alternative life goals — such as raising a family — and that amassing retirement funds might not be the ultimate end focus. Voters should reject Harris “equal pay certification” proposal as economic nonsense.

The Tax Cuts and Job Act made some positive changes to the tax code. The reduction in marginal rates, especially on the corporate side, is noteworthy. However, there were several changes on the individual side which were absolutely ludicrous. These are noted below:

Without any discussion, Congress eliminated the miscellaneous itemized deductions. As I have written about before, in actuality, this one is truly the only legitimate deduction and is absolutely necessary to maintain the integrity of the tax code. With the new change now removing the miscellaneous itemized deduction, this person now has to pay taxes on the full amount earned without being able to deduct expenses accumulated while earning the income they are taxed on.

Another deduction Congress removed summarily is the moving deduction. Similar to the miscellaneous itemized deduction, this is a real expense that is incurred when moving to get a new job (in order to earn the income that will be taxed.) Now with the elimination of the deduction, taxpayers are no longer allowed to write off this cost.

The casualty loss deduction was also eliminated. This enabled you to deduct a loss that was due to a sudden unexpected event — such as a fire, hurricane, or robbery. Now if your house burns down, you can no longer write it off. The exception to this change is if your loss is in a federally-declared disaster area. So if your house burns down due to faulty wiring, you get no deduction. But if it burns down in a large wildfire that was later declared a disaster, you can claim the deduction. This is very egregious because the effect on the individual — the loss of a house due to a fire — is absolutely the same. This deduction elimination is unacceptable.

Furthermore, the alimony deduction was thrown out. The alimony deduction is a mechanism that prevented an inequitable tax burden to be created when a married family unit is split into two. Now, one can no longer deduct alimony payments, a move that is mean-spirited and creates a targeted tax burden on people who suffered a family breakup.

Additionally, there were two business-related deductions that were unnecessarily changed. The first one now caps the limit on the amount of business losses one can deduct at $250K ($500K if married), whereas the prior tax law did not. Furthermore, carryover losses are now limited. It used to be that you could carryover losses from one year to the next; for instance, if you had a $1 million loss on year but a $1 million gain the next, you could use that gain to offset the prior year loss. With the tax law changes, you can now only offset up to 80%.

While eliminating these important and equitable donations, Congress left in place a number of purely political/social engineering deductions and credits. Congress left in a substantial part of the mortgage deduction, which is really nothing more than a government subsidy to the real estate industry. They left in energy credits, rehabilitation and low income housing credits, and the Alternative Minimum Tax (AMT). It’s disappointing to see Congress talk about simplicity, efficiency, and equitability, while simultaneously removing good provisions from the tax code and leaving in parts that are merely political appeasements to various groups and industries. It would be wise for Congress to reinstate these various deductions as a means to truly maintain fairness within the IRC.

In 2017, Congress passed the Tax Cuts and Job Act, which has been beneficial on the corporate side of tax reform. On the individual side, Congress allowed politics to get in the way of real reform, and that is inexcusable. The most egregious example of this was the elimination the miscellaneous itemized deduction.

The miscellaneous itemized deduction was truly the only legitimate deduction in the Internal Revenue Code (IRC). Its inclusion was absolutely necessary to maintain the integrity of the tax code. This deduction allowed taxpayers the ability to write off expenses that were incurred as part of the process to earn the income they are taxed on! For instance, under prior tax law, a person who earned $100K in a business but had to pay $30K in legal fees to get it, would pay taxes on only the $70K net that was actually made during the process. With the new change now removing the miscellaneous itemized deduction, this person will have to pay taxes on the full $100K!

Simply put, if you can’t deduct miscellaneous itemized expenses, you wind up paying taxes on income that you actually didn’t earn. That is simply outrageous — and unfortunately, it is now the case as a result of last year’s tax reform. Allowing such deductions is truly the construct for fair tax law; everything else is merely subsidies, politics, picking winners and losers. Congress must act to restore this equitable provision and restore confidence to the taxpayers.

House Republicans have put forth a bill that would make some of the tax cuts and changes permanent instead of expiring after a few years. This includes:

The reduction in the individual tax rates

The increased new standard deduction, which went to $12000/individual and $24000 married couples

Special deduction for pass-through business owners

It’s worth noting that the corporate tax reduction was already permanent with last year’s law. Other additional financial parts of this new legislation include:

Allowing employers to join together to offer 401Ks in order to lower costs

Allow 401K users who have an annuity to transfer it tax-free to an IRA

Remove the age ceiling (70½) requiring distributions from IRAs and 401Ks, and continue to contribute up to $6,500/year in an IRA

Create a new universal savings account with a maximum of $2,500/year after tax funds that can used for non-retirement purposes

Allow parents to remove up to $7,500 from a retirement plan without penalty under certain child-related conditions.

Allow 529 college savings accounts to fund various other educational expenses, including apprenticeship programs, home schooling, or child student loan payments.

As if on cue, Democrats rebuke the legislation as being overly beneficial to the wealthy — as if the economic upswing which has helped everyone across-the-board, has not happened. They also chide the bill for adding to the federal deficit, even though Democrats were virtually silent when Obama had very sizeable deficits throughout most his administration. However, putting forth the legislation at this time indicates that Republicans are interested in talking about the strong economy ahead of the midterms elections — which is the smartest thing they can do right now. The GOP missed the chance to make the Bush Tax cuts permanent. They would do well not to make the same mistake twice.